Biologics, or complex drugs that are derived from living organisms, have revolutionized treatment of various conditions such as cancer, autoimmune diseases, and chronic illnesses. In 2023, eight out of 10 of the world’s top-selling drugs were biologics, including Merck’s Keytruda, AbbVie’s Humira, and Sanofi’s Dupixent.Due to their high costs, accessibility of biologics has been a challenge. That’s why biosimilars, or game-changing copycats of biologics that provide highly similar yet more affordable alternatives to established biologics, are becoming popular.The first biosimilar — Sandoz’ Zarxio — was approved by the US Food and Drug Administration (FDA) in 2015. Its reference biologic was Amgen’s Neupogen (filgrastim). Since then, the global market for biosimilars has been growing at an impressive pace — between 2015 and 2020, it grew at a whopping compounded annual growth rate (CAGR) of 78 percent, touching US$ 17.9 billion in size. It is expected to continue growing at a CAGR of 15 percent and reach a size of about US$ 75 billion by 2030.Major

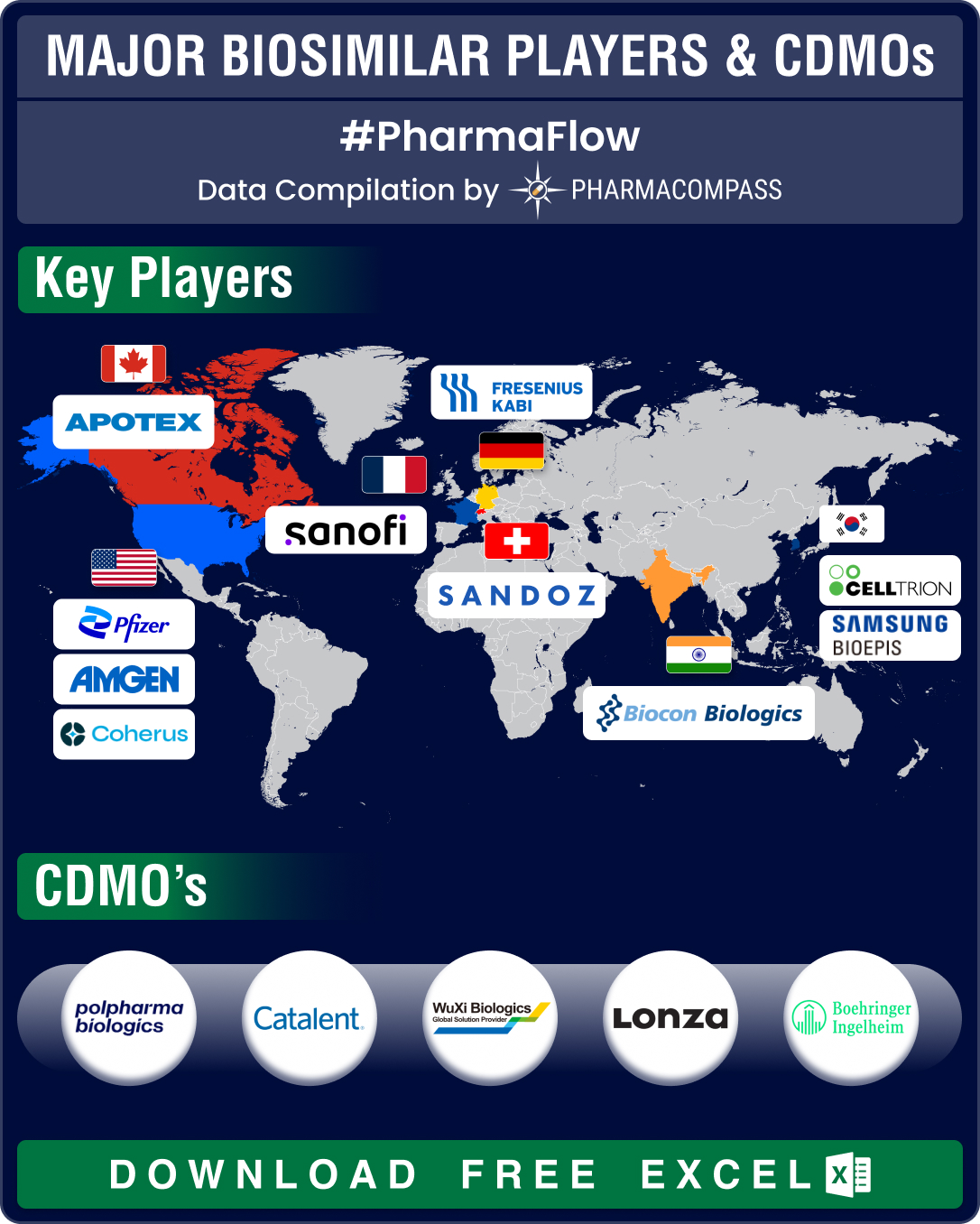

biosimilar players include Amgen, Sandoz, Samsung Bioepis, Pfizer, Biocon Biologics, Celltrion, Stada Arzneimittel, Accord Healthcare, Fresenius Kabi, Coherus Biosciences, Apotex, and Sanofi. The increasing demand for

biosimilars has propelled growth in contract manufacturing. Some of the

leading contract manufacturing organizations (CMOs) and contract development

and manufacturing organizations (CDMOs) that manufacture biosimilars are Polpharma Biologics, Catalent, Pfizer CentreOne, Lonza, Boehringer Ingelheim BioXcellence, Thermo Fisher Scientific, WuXi Biologics, and FUJIFILM Diosynth

Biotechnologies.Access the Interactive Dashboard for Biosimilar Developments (Free Excel)Amgen, Sandoz top list of ‘approved biosimilars’; FDA okays 8 copycats in H1 2024Over

the recent years, regulatory agencies like the FDA

and the European Medicines Agency (EMA) have established rigorous approval pathways for biosimilars.Since 2015, FDA has

approved 53 biosimilars, while the EMA has approved 86 biosimilars. Among the US, European and

Canadian markets, Amgen and Sandoz are tied in the first place

with 13 approved biosimilars each. Samsung Biologics has nine approved

biosimilars, followed by Pfizer with eight and Biocon Biologics with seven. In the first half of this year, FDA set a record by approving eight biosimilars — the highest for H1 of any year. EMA has okayed six biosimilars so far in 2024.In 2023, five biosimilars were approved by the FDA with just one

being okayed in the first half. The year marked the end of exclusivity for Humira after 20 years, in which it

netted a total of US$ 200 billion in sales. AbbVie’s flagship autoimmune drug has a record 10 biosimilars.Johnson & Johnson’s Stelara also lost exclusivity in 2023 and as many as 11

drugmakers hope to bring its biosimilars to the market. Amgen’s Wezlana was the first biosimilar to

Stelara, and it was approved as interchangeable by FDA in October last year.Access the Interactive Dashboard for Biosimilar Developments (Free Excel) FDA approves first

interchangeable biosimilar for Eylea, cuts regulatory feeDeveloping a biosimilar costs both money and time. According to

Pfizer, developing a biosimilar can take five to nine years and cost over US$ 100 million, not including regulatory fees.In October 2023, FDA slashed its fees with the program fee at US$ 177,397, down from US$ 304,162. The application fees for products that require clinical data has been set at US$ 1,018,753, down from US$ 1,746,745. The application fee for products that don’t require clinical data has been set lower — at US$ 509,377 — down from US$ 873,373 set earlier. This reduction in application fee has propelled demand for contract manufacturing of biosimilars.There has also been a rise in approvals of interchangeable

biosimilars this year. Interchangeable biosimilars meet additional requirements

and may be substituted for its reference product by a pharmacist without

consulting the prescriber. This year saw FDA approve the first interchangeable biosimilars for bone cancer

drug denosumab (Prolia and Xgeva) in

Jubbonti and Wyost as well as for eculizumab (Soliris) in Bkemv.In May, FDA approved the first interchangeable biosimilars

for eye drug aflibercept (Eylea) in Opuviz and

Yesafili. Other biosimilars approved in 2024 include Simlandi for adalimumab (Humira), Tyenne for tocilizumab (Actemra), Selarsdi for ustekinumab (Stelara), and Hercessi for trastuzumab (Herceptin).Access the Interactive Dashboard for Biosimilar Developments (Free Excel) Merck’s Keytruda, BMS’ Opdivo, Novartis’ Cosentyx brace for biosimilar competitionHealthcare spending in the US is projected to rise from US$ 4.5

trillion in 2022 to US$ 6 trillion by 2027. While biologics involve just two

percent of prescriptions, they account for 46 percent of all pharmaceutical

spending. In 2022, US$ 252 billion was spent on biologics.Biosimilar-related savings in 2023 were estimated to be US$ 9.4

billion in the US and € 10 billion (US$ 10.68 billion) in Europe. With expensive and widely used drugs like AbbVie’s Humira, J&J’s Stelara, and Regeneron’s Eylea coming under competition, US

savings are projected to reach US$ 181 billion through 2027. Between 2026

and 2032, about 39 blockbusters are set to lose exclusivity in the US and Europe. Merck’s Keytruda (pembrolizumab) was the world’s top-selling drug last year, generating US$ 25 billion in sales. Its patent is set to expire in 2028 with sales expected to drop

19 percent to US$ 27.4 billion in 2029 from US$ 33.7 billion the previous year. Samsung

Bioepis and Amgen initiated phase 3 trials of pembrolizumab in April

and May of this year, respectively.Opdivo (nivolumab), belonging to the same

class of drugs, competes with Keytruda and is also set to lose patent

protection in 2028. It hauled in US$ 10 billion in total global sales in 2023

for Bristol Myers Squibb. The key patents of Novartis’ Cosentyx (secukinumab) are set to expire between

2025 and 2026. Cosentyx saw sales of US$ 5 billion in 2023. Taizhou Mabtech Pharmaceutical and Bio-Thera Solutions are conducting phase 3 trials of secukinumab.Access the Interactive Dashboard for Biosimilar Developments (Free Excel) Our viewWith

over 2 billion people worldwide unable to access life-saving medicines,

biosimilars hold the key to healthcare accessibility. In 2023, a record 13 biosimilars were launched in the market — the highest for a single year. And this included nine much-anticipated biosimilars to AbbVie’s Humira. In April this year, FDA announced a Biosimilars Action Plan to streamline the development of biosimilars. With a sharp focus on biosimilars, we expect more records to be broken in the near term. New launches of biosimilars to drugs like J&J’s Stelara, Regeneron’s Eylea and Merck’s Keytruda will surely help in creating new records.

Impressions: 1504

https://www.pharmacompass.com/radio-compass-blog/fda-approves-record-eight-biosimilars-in-h1-2024-okays-first-interchangeable-biosimilars-for-eylea

#PharmaFlow by PHARMACOMPASS

27 Jun 2024

Acquisitions and spin-offs dominated headlines in 2019 and the tone was set very early with Bristol-Myers Squibb acquiring

New Jersey-based cancer drug company Celgene in a US$ 74 billion deal announced on

January 3, 2019. After factoring

in debt, the deal value ballooned to about US$ 95 billion, which according

to data compiled by Refinitiv, made it the largest healthcare deal on

record.

In the summer, AbbVie Inc,

which sells the world’s best-selling drug Humira, announced its acquisition of Allergan Plc, known for Botox and other cosmetic

treatments, for US$ 63 billion. While the companies are still awaiting

regulatory approval for their deal, with US$ 49 billion in combined 2019

revenues, the merged entity would rank amongst the biggest in the industry.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

The big five by pharmaceutical sales — Pfizer,

Roche, J&J, Novartis and Merck

Pfizer

continued

to lead companies by pharmaceutical sales by reporting annual 2019 revenues of

US$ 51.8 billion, a decrease of US$ 1.9 billion, or 4 percent, compared to

2018. The decline was primarily attributed to the loss of exclusivity of Lyrica in 2019,

which witnessed its sales drop from US$ 5 billion in 2018 to US$ 3.3 billion in

2019.

In 2018, Pfizer’s then incoming CEO Albert Bourla had mentioned that the company did not see the need for any large-scale M&A activity as Pfizer had “the best pipeline” in its history, which needed the company to focus on deploying its capital to keep its pipeline flowing and execute on its drug launches.

Bourla stayed true to his word and barring the acquisition of Array Biopharma for US$ 11.4 billion and a spin-off to merge Upjohn, Pfizer’s off-patent branded and generic established medicines business with

Mylan, there weren’t any other big ticket deals which were announced.

The

Upjohn-Mylan merged entity will be called Viatris and is expected to have 2020

revenues between US$ 19 and US$ 20 billion

and could outpace Teva to

become the largest generic company in the world, in term of revenues.

Novartis, which had

followed Pfizer with the second largest revenues in the pharmaceutical industry

in 2018, reported its first full year earnings after spinning off its Alcon eye

care devices business division that

had US$ 7.15 billion in 2018 sales.

In 2019,

Novartis slipped two spots in the ranking after reporting total sales of US$

47.4 billion and its CEO Vas Narasimhan continued his deal-making spree by buying New

Jersey-headquartered The Medicines Company (MedCo) for US$ 9.7

billion to acquire a late-stage cholesterol-lowering

therapy named inclisiran.

As Takeda Pharmaceutical Co was

busy in 2019 on working to reduce its debt burden incurred due to its US$ 62

billion purchase of Shire Plc, which was announced in 2018, Novartis also purchased

the eye-disease medicine, Xiidra, from the Japanese drugmaker for US$ 5.3 billion.

Novartis’ management also spent a considerable part of 2019 dealing with data-integrity concerns which emerged from its 2018 buyout of AveXis, the

gene-therapy maker Novartis had acquired for US$ 8.7 billion.

The deal gave Novartis rights to Zolgensma,

a novel treatment intended for children less than two years of age with the

most severe form of spinal muscular atrophy (SMA). Priced at US$ 2.1 million,

Zolgensma is currently the world’s most expensive drug.

However,

in a shocking announcement, a month after approving the drug, the US Food and

Drug Administration (FDA) issued a press release on

data accuracy issues as the agency was informed by AveXis that

its personnel had manipulated data which

the FDA used to evaluate product comparability and nonclinical (animal)

pharmacology as part of the biologics license application (BLA), which was

submitted and reviewed by the FDA.

With US$

50.0 billion (CHF 48.5 billion) in annual pharmaceutical sales, Swiss drugmaker

Roche came in at number two position in 2019

as its sales grew 11 percent driven by

its multiple sclerosis medicine Ocrevus, haemophilia drug Hemlibra and cancer medicines Tecentriq and Perjeta.

Roche’s newly introduced medicines generated US$ 5.53 billion (CHF 5.4 billion) in growth, helping offset the impact of the competition from biosimilars for its three best-selling drugs MabThera/Rituxan, Herceptin and Avastin.

In late 2019, after months of increased

antitrust scrutiny, Roche completed

its US$ 5.1 billion acquisition of Spark Therapeutics to strengthen its presence in

gene therapy.

Last year, J&J reported almost flat worldwide sales of US$ 82.1 billion. J&J’s pharmaceutical division generated US$ 42.20 billion and its medical devices and consumer health divisions brought in US$ 25.96 billion and US$ 13.89 billion respectively.

Since J&J’s consumer health division sells analgesics, digestive health along with beauty and oral care products, the US$ 5.43 billion in consumer health sales from over-the-counter drugs and women’s health products was only used in our assessment of J&J’s total pharmaceutical revenues. With combined pharmaceutical sales of US$ 47.63 billion, J&J made it to number three on our list.

While the sales of products like Stelara, Darzalex, Imbruvica, Invega Sustenna drove J&J’s pharmaceutical business to grow by 4 percent over 2018, the firm had to contend with generic competition against key revenue contributors Remicade and Zytiga.

US-headquartered Merck, which is known as

MSD (short for Merck Sharp & Dohme) outside the United States and

Canada, is set to significantly move up the rankings next year fueled by its

cancer drug Keytruda, which witnessed a 55

percent increase in sales to US$ 11.1 billion.

Merck reported total revenues of US$ 41.75 billion and also

announced it will spin off its women’s health drugs,

biosimilar drugs and older products to create a new pharmaceutical

company with US$ 6.5 billion in annual revenues.

The firm had anticipated 2020 sales between US$ 48.8 billion and US$ 50.3 billion however this week it announced that the coronavirus pandemic will reduce 2020 sales by more than $2 billion.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

Humira holds on to remain world’s best-selling drug

AbbVie’s acquisition of Allergan comes as the firm faces the expiration of patent protection for Humira, which brought in a staggering US$ 19.2 billion in sales last year for

the company. AbbVie has failed to successfully acquire or develop a major new

product to replace the sales generated by its flagship drug.

In 2019, Humira’s US revenues increased 8.6 percent to US$ 14.86 billion while internationally, due

to biosimilar competition, the sales dropped 31.1 percent to US$ 4.30 billion.

Bristol Myers Squibb’s Eliquis, which is also marketed by Pfizer, maintained its number two position

and posted total sales of US$ 12.1 billion, a 23 percent increase over 2018.

While Bristol Myers Squibb’s immunotherapy treatment Opdivo, sold in partnership with Ono in Japan, saw sales increase from US$ 7.57 billion to US$ 8.0 billion, the growth paled in comparison to the US$ 3.9

billion revenue increase of Opdivo’s key immunotherapy competitor Merck’s Keytruda.

Keytruda took the number three spot in drug sales that

previously belonged to Celgene’s Revlimid, which witnessed a sales decline from US$ 9.69 billion to US$ 9.4 billion.

Cancer treatment Imbruvica, which is marketed

by J&J and AbbVie, witnessed a 30 percent increase in sales. With US$ 8.1

billion in 2019 revenues, it took the number five position.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

Vaccines – Covid-19 turns competitors into partners

This year has been dominated by the single biggest health emergency in years — the novel coronavirus (Covid-19) pandemic. As drugs continue to fail to meet expectations, vaccine development has received a lot of attention.

GSK reported the highest vaccine sales of all drugmakers with

total sales of US$ 8.4 billion (GBP 7.16 billion), a significant portion of its

total sales of US$ 41.8 billion (GBP 33.754 billion).

US-based Merck’s vaccine division also reported a significant increase in sales to US$ 8.0 billion and in 2019 received FDA and EU approval to market its Ebola vaccine Ervebo.

This is the first FDA-authorized vaccine against the deadly virus which causes

hemorrhagic fever and spreads from person to person through direct contact with

body fluids.

Pfizer and Sanofi also reported an increase in their vaccine sales to US$ 6.4

billion and US$ 6.2 billion respectively and the Covid-19 pandemic has recently

pushed drugmakers to move faster than ever before and has also converted

competitors into partners.

In a rare move, drug behemoths — Sanofi and GlaxoSmithKline (GSK) —joined hands to develop a vaccine for the novel coronavirus.

The two companies plan to start human trials

in the second half of this year, and if things go right, they will file

for potential approvals by the second half of 2021.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

Our view

Covid-19 has brought the world economy to a grinding halt and shifted the global attention to the pharmaceutical industry’s capability to deliver solutions to address this pandemic.

Our compilation shows that vaccines and drugs

for infectious diseases currently form a tiny fraction of the total sales of

pharmaceutical companies and few drugs against infectious diseases rank high on

the sales list.

This could well explain the limited range of

options currently available to fight Covid-19. With the pandemic currently infecting

over 3 million people spread across more than 200 countries, we can safely

conclude that the scenario in 2020 will change substantially. And so should our

compilation of top drugs for the year.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

Impressions: 55020

https://www.pharmacompass.com/radio-compass-blog/top-drugs-and-pharmaceutical-companies-of-2019-by-revenues

#PharmaFlow by PHARMACOMPASS

29 Apr 2020

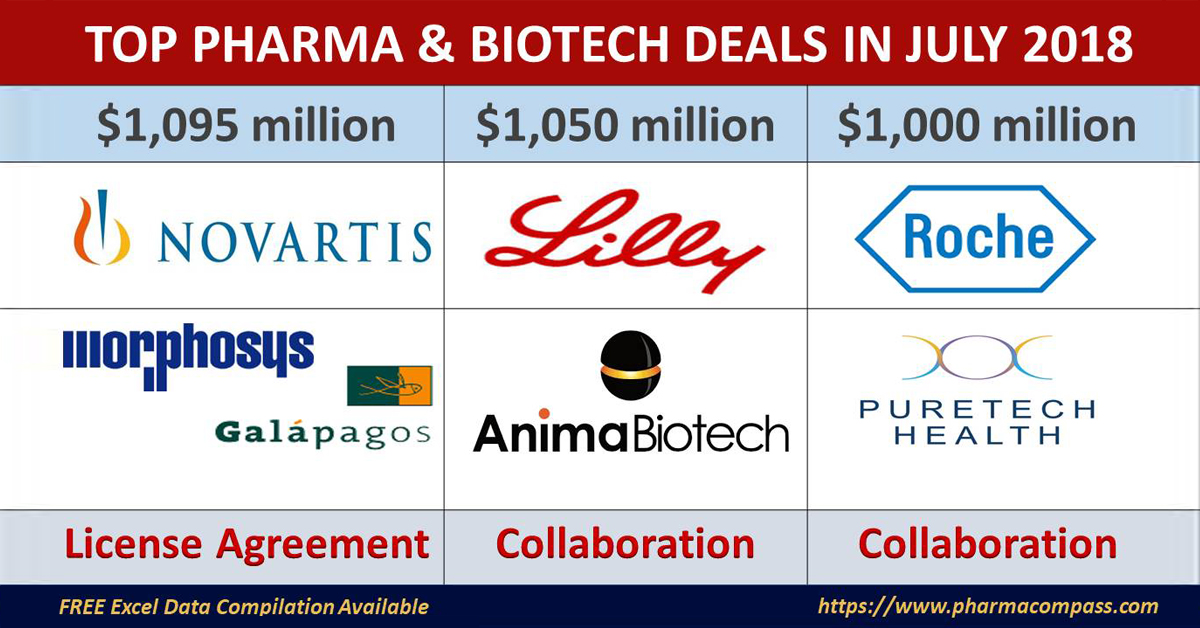

July may not have seen any big-ticket deals — i.e. deals in excess of US$ 1 billion — in the pharma and biotech space. Yet, deal making remained robust last month as well.

Companies like Novartis, Roche, Lilly

and Sanofi bolstered their R&D pipelines by striking deals which may result

in billion-dollar payouts if they achieve their milestones.

However, major investments were

announced in the manufacturing and contract services arena which indicate that

pharma job creation could be heading back to the United States.

Click here to view the major deals in July 2018 (FREE Excel version available)

Trump’s tax cuts make Pfizer announce major US manufacturing investment

Earlier this year, President

Donald Trump announced a reduction in the

US corporate tax rate from 35 percent to 21 percent. The tax cuts were designed to promote employment

and grow manufacturing in the United States.

In January, Pfizer announced its plan to invest approximately US$ 5 billion in US-based capital projects as a result of the enactment of the Tax Cuts and Jobs Act.

Click here to view the major deals in July 2018 (FREE Excel version available)

Last month, weeks after agreeing to roll back its drug price

increases, Pfizer announced it will

make a US$ 465 million investment to build one of the most technically advanced sterile injectable pharmaceutical production facilities in the world in Portage, Michigan.

Known as Modular Aseptic Processing (MAP), the new, multi-story,

400,000-square-foot production facility will also create an estimated 450 new

jobs over the next several years.

This investment will expand Pfizer’s presence in Portage, located in Kalamazoo County, where the company currently employs more than 2,200 people and is one of its largest plants.

During the next six years, Pfizer expects to invest approximately US$ 1.1 billion in Kalamazoo County.

Click here to view the major deals in July 2018 (FREE Excel version available)

Rubius’ IPO: Last month saw an uptick in IPO activity, and the biggest biotech IPO at Nasdaq so far in 2018 came from Cambridge,

Massachusetts-based Rubius Therapeutics, as it raised a whopping US$ 277.3 million to support its approach of engineering red

blood cells into off-the-shelf treatments for several

diseases across multiple therapeutic areas.

The firm also announced that it

had signed an agreement for the acquisition of a 135,000-square foot

manufacturing facility located in Smithfield, Rhode Island. The company plans to invest up to US$

95 million through 2020, and up

to US$ 155 million in total over a period five years or more, and it expects to hire approximately 150 people at the facility.

Click here to view the major deals in July 2018 (FREE Excel version available)

Cambrex acquires Halo Pharma: US-based Cambrex Corporation, a leading manufacturer of small molecule innovator and generic active

pharmaceutical ingredients (APIs), acquired Halo Pharma, a leading dosage form contract development and manufacturing organization (CDMO) for approximately US$ 425 million. Halo operates two facilities located in Whippany, New Jersey, USA and Montreal, Québec, Canada and is expected to generate over US$ 100 million in annual revenue in 2018.

With the acquisition of Halo, Cambrex will enter the growing finished dosage form CDMO market. Halo provides drug product development and commercial manufacturing services, specializing in oral solids, liquids, creams, sterile and non-sterile ointments. Halo’s core competencies include developing and manufacturing highly complex and difficult to produce formulations, products for pediatric indications and controlled substances.

Click here to view the major deals in July 2018 (FREE Excel version available)

Catalent acquires Juniper: Also expanding its presence in the CDMO space

was Catalent,

which acquired Juniper Pharmaceuticals. While Catalent is a leading global provider of

advanced delivery technologies and development solutions for drugs, biologics

and consumer health products, Juniper is a company with two core businesses,

the first being its Crinone (progesterone gel) franchise and the other a fee-for-service

CDMO known as Juniper Pharma Services (JPS).

The transaction was valued at approximately US$ 139.6 million.

Click here to view the major deals in July 2018 (FREE Excel version available)

Novartis continues to bet big on dermatology

A month after Swiss drugmaker Novartis Pharmaceuticals Corporation announced it plans to spin

off Alcon eye care business into a separately traded

standalone company and buy back up to US$ 5 billion in stock, Novartis signed a licensing agreement with MorphoSys and

Galapagos covering the development and commercialization of their investigational, fully human, IgG1 monoclonal antibody – MOR106.

MOR106 is directed against the target IL-17C that was generated in a collaboration between MorphoSys and Galapagos. IL-17C is believed to contribute significantly to atopic dermatitis (AD), a form of eczema and a severe dermatologic condition with high prevalence.

Click here to view the major deals in July 2018 (FREE Excel version available)

MOR106 will be an extension of Novartis’ AD pipeline portfolio that includes oral ZPL389 that is currently in phase II clinical trials.

Atopic Dermatitis, a form of

eczema, is a dermatologic disease that can cause intense itching and recurring

lesions. AD affects approximately 8 percent of adults and 14 percent of

children worldwide.

Novartis also has a blockbuster

drug, Cosentyx (secukinumab), a human IgG1κ monoclonal antibody that binds to the protein interleukin-17A, and is marketed for the treatment of psoriasis, ankylosing spondylitis, and psoriatic arthritis. Cosentyx generated sales of over US$ 2 billion in 2017.

Click here to view the major deals in July 2018 (FREE Excel version available)

In addition to the funding of the current and future MOR106 program by Novartis, MorphoSys and Galapagos will jointly receive an upfront payment of Euro 95 million.

Pending achievement of certain developmental, regulatory, commercial and sales-based milestones, MorphoSys and Galapagos would jointly be eligible to receive significant milestone payments, potentially amounting to approximately Euro 850 million, in addition to tiered royalties on net commercial sales.

Under the terms of their agreement from 2008, Galapagos and MorphoSys will share all payments equally.

Click here to view the major deals in July 2018 (FREE Excel version available)

Roche strikes a deal to develop

drugs using milk-derived exosomes

Milk naturally contains small lipid vesicles called exosomes that

deliver biochemical packages from the mother to her offspring.

A research group led by Dr. Ramesh Gupta from the University of

Louisville recently highlighted a new approach for improving therapeutic drug

effectiveness by artificially packaging drugs in bovine milk-derived exosomes.

It is believed that milk exosomes represent a significant opportunity to potentially resolve the long-standing challenge of oral bioavailability of macromolecules and complex small molecules.

Milk-derived exosomes form the basis for PureTech’s internally-developed technology to accomplish the task of oral transport of complex biological molecules. The technology is based on research conducted by PureTech Health and its academic collaborators, which including Dr. Ramesh Gupta.

Click here to view the major deals in July 2018 (FREE Excel version available)

PureTech Health announced that it has entered into a multiyear collaboration with Swiss drugmaker Roche, to advance PureTech’s milk-derived exosome platform technology for the oral administration of Roche’s antisense oligonucleotide platform.

Under the terms of the agreement, PureTech Health will receive up to $36 million, including upfront payments, research support, and early preclinical milestones. PureTech Health will be eligible to potentially receive development milestone payments of over $1 billion and additional sales milestones and royalties for an undisclosed number of products.

Click here to view the major deals in July 2018 (FREE Excel version available)

Lilly ties up with Anima Biotech for novel strategy against undruggable targets

Anima Biotech’s Translation Control Therapeutics platform got a huge vote of confidence as it struck a deal with Eli Lilly that has the potential to exceed US$ 1

billion.

Anima Biotech is pioneering a

new class of drugs that specifically control protein translation as a novel

strategy against hard and undruggable targets.

The term ‘undruggable' was coined to describe proteins that could not be targeted pharmacologically. However, companies such as Anima have made considerable progress to ‘drug’ many hard and undruggable targets.

The company claims that its novel platform enables for the first time to visualize and specifically control the synthesis of target proteins. By targeting the mechanisms that specifically regulate the process of mRNA translation, they can discover small molecules that either decrease or increase a target protein’s production, enabling a new strategy and new hope against hard and undruggable targets.

Anima’s platform was validated by its fast-growing pipeline programs in multiple therapeutic areas including fibrosis, viral infections,

oncology and neuroscience.

The collaboration with Lilly is to discover and develop translation inhibitors for several target proteins using Anima’s Translation Control Therapeutics platform. It is a multi-year deal set around undisclosed Lilly targets. Anima will use its platform to discover lead candidates that affect the translation of the Lilly targets. Lilly will then handle clinical development and commercialization.

Click here to view the major deals in July 2018 (FREE Excel version available)

Under the terms of the deal, Lilly is paying Anima US$ 30 million

upfront and US$ 14 million in research funding. Anima is eligible for up

to US$ 1.05 billion in development and commercial milestones. Anima is

also entitled to tiered royalties on any products that result from the

collaboration in the low to mid-single digits.

PTC broadens drug pipeline with gene therapy buy

Founded almost 20 years ago, PTC Therapeutics is focused on the discovery, development and commercialization of

medicines for patients with rare disorders. With two drugs on the market

including the contentious Emflaza (deflazacort), PTC announced last month

that it had entered into an agreement to acquire Agilis

Biotherapeutics, Inc., a biotechnology company advancing an innovative gene therapy platform for rare monogenic diseases that affect the central nervous system.

Click here to view the major deals in July 2018 (FREE Excel version available)

The lead gene therapy candidate,

GT-AADC, has compelling clinical data in treating a rare central nervous system

disorder which is an outcome of Aromatic L-Amino Acid Decarboxylase (AADC)

Deficiency.

Under the terms of the merger

agreement, PTC will pay an upfront consideration of US$ 50 million in cash and approximately US$ 150

million in PTC common stock. In addition to

the upfront payments, potential future consideration includes US$

60 million in development milestones to be

paid over the next two years (including the acceptance of a biologics license

application or BLA).

Additionally, the transaction

includes up to US$ 535 million in

success-based milestones in connection with regulatory approvals on the three

most advanced programs and receipt of a priority review voucher, as well as

tiered commercial milestones.

The priority review vouchers, which the FDA awards to companies

that develop drugs for neglected diseases and rare pediatric disorders, ensure

a speedier review from the FDA once a company files for approval. These

vouchers have become valuable commodities themselves, having been bought and

sold at prices topping US$ 100 million.

Click here to view the major deals in July 2018 (FREE Excel version available)

Sanofi buys into early-stage therapy for non-small cell lung

cancer

Sanofi paid an upfront fee of US$ 50 million to develop and commercialize Revolution Medicines’ targeted cancer therapies for patients with non-small cell lung cancer (NSCLC) and other types of cancers carrying certain mutations.

In a deal where Revolution Medicines could receive more than US$ 500 million in development and regulatory milestone payments, Sanofi will apply its expertise in oncology research and drug development to bring Revolution’s lead candidate RMC-4630 to the market.

Click here to view the major deals in July 2018 (FREE Excel version available)

For a molecule which will only enter into human clinicals in the second half of this year, Sanofi’s bet is on RMC-4630 fighting cancer in two separate ways.

First, the drug inhibits SHP2, a cellular enzyme in the protein tyrosine phosphatase family that plays a key role in several types of cancer. And second, the molecule has the “potential to stall — or even shrink — the tumor itself, and also neutralize the immune-suppressing environment in which the tumor thrives,” Revolution’s president and CEO Mark Goldsmith said in an interview with Endpoints News.

Click here to view the major deals in July 2018 (FREE Excel version available)

Our view

Although major investments were announced by companies based in

the US and Europe, there has been a significant uptick in deal making by

Chinese companies as well.

Chinese biotech companies Innovent

Biologics and Ascletis Pharma applied to

list on the Hong Kong Exchange. In its IPO, Ascletis, which makes anti-viral, cancer and liver disease drugs, was

valued at US$ 2 billion. The IPOs are seen as a test for Hong Kong,

which is seeking to establish itself as a financing center for the

growing number of Chinese drug developers.

While it remains to be seen if Hong Kong can dislodge New York as the established center of biotech IPOs, with nine biotechs having so far filed for Hong Kong listings, and at least another four planning to follow suit, we hope you would keep following PharmaCompass’ compilation of top pharma and biotech deals — PharmaFlow — to keep track of key happenings in this area.

Click here to view the major deals in July 2018 (FREE Excel version available)

Impressions: 3999

https://www.pharmacompass.com/radio-compass-blog/top-pharma-biotech-deals-investments-m-as-july-2018

#PharmaFlow by PHARMACOMPASS

16 Aug 2018