In 2016, M&A deals

fell drastically in both numbers and value. One key reason was the falling

through of the Pfizer-Allergan mega merger due to America’s crack down on inversion deals.

The year 2015 went down in

history as a record year for mergers and acquisitions (M&As) in the

pharmaceutical and biotech space, when deals worth US $ 300 billion were

announced.

The

highlight of 2015 was the mega-merger announced between US drugmaker Pfizer and

Ireland-based Allergan – the biggest-ever pharma transaction that

was worth more than US$ 160 billion.

2016 saw Pfizer and Allergan walk away from their US$ 160 billion merger when the new US

Treasury rules cracked down on inversion deals that were encouraging US

companies to move overseas to cut taxes.

The merger would have allowed

New York-based Pfizer to cut its tax bill by an estimated US$ 1 billion

annually by domiciling in Ireland, where tax rates are lower.

M&A deals dip by 20

percent in 2016

Although the Pfizer-Allergan

mega-merger did not go through, The Pharma Letter tracked transactions through the year and noted that although “worldwide merger and acquisition activity in the pharmaceutical and biotechnology sector in 2016 was plentiful”, the numbers and values were “well down” on those seen in the previous two years.

The number of transactions announced in 2016 was 130, compared to 166 M&A deals in 2015 – which was a record year – and 137 in 2014, says The Pharma Letter.

Values of the top 10 deals

drop to a third

The other crucial fact about

M&A deals in 2016 was that transactions that exceeded the US$ 1 billion

mark were down to just 23 in 2016, as against 30 in 2015 and 26 in 2014.

The Pharma Letter quotes a

KPMG report published earlier this year which notes that the total value of the

top 10 completed deals in the first half of 2016 amounted to US $ 67.2 billion

as opposed to US $190.4 billion in first-half 2015.

Sanofi-Actelion — the deal that wasn’t

Sanofi made headlines, not for the acquisitions it made, but for the ones it wasn’t able to close.

Late last year, the French

pharma giant was widely identified as the big player that managed to push Johnson & Johnson away from negotiations with Actelion only to lose its US$ 30 billion bid to J&J even though it would have delivered “approximately equivalent value to Actelion’s shareholders”.

The Actelion loss came after Sanofi was out bid by Pfizer for Medivation.

Pfizer agreed to buy the US

cancer drug company for US$ 14 billion in cash, adding its blockbuster prostate

cancer drug Xtandi to

the company's growing oncology roster.

Additionally, Pfizer acquired Anacor for US$ 5.2 billion to add an eczema gel to its portfolio.

Bayer’s US$ 66 billion takeover

The biggest deal announced in

2016 was Bayer’s US$ 66 billion takeover of the US seeds company Monsanto after months of wrangling. It was the German drug and crop-chemical company’s third offer that clinched the deal, which is also known to be the largest all-cash deal on record.

This signature

deal has disrupted the agribusiness sector, which in recent years has been

involved in a consolidation race largely triggered by factors such as shifting

weather patterns, intense competition in grain exports and a souring global

farm economy.

Top pharma companies by sales

Bayer’s acquisition of Monsanto makes the ranking of top pharmaceutical companies consistently complicated since Bayer will generate more sales from its crop

science and high-tech polymer division than from the sale of prescription

drugs.

Should divisions like

diagnostics, animal health, vaccines, consumer health be counted while

determining the size of a pharmaceutical company?

In a volatile global world,

where wild exchange rate fluctuations play their own major role in determining

the size of organizations, this week PharmaCompass

shares the revenues, as presented in the 2016 annual reports of top 15

companies, so that you can draw your own conclusions on the top drug companies

of the world.

Company Name

Currency

Pharma

Consumer Health

Medical Devices/ Diagnostics

Vaccines

Animal Health

Other Revenues

Total Sales

1

Pfizer

USD

41,600

3,407

6,071

1,746

52,824

2

Novartis

USD

48,518

48,518

3

Roche

CHF

41,047

11,589

52,636

4

Merck & Co.

USD

29,360

5,791

3,478

1,178

39,807

5

GlaxoSmithKline

GBP

16,104

7,193

4,592

27,889

6

Johnson & Johnson

USD

33,464

13,307

25,119

71,890

7

Sanofi

EUR

22,932

3,330

4,577

2,708

274

33,821

8

Gilead

USD

29,953

437

30,390

9

Abbvie

USD

25,560

78

25,638

10

Bayer

EUR

16,420

6,037

1,523

22,789

46,769

11

Amgen

USD

21,892

1,099

22,991

12

Astrazeneca

USD

21,319

1,683

23,002

13

Teva

USD

20,664

1,239

21,903

14

Eli Lilly

USD

18,064

3,158

21,222

15

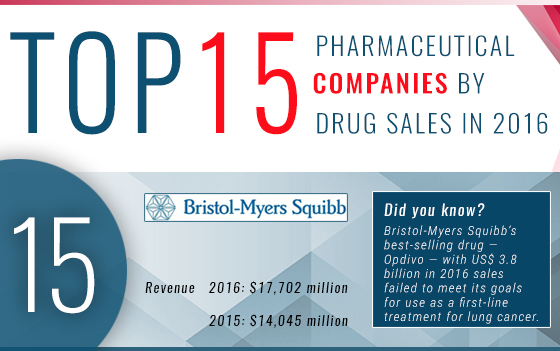

Bristol-Myers Squibb

USD

17,702

1,725

19,427

Sales figures are reported in millions.

Currency exchange rate used CHF: 0.99 USD/ EUR: 1.06 USD / GBP: 1.25 USD

Ranking methodology

When it came to ranking

companies, based on their total sales, we at PharmaCompass did

not face any challenges while including the sales of prescription drugs along

with those of vaccines.

But matters got a little

complicated when we got down to ranking consumer health divisions.

For instance, while we have

included consumer health divisions of companies like Sanofi, GSK and

Bayer, which primarily sell OTC drug products (such as brands like Allegra, Voltaren and Aleve), we have excluded those of companies like Johnson

& Johnson, given their focus on baby and beauty products.

Such a demarcation — based on the focus of the company — will always be a matter of debate.

Similarly, revenue generated

from the sale of medical devices/diagnostics as well as revenues of animal health divisions were not included in our rankings.

In the case of companies like Bayer, whose Covestro’s division has over US$ 10 billion in sales from customer industries such as automotive, construction, electrical and electronics, and furniture, such sales were accounted for in ‘other revenues’.

Our table highlights the sales

revenue of various divisions of companies in order to bring more clarity into the

figures which were included in our rankings.

Impressions: 13636