In 2024, the biopharma industry continued to advance on its robust trajectory of innovation. Though the US Food and Drug Administration’s Center for Drug Evaluation and Research (CDER) and the Center for Biologics Evaluation and Research (CBER) approved fewer drugs, there was a significant increase in medical breakthroughs.While the CDER approved 50 new

drugs in 2024, as compared to 55 in 2023, the CBER granted 14 biologics approvals in 2024, down from 20 in 2023.The European Medicines Agency (EMA) approved 34

new therapies, up from 32 in 2023, while Health Canada granted 28 approvals,

down from 38 in 2023.The year saw long-awaited treatments being approved in areas such as schizophrenia and Alzheimer’s disease in the second half (H2) of 2024. In H1

2024, drugs to treat metabolic dysfunction-associated

steatohepatitis (MASH) and chronic obstructive pulmonary disease (COPD) had

been granted FDA approvals.As the year drew to a close, FDA

began approving drugs at a feverish pace, with 29 of the CDER’s 50 approvals coming in H2.Like most years, the landscape of drug

approvals was dominated by oncology, with 15 of the 50 drugs (30 percent)

approved targeting various forms of cancer. This was followed by dermatology

and non-malignant hematology, each accounting for 12 percent of approvals.

Notably, small molecules continued to dominate the market, making up for 64

percent of the new drug approvals, while 32 percent were proteins, including

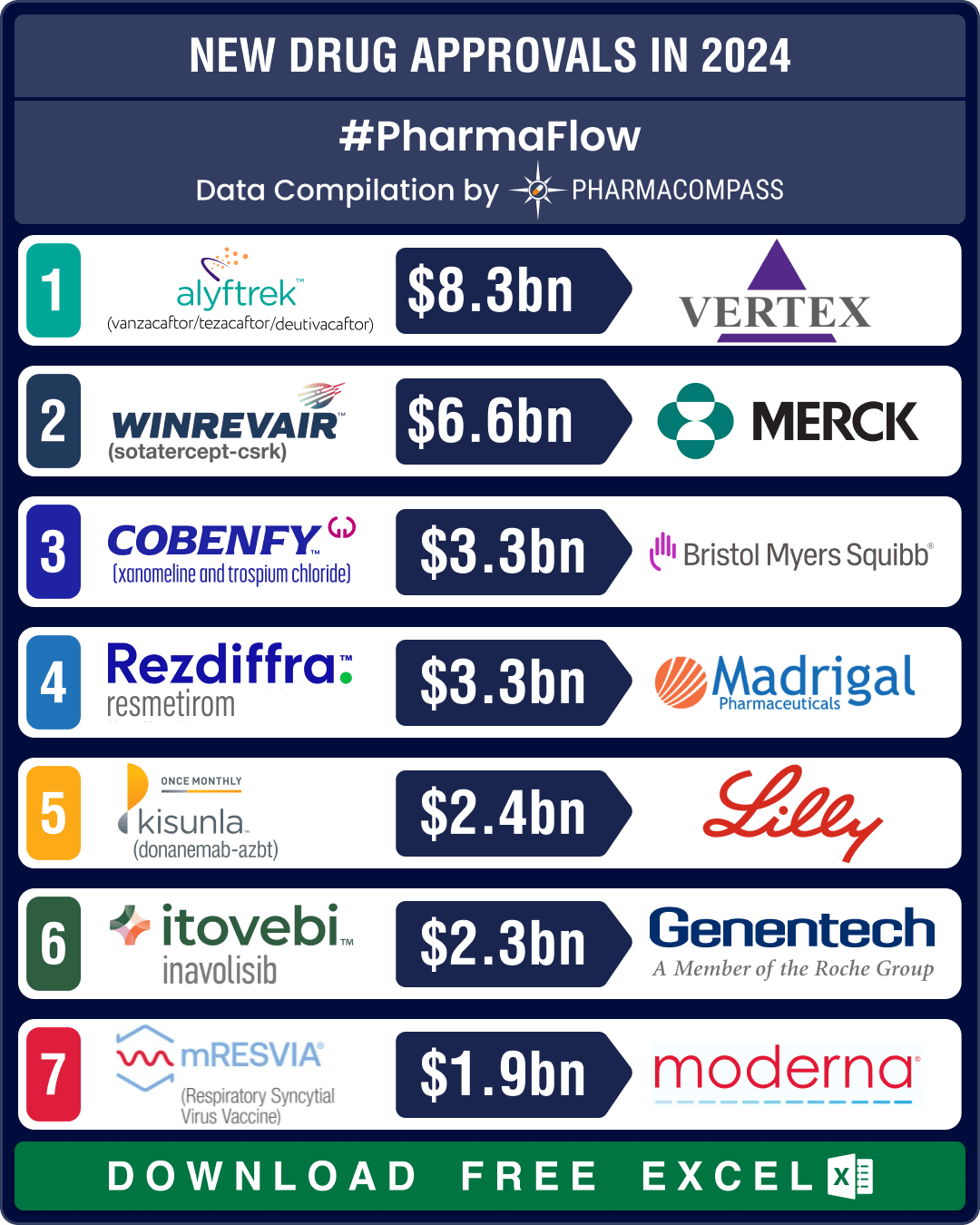

monoclonal and bi-specific antibodies. View New Drug Approvals in 2024 with Estimated Sales (Free Excel Available)Karuna-BMS’ schizophrenia drug, Lilly’s Alzheimer’s med, Neurocrine’s Crenessity dominate list of pathbreaking approvals in H2Out of the 50 new drugs approved in 2024, CDER

identified 24 (48 percent) as first-in-class, showcasing novel mechanisms of

action. The most anticipated approval of 2024 was Karuna and Bristol

Myers Squibb’s Cobenfy, a groundbreaking

treatment for schizophrenia. This fixed-dose combination

of xanomeline and trospium chloride represents the first

novel mechanism of action in decades for this debilitating psychiatric

condition. Analysts forecast peak annual sales of over US$ 3.3 billion for Cobenfy. Eli Lilly’s Alzheimer’s drug Kisunla (donanemab) became

the third amyloid-targeting antibody to gain FDA approval. Unlike

its predecessors, Kisunla offers a

unique limited-duration treatment regimen, allowing

patients to discontinue therapy once amyloid levels in the brain drop below a

certain threshold. Priced at approximately US$ 32,000 per year, it is

positioned as a cost-effective alternative to existing treatments. Analysts

estimate peak sales of US$ 2.4 billion for Kisunla.Crenessity (crinecerfont),

developed by Neurocrine

Biosciences, became the first

FDA-approved treatment in decades for classic

congenital adrenal hyperplasia (genetic conditions that affect the adrenal

glands). Similarly, Vertex’s triple

combination therapy of deutivacaftor, tezacaftor & vanzacaftor

(Alyftrek) for cystic fibrosis represents

a significant advancement in genetic disease

treatment. Analysts forecast peak sales

exceeding US$ 8.3 billion, underscoring the therapy’s potential to transform patient care.Meanwhile, Bridgebio’s Attruby (acoramidis

hydrochloride) emerged as a promising

treatment for cardiac amyloidosis, a life-threatening

condition. View New Drug Approvals in 2024 with Estimated Sales (Free Excel Available) Roche’s Itovebi, Checkpoint’s Unloxcyt clinch FDA approvals in H2 2024; forecast to achieve blockbuster statusThe dominance of cancer drug approvals reflects

the ongoing focus on targeted therapies, immuno-oncology, and precision

medicine to improve outcomes for patients with hard-to-treat cancers.Among the year’s notable FDA

approvals was Genentech’s Itovebi (inavolisib), another targeted therapy that treats hormone receptor-positive (HR+), HER2-negative breast cancer. Itovebi is a PI3Kα inhibitor designed specifically for patients with PIK3CA mutations, a common driver of resistance to endocrine therapy in breast cancer. It demonstrated a more tolerable safety profile. Roche projects Itovebi’s peak (annual) sales to reach CHF 2 billion (US$ 2.3 billion).Checkpoint

Therapeutics’ Unloxcyt (cosibelimab) joined the crowded checkpoint inhibitor market as the eleventh PD-1/PD-L1-targeting monoclonal antibody approved

by the FDA. It was granted approval for cutaneous

squamous cell carcinoma (cSCC), an aggressive form of skin cancer with high

recurrence rates. As compared to other checkpoint inhibitors, like Keytruda (pembrolizumab) and

Opdivo (nivolumab), Unloxcyt is likely to offer an advantage in immune activation.FDA also approved Astellas’ Vyloy

(zolbetuximab), a first-in-class

monoclonal antibody for metastatic gastric and gastroesophageal junction (GEJ)

adenocarcinoma. Analysts forecast peak sales of approximately US$ 850 million for Vyloy.Syndax Pharmaceuticals’ Revuforj (revumenib) was approved

by FDA to treat a type of acute leukemia in both

adults and children. This approval introduces a novel class of medications

known as menin inhibitors. These agents are currently in clinical development

for the treatment of genetically defined subsets of acute leukemia. These

inhibitors function by preventing the activation of cancer growth-related

proteins. View New Drug Approvals in 2024 with Estimated Sales (Free Excel Available) Potential blockbusters Lilly’s Ebglyss, Galderma’s Nemluvio lead advances in dermatologyEli Lilly’s Ebglyss (lebrikizumab) garnered

significant attention. Approved

by FDA for moderate-to-severe atopic dermatitis, this

monoclonal antibody introduces a less burdensome dosing regimen compared to its

competitors, with maintenance therapy required only once a month. This feature

positions it as a potential contender to Dupixent (dupilumab), a

market leader in atopic dermatitis. Ebglyss sales are forecast to reach US$ 1.9 billion by 2030.Galderma’s Nemluvio (nemolizumab) secured FDA

approval for two indications in 2024 — prurigo nodularis (a chronic disorder of the skin) and moderate-to-severe atopic dermatitis in patients aged 12 years and older. As the first humanized IgG2 monoclonal antibody targeting the IL-31 receptor, Nemluvio directly inhibits the key driver of itch and inflammation in both these conditions. With its unique mechanism and broad dermatology potential, analysts forecast peak sales of approximately US$ 1.66 billion. Ebglyss and Nemluvio underscore the growing importance of biologics in dermatological care.Botanix

Pharmaceuticals also made strides in dermatology by

clinching an FDA approval for Sofdra (sofpironium) in June. The drug has been okayed for the treatment of primary axillary hyperhidrosis, a condition characterized by excessive sweating.Ascendis

Pharma’s Yorvipath (palopegteriparatide),

a therapy approved by FDA to

treat hypoparathyroidism, is forecast to achieve

blockbuster sales of US$ 1.8 billion by 2030,

highlighting its potential to transform endocrine care. View New Drug Approvals in 2024 with Estimated Sales (Free Excel Available) Our viewOverall, 2024 was

defined by its breakthrough drug approvals. The year also saw significant reduction in complete response letters (CRLs) — they dropped from 43 in 2023 to just 29 in 2024. This suggests improved industry preparedness and alignment with regulatory expectations.The new year began with the approval of Datroway

(datopotamab deruxtecan) from AstraZeneca and Daiichi

Sankyo, marking a significant advancement in oncology.

Several other promising new drugs are coming up for FDA approval this year,

such as J&J’s nipocalimab, Vertex

Pharmaceuticals’ suzetrigine, Elevar

Therapeutics’ rivoceranib/camrelizumab, Sanofi’s fitusiran and GSK’s gepotidacin. Hopefully, the momentum of breakthrough approvals will continue through 2025, political headwinds in the US notwithstanding.