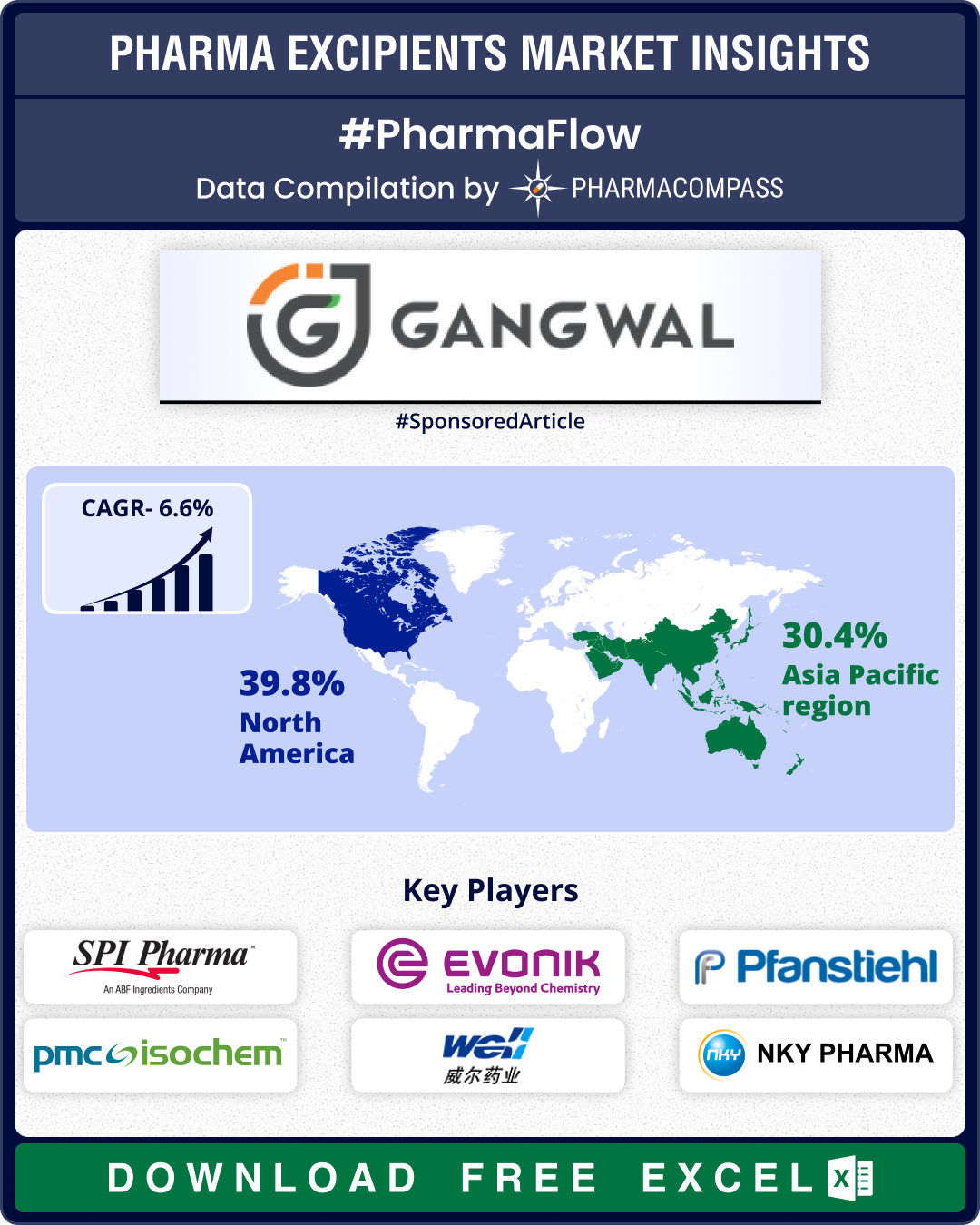

Excipient Market Overview: Evonik launches high-purity excipients; India mandates disclosures from March 2026

The global pharmaceutical excipients market continued to evolve in the third quarter (Q3) of 2025, s

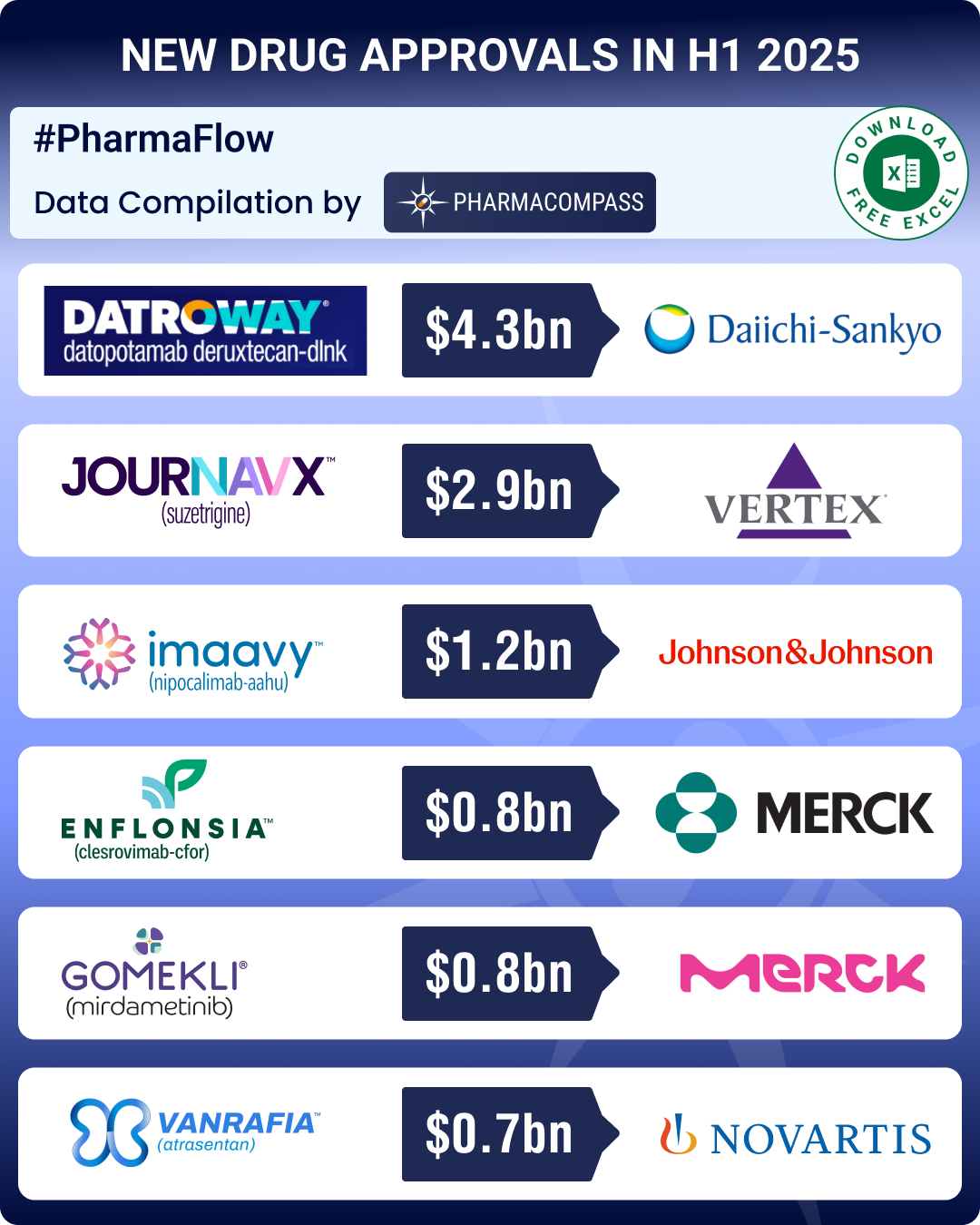

FDA approvals drop 24% in H1 2025; GSK’s UTI med, Vertex’s non-opioid painkiller lead pack of first-in-class meds

It has been a turbulent year for the US

Food and Drug Administration (FDA), marked by reduction

CDMO Activity Tracker: Veranova, Carbogen lead ADC investments; Axplora, Polfa Tarchomin, Famar expand European footprint

During the second quarter (Q2) of 2025, contract development and manufacturing organizations (CDMOs)

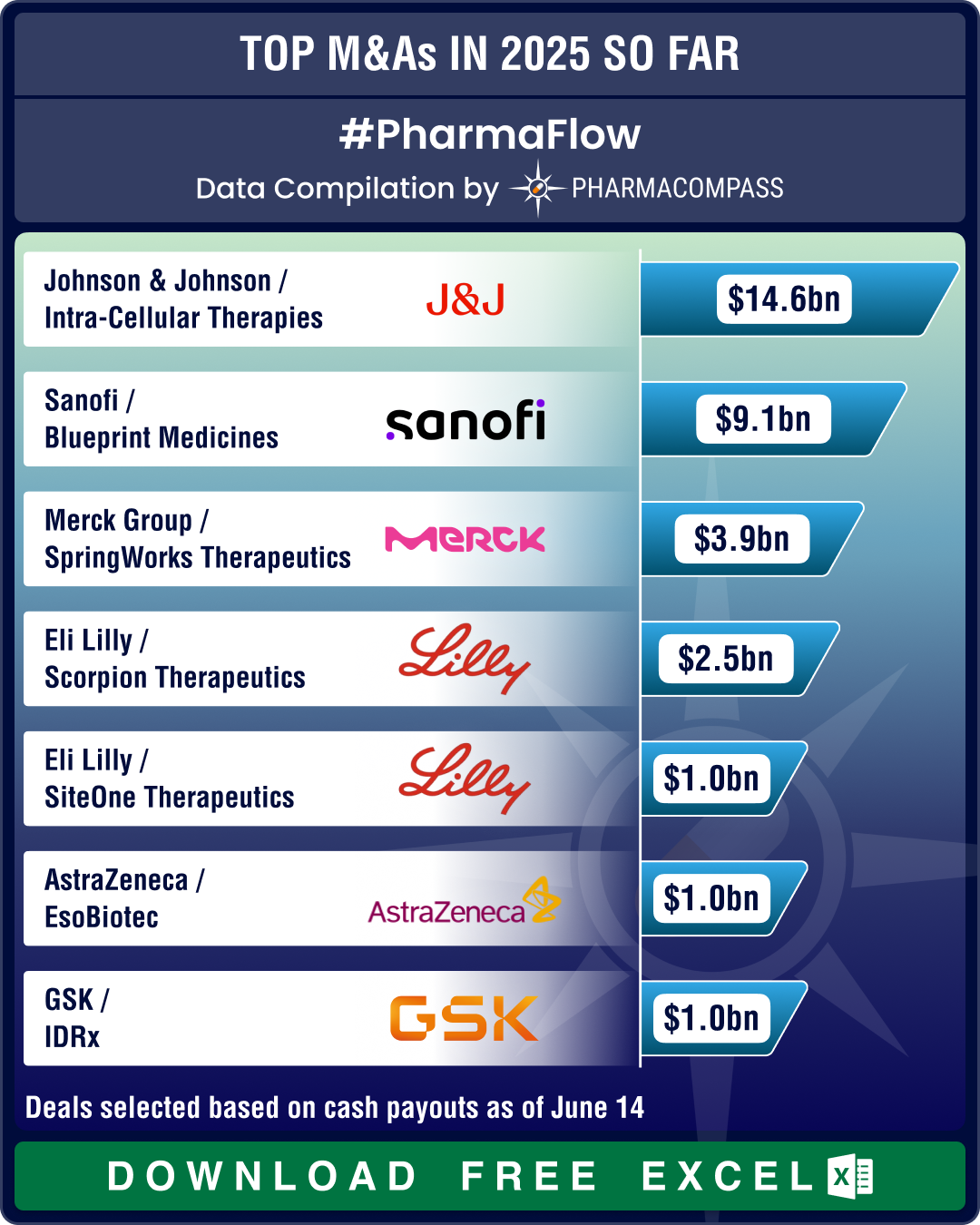

J&J’s Intra‑Cellular buyout, BMS’ oncology gambit, Sanofi’s Blueprint acquisition drive mega deals in H1 2025

The pharmaceutical industry has witnessed a wave of mergers, acquisitions, and strategic partnership

Excipient Market Overview: Roquette announces restructuring post IFF Pharma buyout; WHO, FDA advance regulatory frameworks

The pharmaceutical excipients market saw significant strategic

consolidations, technological develo

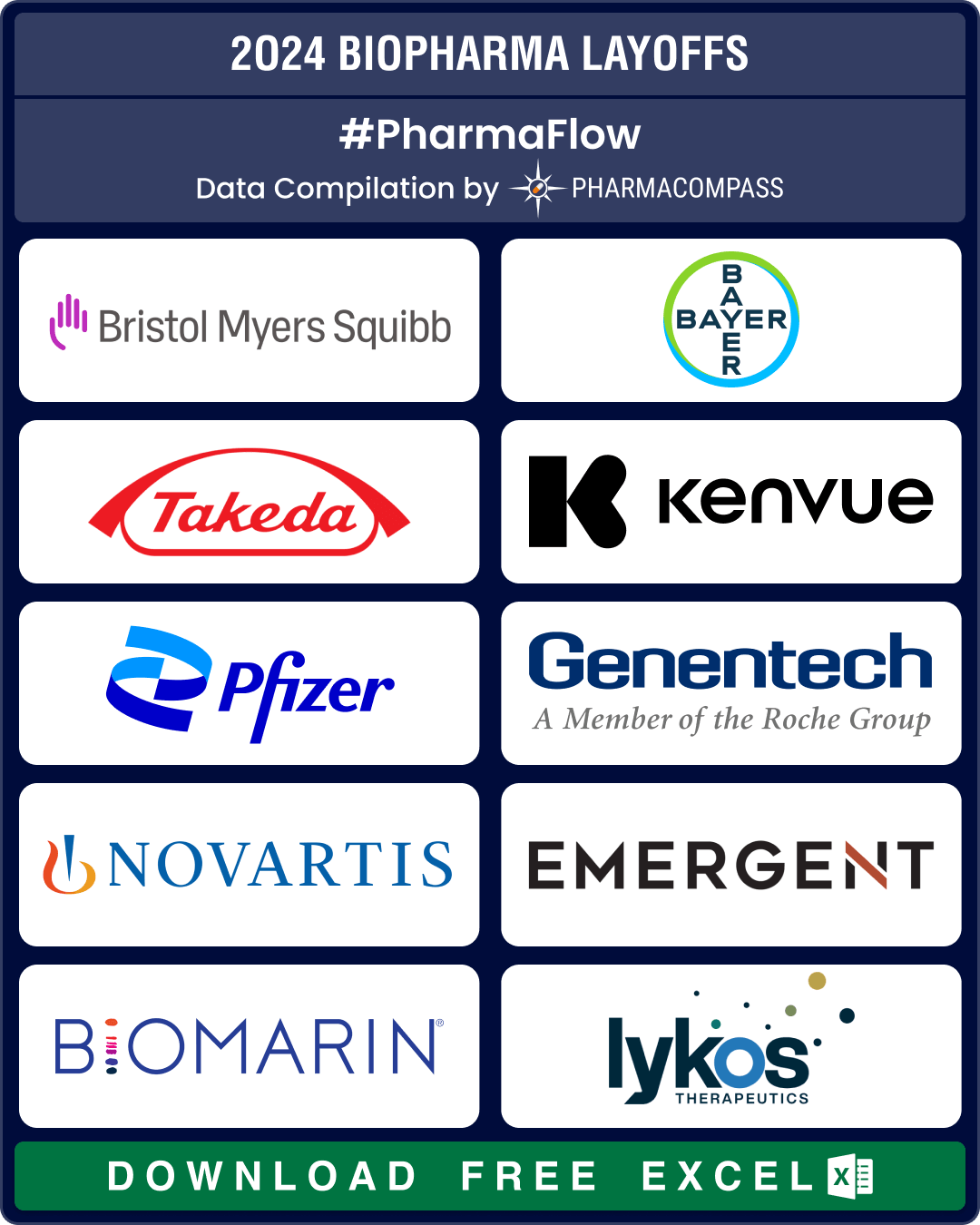

BMS, J&J, Bayer lead 25,000+ pharma layoffs in 2024; Amylyx, FibroGen, Kronos Bio hit by trial failures, cash crunch

Since 2022, there has been a significant surge in layoffs by pharmaceutical and biotech companies. W

CDMO Activity Tracker: Bora, PolPharma make acquisitions; Evonik, EUROAPI, Porton announce technological expansions

The contract development and

manufacturing organization (CDMO) space continued to grow at an impres

BMS, Bayer, Takeda, Pfizer downsize to combat cost pressures, meet restructuring plans

Over

the last two years, there has been a significant surge in layoffs by

pharmaceutical and biote

Excipient Market Overview: Roquette, Seqens, Evonik make strategic moves; new guidelines deal with contamination

The pharmaceutical industry has long recognized the critical role

excipients or inactive ingredient

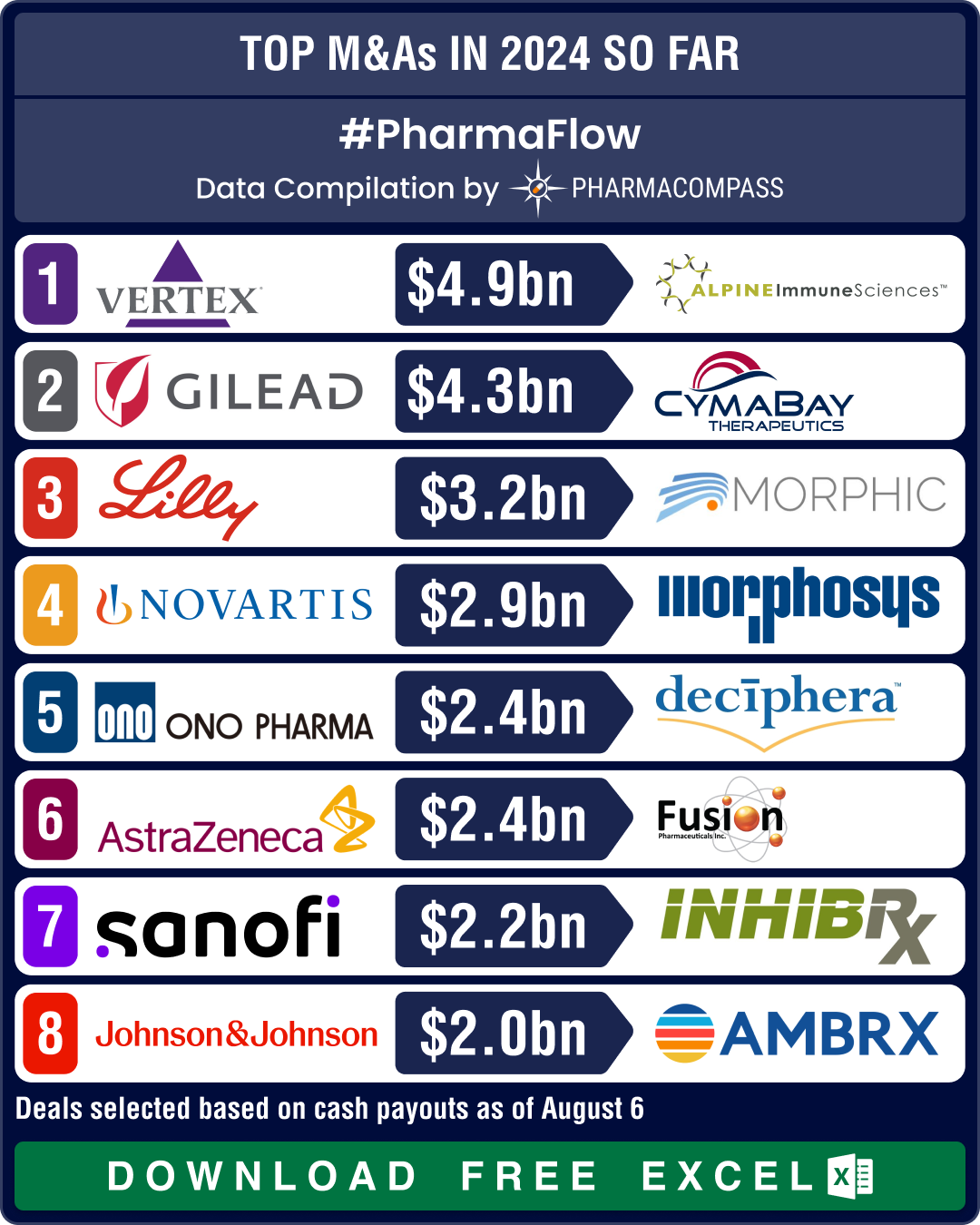

Novartis, GSK, Sanofi, BMS shell out over US$ 10 bn in dealmaking, as mid-size deals take centerstage in 2024

The world of pharmaceuticals and biotechnology continued to evolve

this year with strategic allianc

- Privacy policy

- Terms and conditions

- Disclaimers

-

- Product listings are provided for informational purposes only. We do not supply or sell any products. Any products that may be covered by patent(s) are supplied solely for uses permitted under Section 107A of the Indian Patents Act and not for commercial sale.