Market Place

Market Place Sourcing Support

Sourcing Support

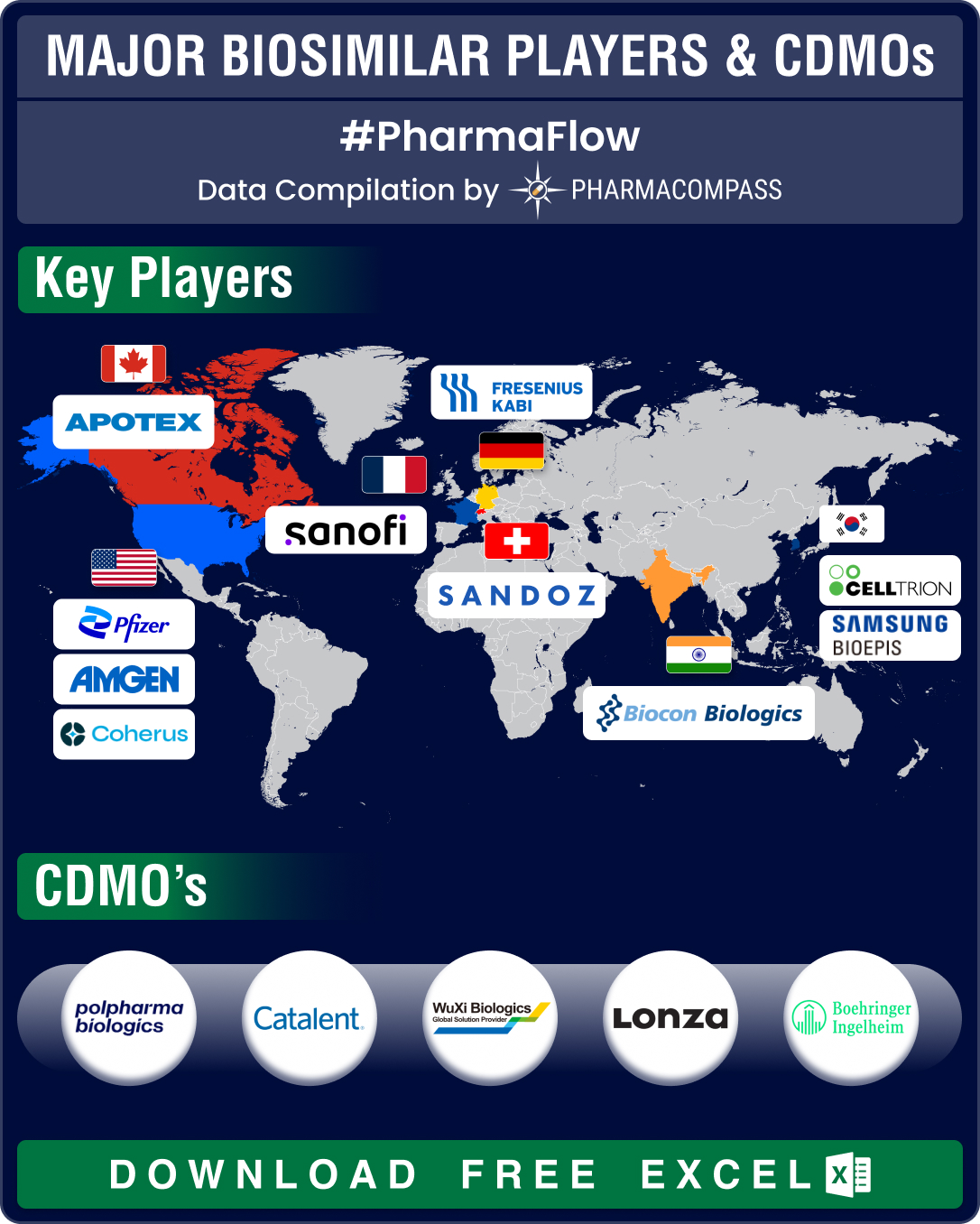

FDA approves record eight biosimilars in H1 2024; okays first interchangeable biosimilars for Eylea

Biologics, or complex drugs that are derived from living organisms, have revolutionized treatment of

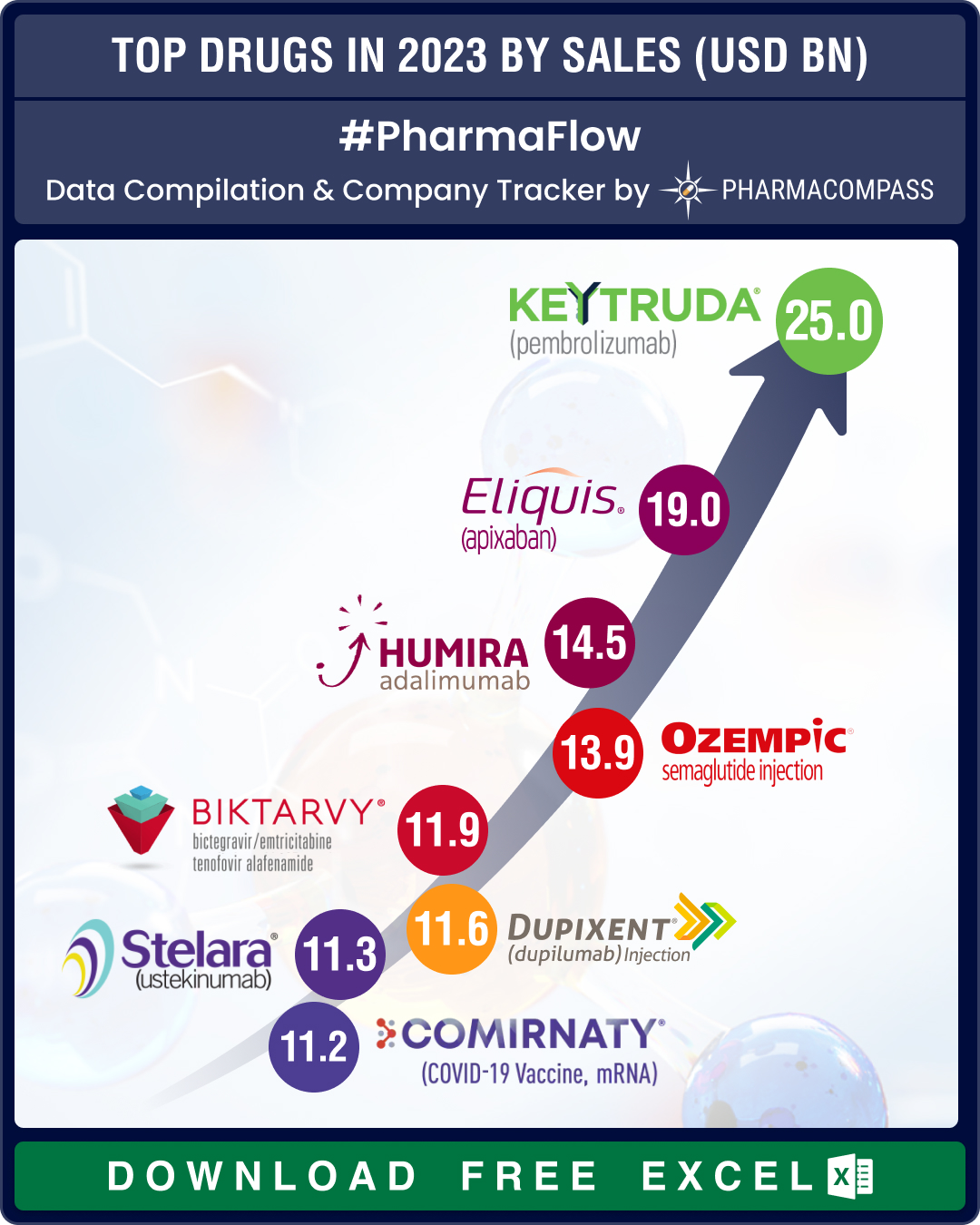

Top Pharma Companies & Drugs in 2023: Merck’s Keytruda emerges as top-selling drug; Novo, Lilly sales skyrocket

The pharma industry clearly recalibrated itself in 2023, turning its focus away from Covid and onto

FDA reports 62.5% growth in new drug approvals in H1 2023; Health Canada sees drop

After a year when

drug approvals by the US Food and Drug Administration

(FDA) slipped to the lowes