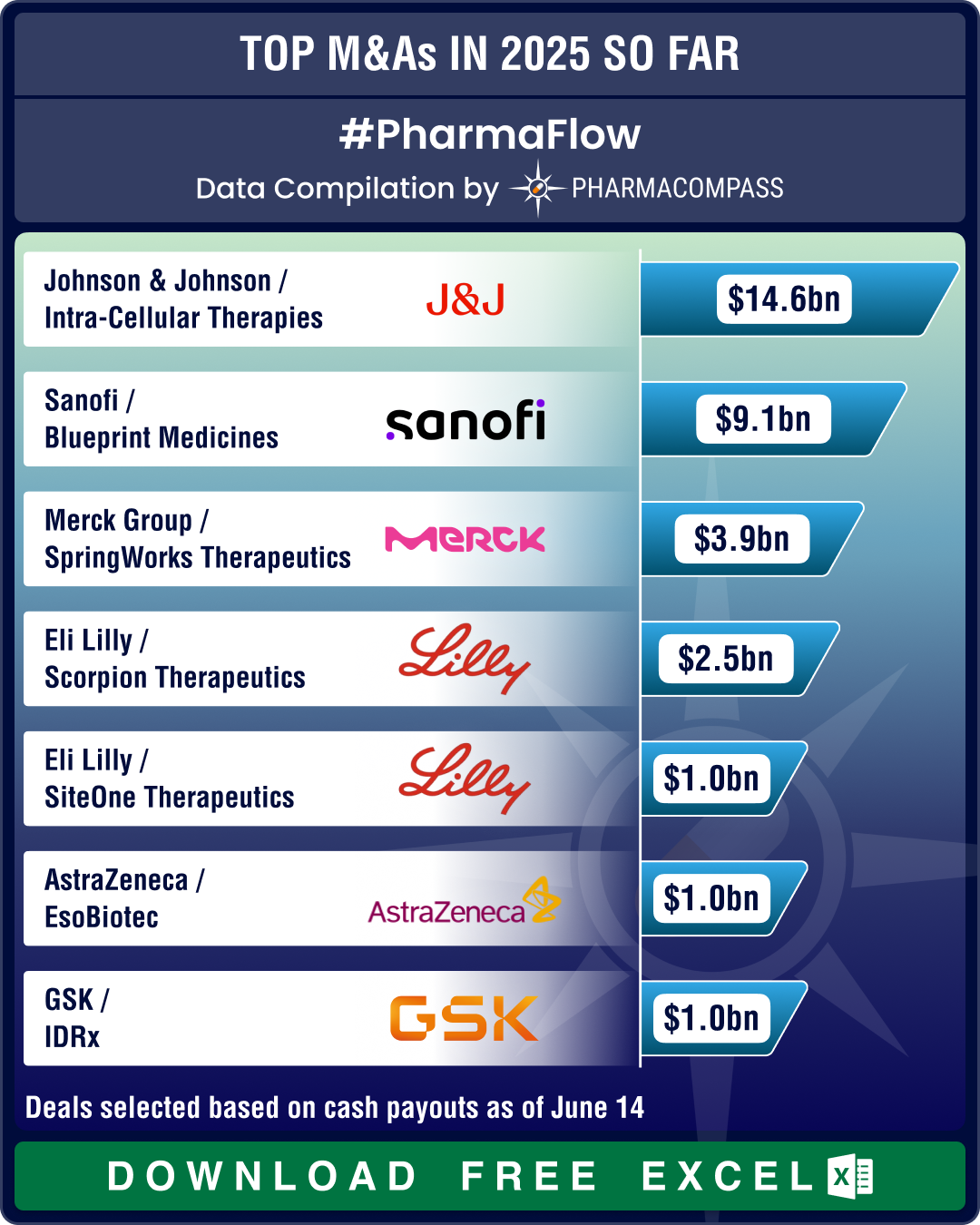

J&J’s Intra‑Cellular buyout, BMS’ oncology gambit, Sanofi’s Blueprint acquisition drive mega deals in H1 2025

The pharmaceutical industry has witnessed a wave of mergers, acquisitions, and strategic partnership

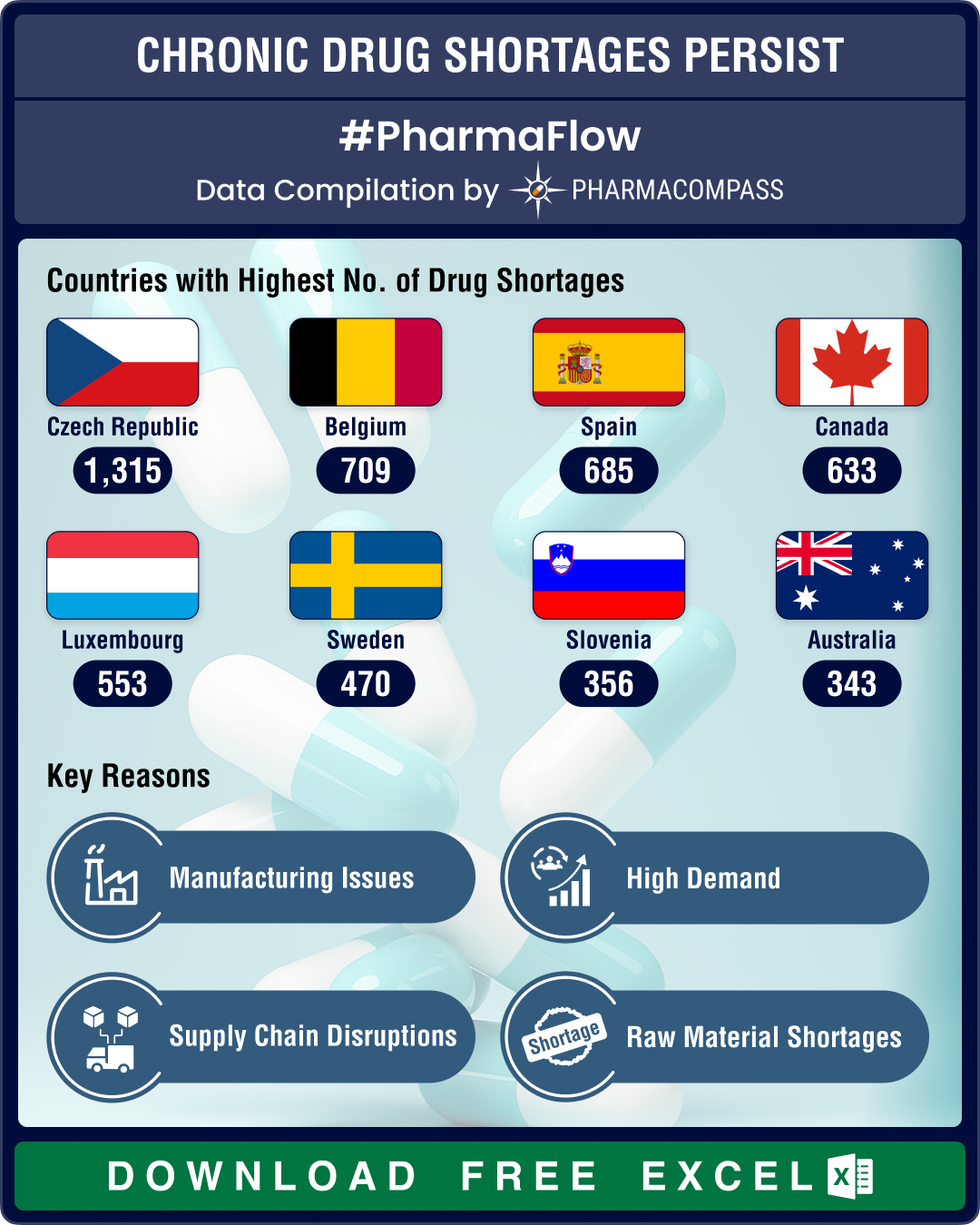

US drug shortages reduce 16% YoY in Q1 2025; CNS drugs, antimicrobials face highest scarcities

The pharmaceutical industry in the United States continued to

grapple with drug shortages during th

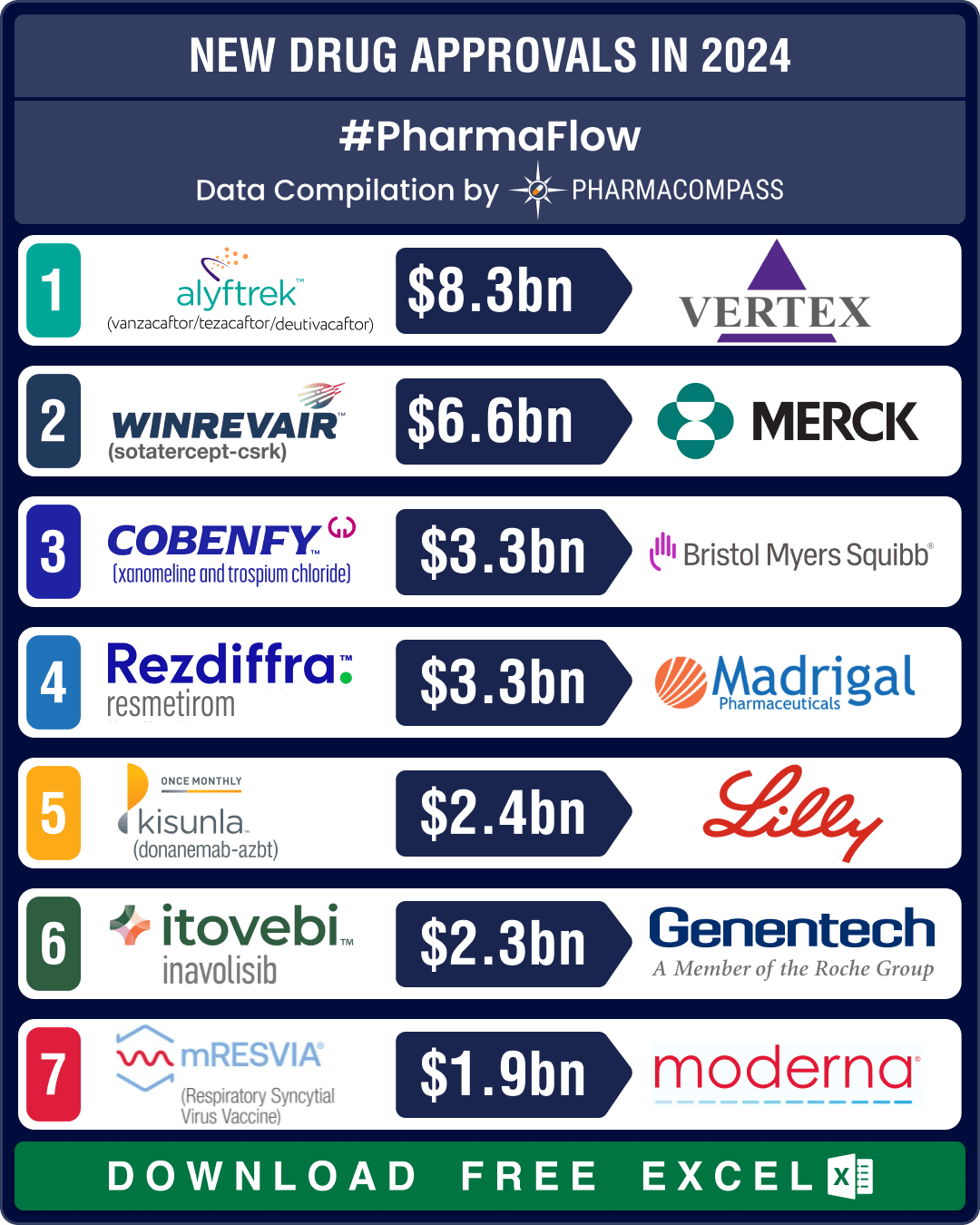

FDA okays 50 new drugs in 2024; BMS’ Cobenfy, Lilly’s Kisunla lead pack of breakthrough therapies

In 2024, the biopharma industry continued to advance on its robust trajectory of innovation. Though

FDA’s landmark approvals of BMS’ schizo med, Madrigal’s MASH drug, US$ 16.5 bn Catalent buyout make it to top 10 news of 2024

The year 2024 was marked by some landmark drug approvals in the areas of schizophrenia, metabolic dy

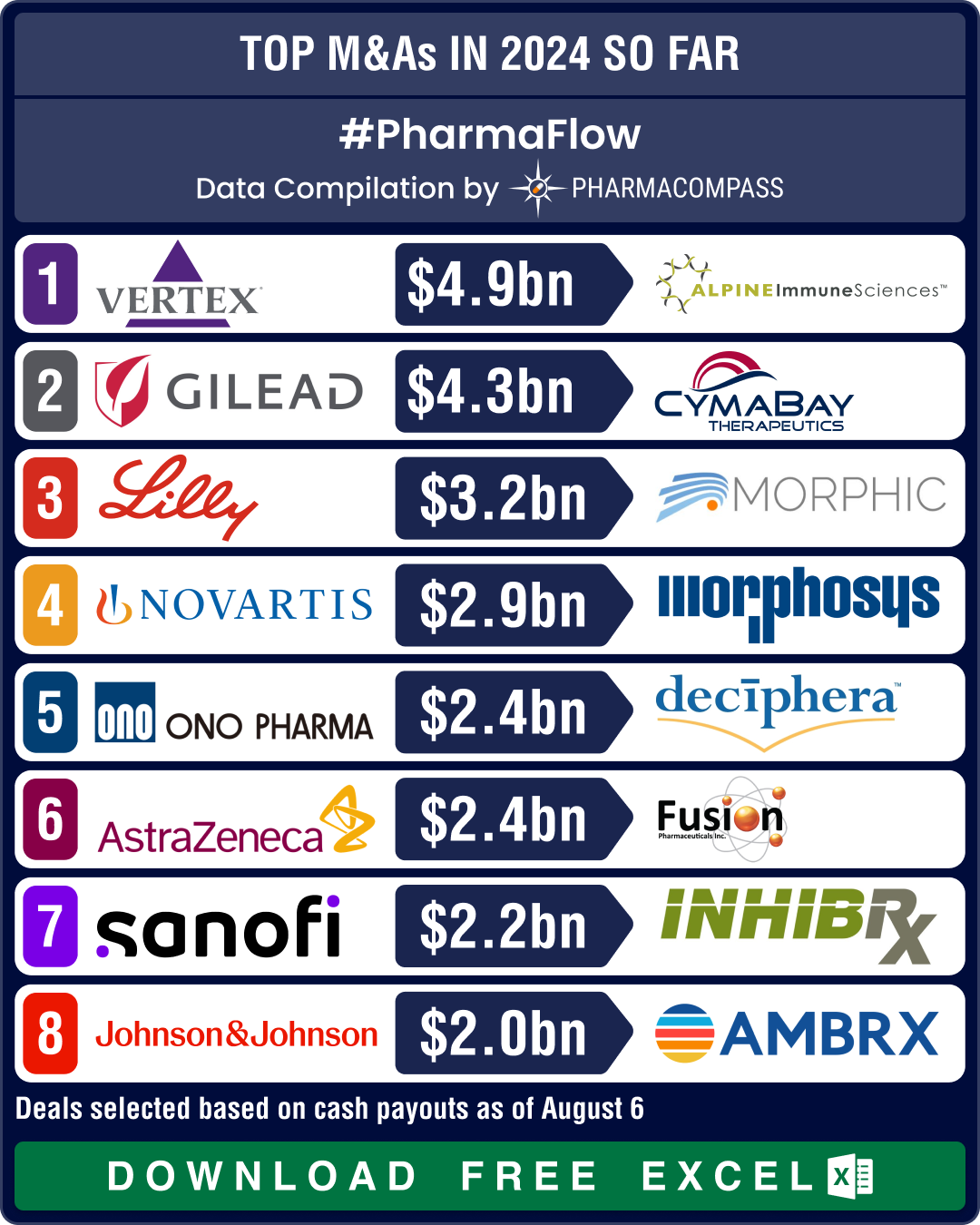

Novartis, GSK, Sanofi, BMS shell out over US$ 10 bn in dealmaking, as mid-size deals take centerstage in 2024

The world of pharmaceuticals and biotechnology continued to evolve

this year with strategic allianc

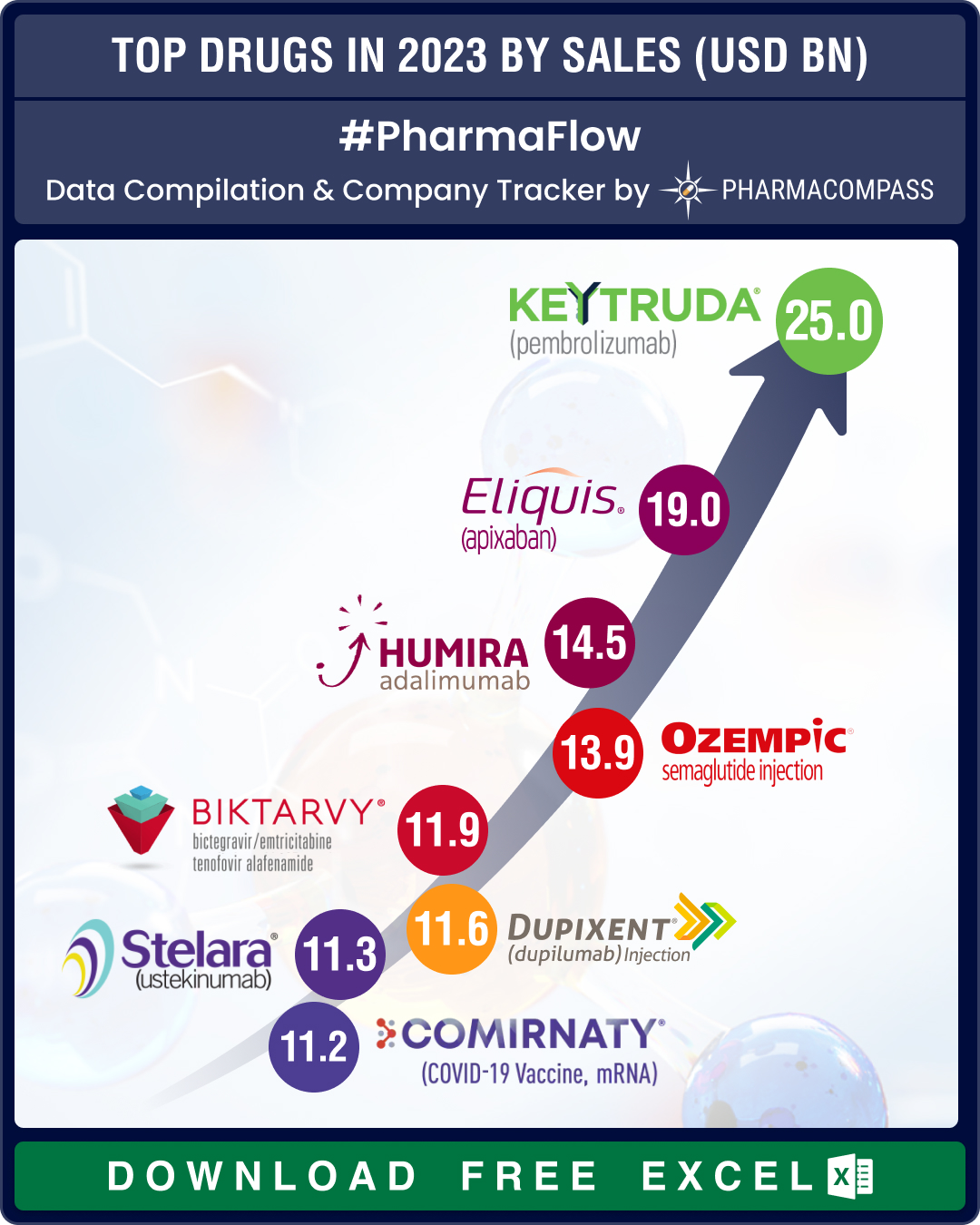

Top Pharma Companies & Drugs in 2023: Merck’s Keytruda emerges as top-selling drug; Novo, Lilly sales skyrocket

The pharma industry clearly recalibrated itself in 2023, turning its focus away from Covid and onto

- Privacy policy

- Terms and conditions

- Disclaimers

-

- Product listings are provided for informational purposes only. We do not supply or sell any products. Any products that may be covered by patent(s) are supplied solely for uses permitted under Section 107A of the Indian Patents Act and not for commercial sale.