Biologics, or complex drugs that are derived from living organisms, have revolutionized treatment of various conditions such as cancer, autoimmune diseases, and chronic illnesses. In 2023, eight out of 10 of the world’s top-selling drugs were biologics, including Merck’s Keytruda, AbbVie’s Humira, and Sanofi’s Dupixent.Due to their high costs, accessibility of biologics has been a challenge. That’s why biosimilars, or game-changing copycats of biologics that provide highly similar yet more affordable alternatives to established biologics, are becoming popular.The first biosimilar — Sandoz’ Zarxio — was approved by the US Food and Drug Administration (FDA) in 2015. Its reference biologic was Amgen’s Neupogen (filgrastim). Since then, the global market for biosimilars has been growing at an impressive pace — between 2015 and 2020, it grew at a whopping compounded annual growth rate (CAGR) of 78 percent, touching US$ 17.9 billion in size. It is expected to continue growing at a CAGR of 15 percent and reach a size of about US$ 75 billion by 2030.Major

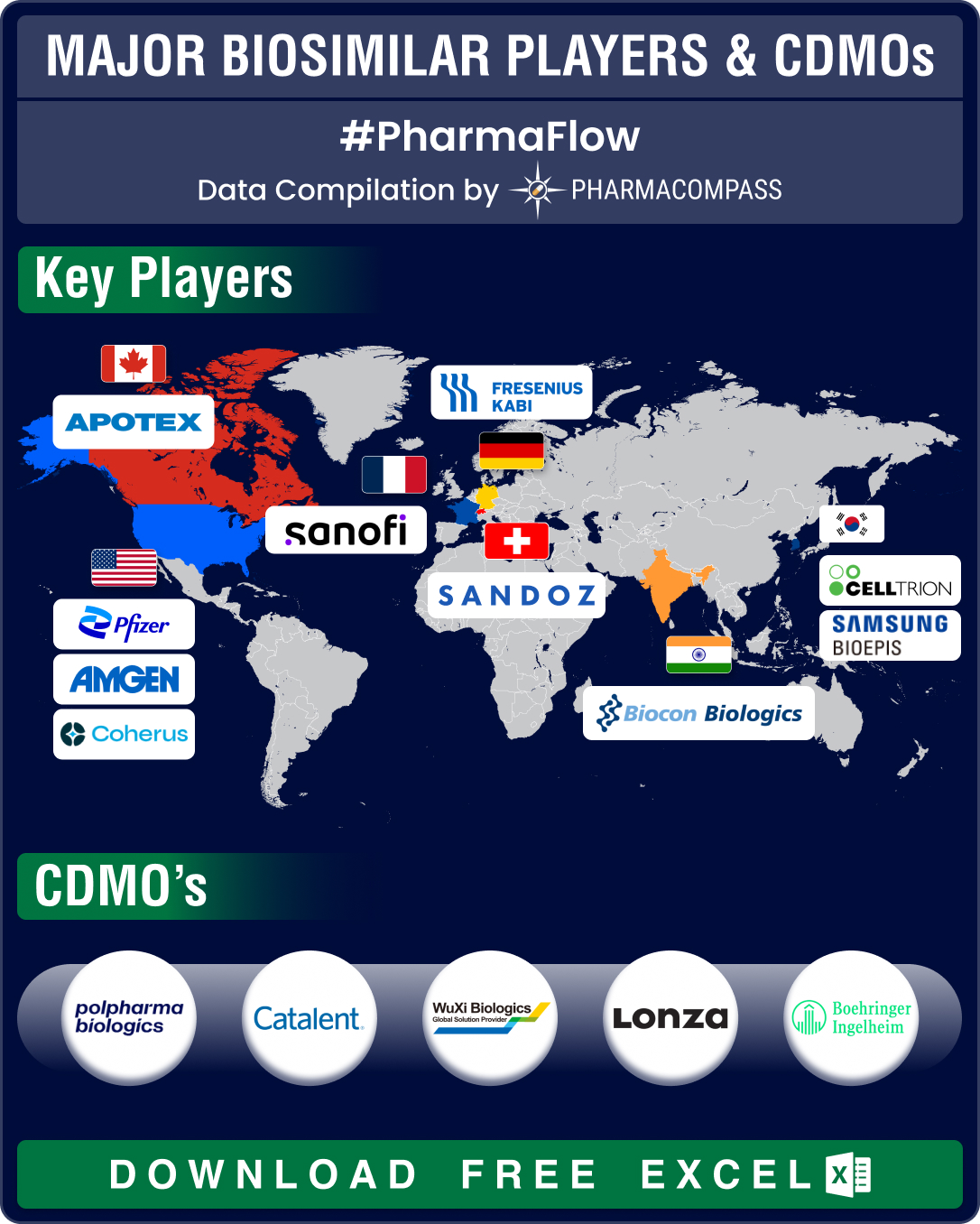

biosimilar players include Amgen, Sandoz, Samsung Bioepis, Pfizer, Biocon Biologics, Celltrion, Stada Arzneimittel, Accord Healthcare, Fresenius Kabi, Coherus Biosciences, Apotex, and Sanofi. The increasing demand for

biosimilars has propelled growth in contract manufacturing. Some of the

leading contract manufacturing organizations (CMOs) and contract development

and manufacturing organizations (CDMOs) that manufacture biosimilars are Polpharma Biologics, Catalent, Pfizer CentreOne, Lonza, Boehringer Ingelheim BioXcellence, Thermo Fisher Scientific, WuXi Biologics, and FUJIFILM Diosynth

Biotechnologies.Access the Interactive Dashboard for Biosimilar Developments (Free Excel)Amgen, Sandoz top list of ‘approved biosimilars’; FDA okays 8 copycats in H1 2024Over

the recent years, regulatory agencies like the FDA

and the European Medicines Agency (EMA) have established rigorous approval pathways for biosimilars.Since 2015, FDA has

approved 53 biosimilars, while the EMA has approved 86 biosimilars. Among the US, European and

Canadian markets, Amgen and Sandoz are tied in the first place

with 13 approved biosimilars each. Samsung Biologics has nine approved

biosimilars, followed by Pfizer with eight and Biocon Biologics with seven. In the first half of this year, FDA set a record by approving eight biosimilars — the highest for H1 of any year. EMA has okayed six biosimilars so far in 2024.In 2023, five biosimilars were approved by the FDA with just one

being okayed in the first half. The year marked the end of exclusivity for Humira after 20 years, in which it

netted a total of US$ 200 billion in sales. AbbVie’s flagship autoimmune drug has a record 10 biosimilars.Johnson & Johnson’s Stelara also lost exclusivity in 2023 and as many as 11

drugmakers hope to bring its biosimilars to the market. Amgen’s Wezlana was the first biosimilar to

Stelara, and it was approved as interchangeable by FDA in October last year.Access the Interactive Dashboard for Biosimilar Developments (Free Excel) FDA approves first

interchangeable biosimilar for Eylea, cuts regulatory feeDeveloping a biosimilar costs both money and time. According to

Pfizer, developing a biosimilar can take five to nine years and cost over US$ 100 million, not including regulatory fees.In October 2023, FDA slashed its fees with the program fee at US$ 177,397, down from US$ 304,162. The application fees for products that require clinical data has been set at US$ 1,018,753, down from US$ 1,746,745. The application fee for products that don’t require clinical data has been set lower — at US$ 509,377 — down from US$ 873,373 set earlier. This reduction in application fee has propelled demand for contract manufacturing of biosimilars.There has also been a rise in approvals of interchangeable

biosimilars this year. Interchangeable biosimilars meet additional requirements

and may be substituted for its reference product by a pharmacist without

consulting the prescriber. This year saw FDA approve the first interchangeable biosimilars for bone cancer

drug denosumab (Prolia and Xgeva) in

Jubbonti and Wyost as well as for eculizumab (Soliris) in Bkemv.In May, FDA approved the first interchangeable biosimilars

for eye drug aflibercept (Eylea) in Opuviz and

Yesafili. Other biosimilars approved in 2024 include Simlandi for adalimumab (Humira), Tyenne for tocilizumab (Actemra), Selarsdi for ustekinumab (Stelara), and Hercessi for trastuzumab (Herceptin).Access the Interactive Dashboard for Biosimilar Developments (Free Excel) Merck’s Keytruda, BMS’ Opdivo, Novartis’ Cosentyx brace for biosimilar competitionHealthcare spending in the US is projected to rise from US$ 4.5

trillion in 2022 to US$ 6 trillion by 2027. While biologics involve just two

percent of prescriptions, they account for 46 percent of all pharmaceutical

spending. In 2022, US$ 252 billion was spent on biologics.Biosimilar-related savings in 2023 were estimated to be US$ 9.4

billion in the US and € 10 billion (US$ 10.68 billion) in Europe. With expensive and widely used drugs like AbbVie’s Humira, J&J’s Stelara, and Regeneron’s Eylea coming under competition, US

savings are projected to reach US$ 181 billion through 2027. Between 2026

and 2032, about 39 blockbusters are set to lose exclusivity in the US and Europe. Merck’s Keytruda (pembrolizumab) was the world’s top-selling drug last year, generating US$ 25 billion in sales. Its patent is set to expire in 2028 with sales expected to drop

19 percent to US$ 27.4 billion in 2029 from US$ 33.7 billion the previous year. Samsung

Bioepis and Amgen initiated phase 3 trials of pembrolizumab in April

and May of this year, respectively.Opdivo (nivolumab), belonging to the same

class of drugs, competes with Keytruda and is also set to lose patent

protection in 2028. It hauled in US$ 10 billion in total global sales in 2023

for Bristol Myers Squibb. The key patents of Novartis’ Cosentyx (secukinumab) are set to expire between

2025 and 2026. Cosentyx saw sales of US$ 5 billion in 2023. Taizhou Mabtech Pharmaceutical and Bio-Thera Solutions are conducting phase 3 trials of secukinumab.Access the Interactive Dashboard for Biosimilar Developments (Free Excel) Our viewWith

over 2 billion people worldwide unable to access life-saving medicines,

biosimilars hold the key to healthcare accessibility. In 2023, a record 13 biosimilars were launched in the market — the highest for a single year. And this included nine much-anticipated biosimilars to AbbVie’s Humira. In April this year, FDA announced a Biosimilars Action Plan to streamline the development of biosimilars. With a sharp focus on biosimilars, we expect more records to be broken in the near term. New launches of biosimilars to drugs like J&J’s Stelara, Regeneron’s Eylea and Merck’s Keytruda will surely help in creating new records.