Latest Content by PharmaCompass

CORPORATE CONTENT #SupplierSpotlight

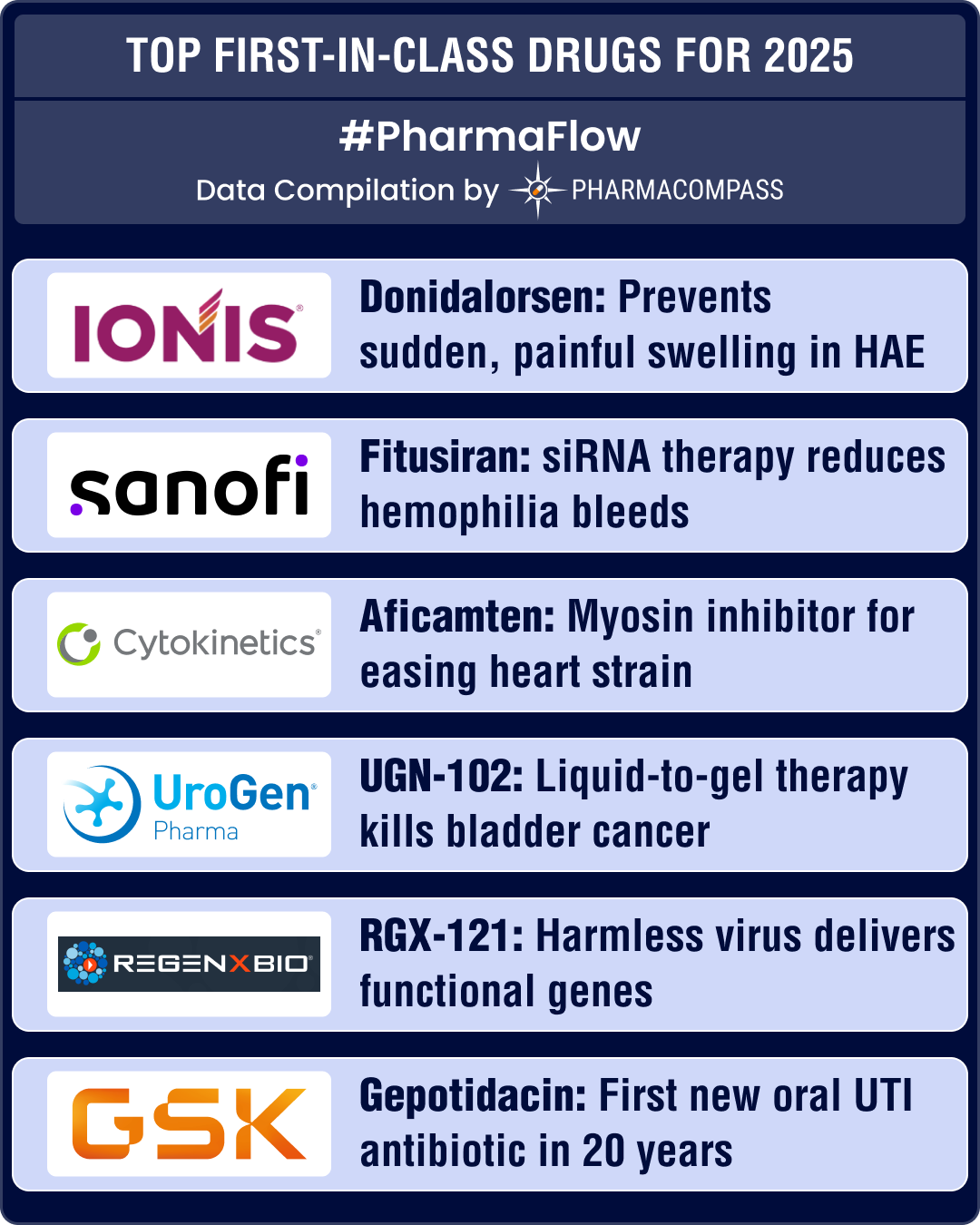

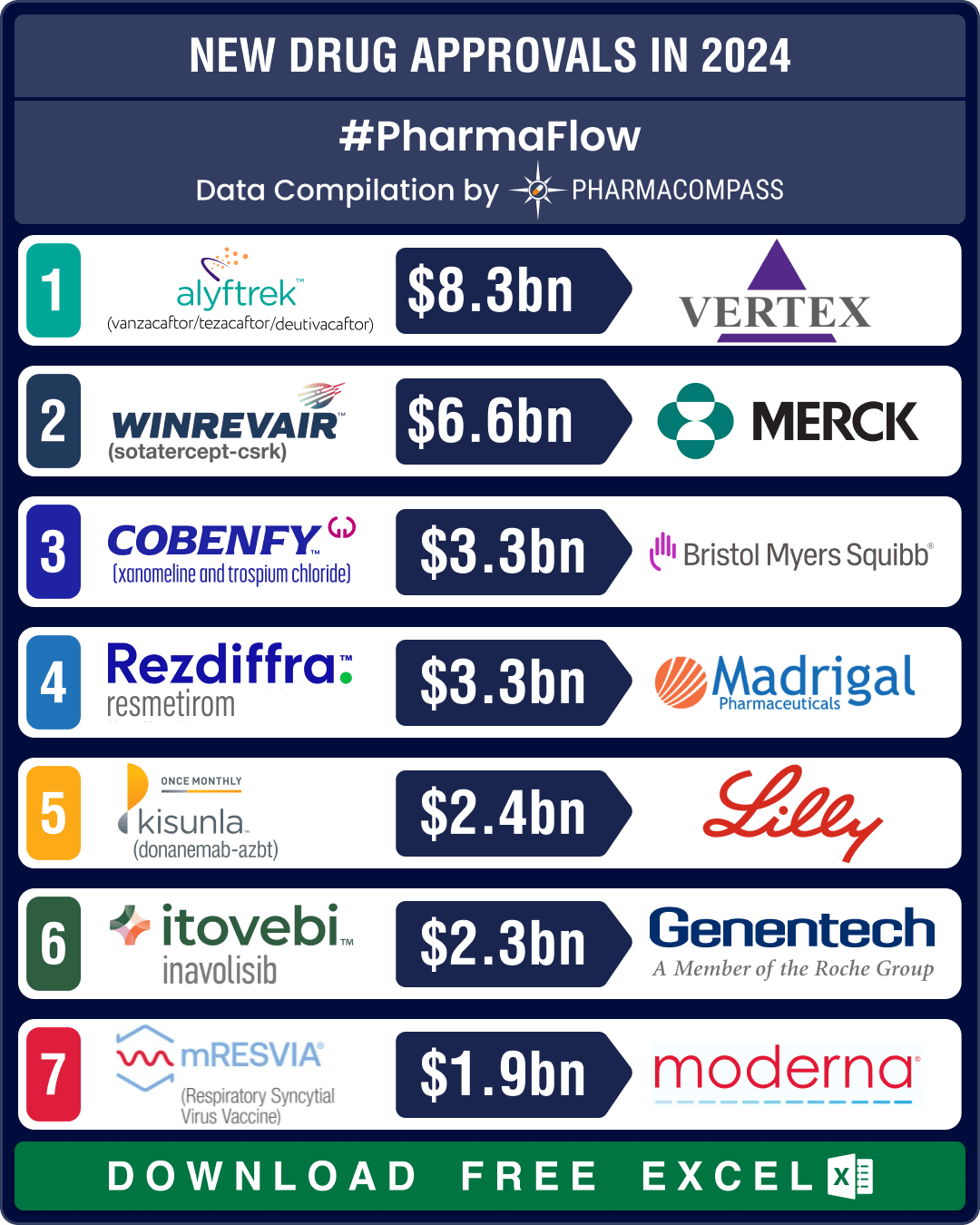

DATA COMPILATION #PharmaFlow

NEWS #PharmaBuzz

11 Apr 2025

// INDPHARMAPOST

08 Apr 2025

// PRESS RELEASE

04 Apr 2025

// PRESS RELEASE

03 Apr 2025

// PRESS RELEASE

01 Apr 2025

// ENDPTS

29 Mar 2025

// PRESS RELEASE

Sanofi is a supplier offers 202 products (APIs, Excipients or Intermediates).

Find a price of Irbesartan bulk with DMF, CEP, JDMF offered by Sanofi

Find a price of Chlorpromazine Hydrochloride bulk with DMF, CEP offered by Sanofi

Find a price of Promethazine Hydrochloride bulk with DMF, CEP offered by Sanofi

Find a price of Zolpidem Tartrate bulk with DMF, CEP offered by Sanofi

Find a price of Clorazepate Dipotassium bulk with CEP offered by Sanofi

Find a price of Trimipramine bulk with CEP offered by Sanofi

Find a price of Zopiclone bulk with CEP offered by Sanofi

Find a price of Acebutolol Hydrochloride bulk offered by Sanofi

Find a price of Alendronate Sodium bulk with CEP offered by Sanofi

Find a price of Alfuzosin HCl bulk with DMF offered by Sanofi

Find a price of Amiodarone Hydrochloride bulk with CEP offered by Sanofi

Find a price of Amisulpride bulk with CEP offered by Sanofi

Find a price of Amlodipine Besylate bulk with CEP offered by Sanofi

Find a price of Avanafil bulk with DMF offered by Sanofi

Find a price of Cabazitaxel bulk with DMF offered by Sanofi

Find a price of Carbaspirin Calcium bulk with CEP offered by Sanofi

Find a price of Ciprofibrate bulk with CEP offered by Sanofi

Find a price of Clopidogrel bulk with DMF offered by Sanofi

Find a price of Divalproex Sodium bulk with CEP offered by Sanofi

Find a price of Docetaxel bulk with CEP offered by Sanofi

Find a price of Dronedarone Hydrochloride bulk with DMF offered by Sanofi

Find a price of Heptaminol bulk with CEP offered by Sanofi

Find a price of Irbesartan bulk with CEP offered by Sanofi

Find a price of Ketoprofen bulk offered by Sanofi

Find a price of Meglumine Antimonate bulk with DMF offered by Sanofi

Find a price of Methylprednisolone Acetate bulk with DMF offered by Sanofi

Find a price of Polio Vaccine bulk with JDMF offered by Sanofi

Find a price of Sodium Hyaluronate bulk with JDMF offered by Sanofi

Find a price of Sodium Valproate bulk with CEP offered by Sanofi

Find a price of Spiramycin bulk offered by Sanofi

Find a price of Thyrotropin-Releasing Hormone bulk offered by Sanofi

Find a price of Tiapride Hydrochloride bulk with CEP offered by Sanofi

Find a price of Ticlopidine bulk with CEP offered by Sanofi

Find a price of SAR441236 bulk with DMF offered by Sanofi

Find a price of Defibrinated sheep blood bulk with CEP offered by Sanofi

Find a price of Citrated Ovine Blood bulk with CEP offered by Sanofi

Find a price of 2-Hydroxymethyl-4-3-Methoxypropoxy-3-Methylpyrid bulk offered by Sanofi

Find a price of 5 6-Dimethoxy-1-Indanone bulk offered by Sanofi

Find a price of 5-Hydroxy Tryptophan bulk offered by Sanofi

Find a price of Acesulfamo bulk offered by Sanofi

Find a price of Alfuzosin HCl bulk offered by Sanofi

Find a price of Alimemazine bulk offered by Sanofi

Find a price of Allethrin bulk offered by Sanofi

Find a price of Alvocidib bulk offered by Sanofi

Find a price of Amisulpride bulk offered by Sanofi

Find a price of Aprotinin bulk offered by Sanofi

Find a price of Artesunate bulk offered by Sanofi

Find a price of Articaine Hydrochloride bulk offered by Sanofi

Find a price of Beclomethasone Dipropionate bulk offered by Sanofi

Find a price of Betamethasone Acetate bulk offered by Sanofi

Find a price of Betaxolol bulk offered by Sanofi

Find a price of Buprenorphine Hydrochloride bulk offered by Sanofi

Find a price of Calcitonin bulk offered by Sanofi

Find a price of CAS 150975-95-4 bulk offered by Sanofi

Find a price of CAS 50-28-2 bulk offered by Sanofi

Find a price of CAS 53-16-7 bulk offered by Sanofi

Find a price of CAS 62063-19-8 bulk offered by Sanofi

Find a price of Chenodeoxycholic Acid bulk offered by Sanofi

Find a price of Chlormezanone bulk offered by Sanofi

Find a price of Chloroquine Phosphate bulk offered by Sanofi

Find a price of Cholesteryl Sodium Sulfate bulk offered by Sanofi

Find a price of Cholic Acid bulk offered by Sanofi

Find a price of Ciramadol bulk offered by Sanofi

Find a price of Clemastine bulk offered by Sanofi

Find a price of Clindamycin Phosphate bulk offered by Sanofi

Find a price of Clopidogrel bulk offered by Sanofi

Find a price of Clotrimazole bulk offered by Sanofi

Find a price of Codeine bulk offered by Sanofi

Find a price of Colchicine bulk offered by Sanofi

Find a price of Cortisone bulk offered by Sanofi

Find a price of Dalteparin sodium bulk offered by Sanofi

Find a price of Daunorubicin HCl bulk offered by Sanofi

Find a price of Deserpidine bulk offered by Sanofi

Find a price of Dextropropoxyphene bulk offered by Sanofi

Find a price of Diatrizoate Sodium bulk offered by Sanofi

Find a price of Dihydroergotamine Mesylate bulk offered by Sanofi

Find a price of Dihydrotachysterol bulk offered by Sanofi

Find a price of Disopyramide bulk offered by Sanofi

Find a price of Dobutamine Hydrochloride bulk offered by Sanofi

Find a price of DPPC bulk offered by Sanofi

Find a price of Eplivanserin Hemifumarate Salt bulk offered by Sanofi

Find a price of Estradiol Valerate bulk offered by Sanofi

Find a price of Ethambutol Dihydrochloride bulk offered by Sanofi

Find a price of Ethinyl Estradiol bulk offered by Sanofi

Find a price of Ethionamide bulk offered by Sanofi

Find a price of Fluprednidene Acetate bulk offered by Sanofi

Find a price of Flurazepam bulk offered by Sanofi

Find a price of Fluticasone Propionate bulk offered by Sanofi

Find a price of Fondaparinux Sodium bulk offered by Sanofi

Find a price of gamma-BHC bulk offered by Sanofi

Find a price of Guaifenesin bulk offered by Sanofi

Find a price of Hematoporphyrin Dihydrochloride bulk offered by Sanofi

Find a price of Hematoporphyrins bulk offered by Sanofi

Find a price of Heparin Sodium bulk offered by Sanofi

Find a price of Hydrochlorothiazide bulk offered by Sanofi

Find a price of Hydrocortisone bulk offered by Sanofi

Find a price of Insulin Lispro bulk offered by Sanofi

Find a price of Iodine bulk offered by Sanofi

Find a price of Isoetharine bulk offered by Sanofi

Find a price of Leuprolide Acetate bulk offered by Sanofi

Find a price of Levonordefrin bulk offered by Sanofi

Find a price of Lidocaine bulk offered by Sanofi

Find a price of Melatonin bulk offered by Sanofi

Find a price of Mephentermine bulk offered by Sanofi

Find a price of Meso-2,3-Dimercaptosuccinic Acid bulk offered by Sanofi

Find a price of Mestranol bulk offered by Sanofi

Find a price of Methadone Hydrochloride bulk offered by Sanofi

Find a price of Methyl Testosterone bulk offered by Sanofi

Find a price of Methylprednisolone Hemisuccinate bulk offered by Sanofi

Find a price of Metronidazole bulk offered by Sanofi

Find a price of Minaprine bulk offered by Sanofi

Find a price of Nalmefene Hydrochloride bulk offered by Sanofi

Find a price of Nedocromil Sodium bulk offered by Sanofi

Find a price of Neomycin Sulfate bulk offered by Sanofi

Find a price of Norandrostenedione bulk offered by Sanofi

Find a price of Norelgestromin bulk offered by Sanofi

Find a price of Norethisterone bulk offered by Sanofi

Find a price of Norethisterone Acetate bulk offered by Sanofi

Find a price of Norgestimate bulk offered by Sanofi

Find a price of Octoxynol bulk offered by Sanofi

Find a price of Omeprazole bulk offered by Sanofi

Find a price of Oxybutynin Hydrochloride bulk offered by Sanofi

Find a price of Paracetamol bulk offered by Sanofi

Find a price of Pentamidine Isethionate bulk offered by Sanofi

Find a price of Phospholipon Mc bulk offered by Sanofi

Find a price of POPC bulk offered by Sanofi

Find a price of Prochlorperazine Edisylate bulk offered by Sanofi

Find a price of Promazine bulk offered by Sanofi

Find a price of Propionylpromazine bulk offered by Sanofi

Find a price of Propyphenazone bulk offered by Sanofi

Find a price of Pyrazinamide bulk offered by Sanofi

Find a price of R-Zacopride bulk offered by Sanofi

Find a price of Rifampicin bulk offered by Sanofi

Find a price of Rifamycin Sodium bulk offered by Sanofi

Find a price of Rimonabant bulk offered by Sanofi

Find a price of Salicylic Acid bulk offered by Sanofi

Find a price of Saredutant Succinate bulk offered by Sanofi

Find a price of Satavaptan Phosphate bulk offered by Sanofi

Find a price of Sodium Cromoglicate bulk offered by Sanofi

Find a price of Streptomycin bulk offered by Sanofi

Find a price of Suproclone bulk offered by Sanofi

Find a price of Suriclone bulk offered by Sanofi

Find a price of Teicoplanin bulk offered by Sanofi

Find a price of Testosterone bulk offered by Sanofi

Find a price of Testosterone Cypionate bulk offered by Sanofi

Find a price of Testosterone Enanthate bulk offered by Sanofi

Find a price of Testosterone Propionate bulk offered by Sanofi

Find a price of Tetrazepam bulk offered by Sanofi

Find a price of Tiludronic Acid bulk offered by Sanofi

Find a price of Triamcinolone bulk offered by Sanofi

Find a price of Triamcinolone Acetonide bulk offered by Sanofi

Find a price of Triamcinolone Diacetate bulk offered by Sanofi

Find a price of Triamcinolone Hexacetonide bulk offered by Sanofi

Find a price of Triamterene bulk offered by Sanofi

Find a price of Trifluoperazine Hydrochloride bulk offered by Sanofi

Find a price of Trimegestone bulk offered by Sanofi

Find a price of Triprolidine Hydrochloride bulk offered by Sanofi

Find a price of Tyropanoate bulk offered by Sanofi

Find a price of Verapamil Hydrochloride bulk offered by Sanofi

Find a price of Vitamin B12 bulk offered by Sanofi

Find a price of HYDROXY ACID bulk offered by Sanofi

Find a price of FACILITIES UTILIZED IN MONTPELLIER, FRANCE bulk offered by Sanofi

Find a price of MANUF RESCH AND PERSONNEL FILE RSCH FACILS, EQUIPMENT & CONTROLS 11-16 bulk offered by Sanofi

Find a price of MANUFACTURING SITE, FACILITIES, PERSONNEL, AND GENERAL OPERATING PROCEDURES OF 5,6-DIMETHOXY-1-INDANONE bulk offered by Sanofi

Find a price of MANUFACTURING SITE, FACILITIES, PERSONNEL, AND GENERAL OPERATING PROCEDURES IN FAWDON, NEWCASTLE TYNE NE3 3TT, ENGLAND. bulk offered by Sanofi

Find a price of BEFLOXATONE bulk offered by Sanofi

Find a price of HEMATOROPHYRINE DIHYDROCHLORIDE,PACKAGED AND TESTED IN VERTOLAYE,FRANCE bulk offered by Sanofi

Find a price of PEGYLATED RECOMBINANT ANTI-PSEUDOMONAS AERUGINOSA PCRV FAB' ANTIBODY (KB001-A) DRUG SUBSTANCE bulk offered by Sanofi

Find a price of MANUFACTURING SITE, FACILITIES, PERSONNEL, AND GENERAL OPERATING PROCEDURES IN LIESTAL, SWITZERLAND. bulk offered by Sanofi

Find a price of NORTON PLASTIC S-500-304 bulk offered by Sanofi

Find a price of ADENO-ASSOCIATED VIRUS (AAV) VECTOR CONTAINING THE GENE FOR HUMAN BLOOD COAGULATION FACTOR IX (COAGULIN-B) bulk offered by Sanofi

Find a price of ELS(ELASTASE) bulk offered by Sanofi

Find a price of MANUFACTURING FACILITIES AT NOTRE DAME DE BONDEVILLE, FRANCE bulk offered by Sanofi

Find a price of 1-PALMITOYL-2-OLEOYL-SN-GLYCERO-3-PHOSPHOGLYCEROL, AMMONIUM SALT (POPG, NH4) bulk offered by Sanofi

Find a price of FACILITIES LOCATED IN SISTERON, FRNACE bulk offered by Sanofi

Find a price of MANUFACTURING SITE, FACILITIES, PERSONNEL, AND GENERAL OPERATING PROCEDURES IN ARAMON. bulk offered by Sanofi

Find a price of MANUFACTURING SITE, FACILITIES, PERSONNEL, AND GENERAL OPERATING PROCEDURES IN LABEGE CEDEX, FRANCE bulk offered by Sanofi

Find a price of 1-(A-HYDROXYETHYL)-2-METHYL-5-NITRO-IMIDAZOLE,A NEW TRICHOMONOCIDE bulk offered by Sanofi

Find a price of SR 27417A bulk offered by Sanofi

Find a price of MANUFACTURING SITE, FACILITIES, PERSONNEL, AND GENERAL OPERATING PROCEDURES IN TOULOUSE, FRANCE. bulk offered by Sanofi

Find a price of SEMULOPARIN SODIUM bulk offered by Sanofi

Find a price of CERAMIDETRIHEXOSIDASE bulk offered by Sanofi

Find a price of MDL 104036 bulk offered by Sanofi

Find a price of FACILITY LOCATED IN SISTERON, FRANCE bulk offered by Sanofi

Find a price of CONTRACT PACKAGING OPERATIONS ONLY, LOCATED IN FENTON, MO bulk offered by Sanofi

Find a price of METHYLOXINE BROMOMETHYLOXINE METHYLOXINE N-DODECYLSULFATE bulk offered by Sanofi

Find a price of MANUFACTURING SITE, FACILITIES, PERSONNEL AND GENERAL OPERATING PROCEDURES IN AMBARES, FRANCE. bulk offered by Sanofi

Find a price of MDL 101,731 bulk offered by Sanofi

Find a price of PEGYLATED RECOMBINANT ANIT-PSEUDOMONAS AERUGINOSA PCRV FAB' ANTIBODY (KB001-A) DRUG PRODUCT bulk offered by Sanofi

Find a price of MANUFACTURING SITE, FACILITIES, PERSONNEL AND GENERAL OPERATING PROCEDURES AT COLLEGEVIEW, PA bulk offered by Sanofi

Find a price of FACILITIES, PERSONNEL AND GENERAL OPERATING PROCEDURES AT BUDAPEST, HUNGARY bulk offered by Sanofi

Find a price of MANUFACTURING FACILITIES AND CONTROLS bulk offered by Sanofi

Find a price of SPIROMETHYL-BIPHENYL-NITRILE (SR47563) bulk offered by Sanofi

Find a price of MDL 105074 bulk offered by Sanofi

Find a price of Apomorphine Hydrochloride bulk offered by Sanofi

Find a price of Grape Seed Extract bulk offered by Sanofi

Find a price of Hydroxocobalamin bulk offered by Sanofi

Find a price of Hydroxocobalamin Acetate bulk offered by Sanofi

Find a price of Nalbuphine Hydrochloride bulk offered by Sanofi

Find a price of Naloxone Hydrochloride bulk offered by Sanofi

Find a price of Naltrexone Hydrochloride bulk offered by Sanofi

Find a price of Trenbolone Acetate bulk offered by Sanofi