This week PharmaCompass brings to you key highlights of the US Food and Drug Administration’s recently released June 2024 list of Off-Patent, Off-Exclusivity

Drugs without an Approved Generic (OPOE list). The list is a crucial

resource for promoting competition and affordability in the pharmaceutical

industry. Updated biannually in December and June, the OPOE list serves as a

transparent guide for drug manufacturers.

Since December 2021, the FDA has enhanced its transparency efforts by providing separate lists for prescription (Rx) and over-the-counter (OTC) drugs approved under a New Drug Application (NDA). This initiative is a significant cog in the FDA’s broader strategy to encourage the development and submission of Abbreviated New Drug Applications (ANDAs).

ANDAs are a streamlined pathway for generic drug development,

offering a more cost-effective alternative to brand-name drugs. By highlighting

drugs that lack generic competition on the OPOE list, FDA aims to incentivize

manufacturers to develop generics, ultimately leading to greater affordability

and access for patients.

Access the Interactive Dashboard on FDA's June 2024 List of Off-Patent Drugs (Free Excel)

ALS drugs, cancer, asthma,

HIV treatments among new drugs added to OPOE list

The December 2023 OPOE list had 23 new applications of branded

drugs eligible for but without generic competition. The June list further added

21 new applications of drugs that had never appeared before. These include bendamustine hydrochloride (to treat chronic

lymphocytic leukemia), fluticasone propionate (to treat asthma), maraviroc (to treat HIV-1 infection in

patients two years of age and older weighing at least 10 kilograms), carbamazepine (to treat epilepsy and

bipolar I disorder), and posaconazole (an antifungal agent indicated for Aspergillus and Candida infections). There are two other drugs on the list – edaravone and riluzole – to treat amyotrophic lateral sclerosis (ALS) or Lou Gehrig’s disease (a neurological disorder).

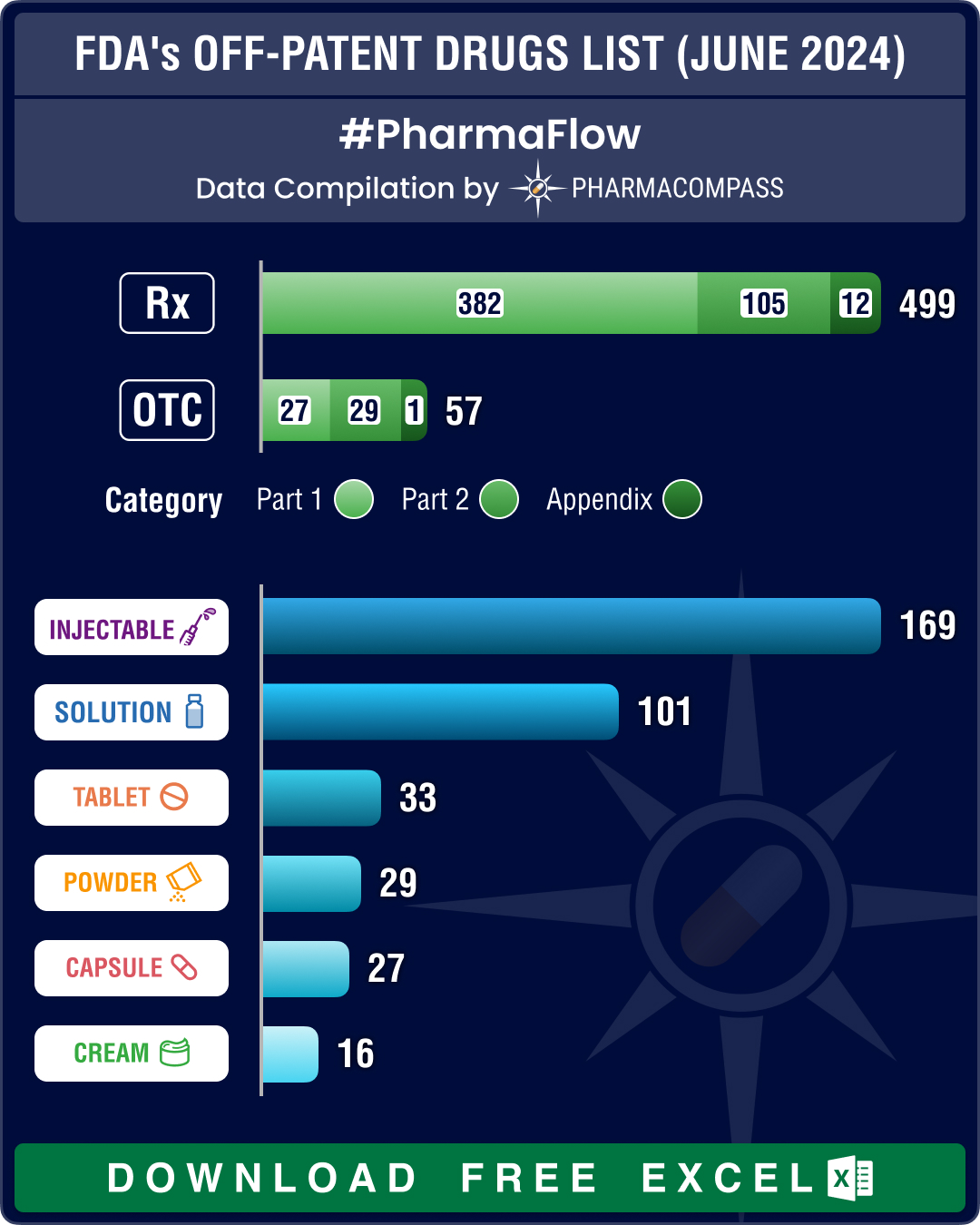

Much like the June 2023 OPOE list, nearly one-third of the prescription drugs listed are injectables – 170 out of 499. There are 74 prescription entries for oral solid dosage forms (such as tablets, capsules and modified release forms).

The June 2024 OPOE list has 57 OTC drugs, a tad shy of the 60 drugs in last year’s list. Among them are antihistamine drugs (used to treat allergies), cetirizine hydrochloride, nizatidine, famotidine, loratadine and anti-obesity medication orlistat.

The list also had a newly listed drug, which is a combination of chlorpheniramine maleate, ibuprofen and pseudoephedrine hydrochloride for treating allergic sinusitis. Out of the 57 OTC drug products on the list, 18 are delivered as oral solid dosage forms.

Access the Interactive Dashboard on FDA's June 2024 List of Off-Patent Drugs (Free Excel)

Novartis blockbusters lose exclusivity, Lupin wins FDA nod for copycat of Neurocrine’s bestseller

This year, several large-selling drugs from drugmakers like Eisai, AbbVie, Gilead, Sanofi, Fresenius Kabi and

others are due to face their first generic or biosimilar challengers in the US market. “First generics” are given for a first-to-file ANDA, for which there is no previously-approved ANDA by the FDA for the drug product.

The agency considers first generics to be important to public

health and prioritizes review of these submissions. First generics are eligible

for a 180-day exclusivity period.

Three of Novartis’ drugs have lost exclusivity so far, this year. These include Promacta/Revolade (eltrombopag) used to treat

thrombocytopenia (low platelet count). Promacta was approved in 2015 and saw sales of US$ 2.27 billion last year. Annora Pharma scored an FDA approval for eltrombopag’s first generic in April. Tasigna (nilotinib), the Swiss drugmaker’s oral treatment for Philadelphia chromosome-positive chronic myeloid leukemia (a kind of leukemia where patients have an abnormal

chromosome in their blood cells called the Philadelphia chromosome), got its

first generic in January, which was introduced by Apotex. Tasigna brought

in sales of US$ 1.85 billion in 2023 and its sales are

projected to plummet to US$ 79 million by 2029. Novartis’ Rydapt (midostaurin) for treating adult patients

with newly diagnosed acute myeloid leukemia (AML) also lost exclusivity in

April.

Neurocrine Biosciences’ top-selling drug Ingrezza (valbenazine) was the first FDA-approved

drug to treat tardive dyskinesia, a disorder that involves involuntary

movements. It raked in US$ 1.84 billion in 2023, registering a

year-on-year growth of 29 percent. In April, Lupin won FDA’s approval for the first generic of valbenazine capsules.

Access the Interactive Dashboard on FDA's June 2024 List of Off-Patent Drugs (Free Excel)

Our view

The Biden administration has been pushing hard to lower the price of prescription drugs. It is one of President Joe Biden’s central campaign promises this year. However, lowering drug prices is a bipartisan issue in the US. So whether a republican or

a democrat takes over the US administration, making medicines affordable should

remain a priority.

In 2023, generic drugs accounted for US$ 424 billion of the US$ 1.6 trillion global pharmaceutical market. A determined FDA that is proactively looking to approve generic drugs will no doubt help this segment grow even further.

Impressions: 2500

https://www.pharmacompass.com/radio-compass-blog/fda-s-june-2024-list-of-off-patent-off-exclusivity-drugs-sees-rise-in-cancer-hiv-treatments

#PharmaFlow by PHARMACOMPASS

11 Jul 2024

Acquisitions and spin-offs dominated headlines in 2019 and the tone was set very early with Bristol-Myers Squibb acquiring

New Jersey-based cancer drug company Celgene in a US$ 74 billion deal announced on

January 3, 2019. After factoring

in debt, the deal value ballooned to about US$ 95 billion, which according

to data compiled by Refinitiv, made it the largest healthcare deal on

record.

In the summer, AbbVie Inc,

which sells the world’s best-selling drug Humira, announced its acquisition of Allergan Plc, known for Botox and other cosmetic

treatments, for US$ 63 billion. While the companies are still awaiting

regulatory approval for their deal, with US$ 49 billion in combined 2019

revenues, the merged entity would rank amongst the biggest in the industry.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

The big five by pharmaceutical sales — Pfizer,

Roche, J&J, Novartis and Merck

Pfizer

continued

to lead companies by pharmaceutical sales by reporting annual 2019 revenues of

US$ 51.8 billion, a decrease of US$ 1.9 billion, or 4 percent, compared to

2018. The decline was primarily attributed to the loss of exclusivity of Lyrica in 2019,

which witnessed its sales drop from US$ 5 billion in 2018 to US$ 3.3 billion in

2019.

In 2018, Pfizer’s then incoming CEO Albert Bourla had mentioned that the company did not see the need for any large-scale M&A activity as Pfizer had “the best pipeline” in its history, which needed the company to focus on deploying its capital to keep its pipeline flowing and execute on its drug launches.

Bourla stayed true to his word and barring the acquisition of Array Biopharma for US$ 11.4 billion and a spin-off to merge Upjohn, Pfizer’s off-patent branded and generic established medicines business with

Mylan, there weren’t any other big ticket deals which were announced.

The

Upjohn-Mylan merged entity will be called Viatris and is expected to have 2020

revenues between US$ 19 and US$ 20 billion

and could outpace Teva to

become the largest generic company in the world, in term of revenues.

Novartis, which had

followed Pfizer with the second largest revenues in the pharmaceutical industry

in 2018, reported its first full year earnings after spinning off its Alcon eye

care devices business division that

had US$ 7.15 billion in 2018 sales.

In 2019,

Novartis slipped two spots in the ranking after reporting total sales of US$

47.4 billion and its CEO Vas Narasimhan continued his deal-making spree by buying New

Jersey-headquartered The Medicines Company (MedCo) for US$ 9.7

billion to acquire a late-stage cholesterol-lowering

therapy named inclisiran.

As Takeda Pharmaceutical Co was

busy in 2019 on working to reduce its debt burden incurred due to its US$ 62

billion purchase of Shire Plc, which was announced in 2018, Novartis also purchased

the eye-disease medicine, Xiidra, from the Japanese drugmaker for US$ 5.3 billion.

Novartis’ management also spent a considerable part of 2019 dealing with data-integrity concerns which emerged from its 2018 buyout of AveXis, the

gene-therapy maker Novartis had acquired for US$ 8.7 billion.

The deal gave Novartis rights to Zolgensma,

a novel treatment intended for children less than two years of age with the

most severe form of spinal muscular atrophy (SMA). Priced at US$ 2.1 million,

Zolgensma is currently the world’s most expensive drug.

However,

in a shocking announcement, a month after approving the drug, the US Food and

Drug Administration (FDA) issued a press release on

data accuracy issues as the agency was informed by AveXis that

its personnel had manipulated data which

the FDA used to evaluate product comparability and nonclinical (animal)

pharmacology as part of the biologics license application (BLA), which was

submitted and reviewed by the FDA.

With US$

50.0 billion (CHF 48.5 billion) in annual pharmaceutical sales, Swiss drugmaker

Roche came in at number two position in 2019

as its sales grew 11 percent driven by

its multiple sclerosis medicine Ocrevus, haemophilia drug Hemlibra and cancer medicines Tecentriq and Perjeta.

Roche’s newly introduced medicines generated US$ 5.53 billion (CHF 5.4 billion) in growth, helping offset the impact of the competition from biosimilars for its three best-selling drugs MabThera/Rituxan, Herceptin and Avastin.

In late 2019, after months of increased

antitrust scrutiny, Roche completed

its US$ 5.1 billion acquisition of Spark Therapeutics to strengthen its presence in

gene therapy.

Last year, J&J reported almost flat worldwide sales of US$ 82.1 billion. J&J’s pharmaceutical division generated US$ 42.20 billion and its medical devices and consumer health divisions brought in US$ 25.96 billion and US$ 13.89 billion respectively.

Since J&J’s consumer health division sells analgesics, digestive health along with beauty and oral care products, the US$ 5.43 billion in consumer health sales from over-the-counter drugs and women’s health products was only used in our assessment of J&J’s total pharmaceutical revenues. With combined pharmaceutical sales of US$ 47.63 billion, J&J made it to number three on our list.

While the sales of products like Stelara, Darzalex, Imbruvica, Invega Sustenna drove J&J’s pharmaceutical business to grow by 4 percent over 2018, the firm had to contend with generic competition against key revenue contributors Remicade and Zytiga.

US-headquartered Merck, which is known as

MSD (short for Merck Sharp & Dohme) outside the United States and

Canada, is set to significantly move up the rankings next year fueled by its

cancer drug Keytruda, which witnessed a 55

percent increase in sales to US$ 11.1 billion.

Merck reported total revenues of US$ 41.75 billion and also

announced it will spin off its women’s health drugs,

biosimilar drugs and older products to create a new pharmaceutical

company with US$ 6.5 billion in annual revenues.

The firm had anticipated 2020 sales between US$ 48.8 billion and US$ 50.3 billion however this week it announced that the coronavirus pandemic will reduce 2020 sales by more than $2 billion.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

Humira holds on to remain world’s best-selling drug

AbbVie’s acquisition of Allergan comes as the firm faces the expiration of patent protection for Humira, which brought in a staggering US$ 19.2 billion in sales last year for

the company. AbbVie has failed to successfully acquire or develop a major new

product to replace the sales generated by its flagship drug.

In 2019, Humira’s US revenues increased 8.6 percent to US$ 14.86 billion while internationally, due

to biosimilar competition, the sales dropped 31.1 percent to US$ 4.30 billion.

Bristol Myers Squibb’s Eliquis, which is also marketed by Pfizer, maintained its number two position

and posted total sales of US$ 12.1 billion, a 23 percent increase over 2018.

While Bristol Myers Squibb’s immunotherapy treatment Opdivo, sold in partnership with Ono in Japan, saw sales increase from US$ 7.57 billion to US$ 8.0 billion, the growth paled in comparison to the US$ 3.9

billion revenue increase of Opdivo’s key immunotherapy competitor Merck’s Keytruda.

Keytruda took the number three spot in drug sales that

previously belonged to Celgene’s Revlimid, which witnessed a sales decline from US$ 9.69 billion to US$ 9.4 billion.

Cancer treatment Imbruvica, which is marketed

by J&J and AbbVie, witnessed a 30 percent increase in sales. With US$ 8.1

billion in 2019 revenues, it took the number five position.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

Vaccines – Covid-19 turns competitors into partners

This year has been dominated by the single biggest health emergency in years — the novel coronavirus (Covid-19) pandemic. As drugs continue to fail to meet expectations, vaccine development has received a lot of attention.

GSK reported the highest vaccine sales of all drugmakers with

total sales of US$ 8.4 billion (GBP 7.16 billion), a significant portion of its

total sales of US$ 41.8 billion (GBP 33.754 billion).

US-based Merck’s vaccine division also reported a significant increase in sales to US$ 8.0 billion and in 2019 received FDA and EU approval to market its Ebola vaccine Ervebo.

This is the first FDA-authorized vaccine against the deadly virus which causes

hemorrhagic fever and spreads from person to person through direct contact with

body fluids.

Pfizer and Sanofi also reported an increase in their vaccine sales to US$ 6.4

billion and US$ 6.2 billion respectively and the Covid-19 pandemic has recently

pushed drugmakers to move faster than ever before and has also converted

competitors into partners.

In a rare move, drug behemoths — Sanofi and GlaxoSmithKline (GSK) —joined hands to develop a vaccine for the novel coronavirus.

The two companies plan to start human trials

in the second half of this year, and if things go right, they will file

for potential approvals by the second half of 2021.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

Our view

Covid-19 has brought the world economy to a grinding halt and shifted the global attention to the pharmaceutical industry’s capability to deliver solutions to address this pandemic.

Our compilation shows that vaccines and drugs

for infectious diseases currently form a tiny fraction of the total sales of

pharmaceutical companies and few drugs against infectious diseases rank high on

the sales list.

This could well explain the limited range of

options currently available to fight Covid-19. With the pandemic currently infecting

over 3 million people spread across more than 200 countries, we can safely

conclude that the scenario in 2020 will change substantially. And so should our

compilation of top drugs for the year.

View Our Interactive Dashboard on Top drugs by sales in 2019 (Free Excel Available)

Impressions: 55104

https://www.pharmacompass.com/radio-compass-blog/top-drugs-and-pharmaceutical-companies-of-2019-by-revenues

#PharmaFlow by PHARMACOMPASS

29 Apr 2020

We always knew math was fuzzy, but never imagined addition could get so

complicated.

A recent publication on 2014 Global Prescription Medication Statistics listed the top pharmaceutical corporations by revenues, the best

selling products along with the top therapy areas.

The list, based on data published by IMS Health,

caught us by surprise since a previous publication by FiercePharma had a completely different order when ranking the top 15 pharmaceutical

companies.

As the difference in revenues of the top-10 companies was in excess of $60 billion and IMS Health’s data is an industry standard for decision making, we dug deeper to analyze the correlation between the information in the annual reports and IMS Health’s statistics.

Which pharmaceutical company is the largest?

Simply put, the answer is, ‘it depends’ on how you define a pharmaceutical company.

Should divisions like diagnostics, animal health, vaccines, consumer

health be counted when determining the size of a pharmaceutical company?

FiercePharma, in their analysis, used the total

revenue of all divisions of the organizations to determine the largest

organization; in their case it is Johnson & Johnson.

IMS determines their numbers by measuring “prescription sales and dispensing” and hence, excludes divisions like diagnostics, consumer health and animal health, making Novartis the largest

company.

As currency exchange rate fluctuations have their own, big role, in

determining the size of organizations, we believed it would be best to share

the revenues, as presented, so that you can draw your own conclusions.

Table 1/ Sales comparison for top pharmaceutical companies in 2014 from different sources (IMS, Fierce Pharma and Annual Reports)

Big Pharma

IMS Rank

IMS Sales

(US $Mn)

Fierce Pharma Rank

Fierce Pharma Sales (US $Mn)

Group Sales based on the Annual Report

(Currency as reported, Mn)

Novartis

1

51,307

2

57,996

USD

57,996

Pfizer

2

44,929

4

49,605

USD

49,605

Sanofi

3

40,037

5

43,070

Euro

33,770

Roche

4

37,607

3

49,866

CHF 49,866

Merck & Co

5

36,550

6

42,237

USD

42,237

Johnson &

Johnson

6

36,422

1

74,331

USD

74,331

AstraZeneca

7

33,313

8

26,095

USD

26,095

Glaxo SmithKline

8

31,470

7

37,960

GBP

23,006

Teva

9

26,001

11

20,272

USD

20,272

Gilead Sciences

10

23,673

10

24,474

USD

24,890

Amgen

11

20,473

12

20,063

USD

20,063

Lilly

12

19,909

14

19,615

USD 19,615

AbbVie

13

19,049

13

19,960

USD

19,960

Bayer

14

18,347

9

25,470

Euro

42,239

Bristol-Myers

Squibb

Not

in Top 20

15

15,879

USD

15,879

NB: Mn is million

Click here to access and download all

the 2014 data (Excel version available) for FREE!

Since each group has multiple divisions, we further split the sales for

you to brainstorm:

Table 2/ Sales comparison of the different divisions of top

pharmaceutical companies in 2014 (Annual Reports in Mn)

Big Pharma

Pharma Division

Vaccine Division

Generics

Consumer Health

Other Divisions

Medical Devices/ Diagnostics Division

Animal Health Division

Divestures/ Other adjustments

Novartis

USD 31,791

Sandoz USD 9,562

Alcon USD 10,827

USD 5,816

Pfizer

USD 45,708

USD 3,446

USD 451

Sanofi

Euro 22,578

Euro 3,974

Euro 1,805

Euro 3,337

Euro 2,076

Roche

CHF 38,969

CHF 10,897

Merck & Co

USD 30,740

USD 5,302

USD 6,195

Johnson &

Johnson

USD 32,313

USD 14,496

USD 27,522

AstraZeneca

USD 26,095

Glaxo SmithKline

GBP 18,670

GBP 4,336

Teva

USD 10,458

USD 9,814

Gilead Sciences

USD 24,474

USD 416

Amgen

USD

19,327

USD 736

Lilly

USD 16,481

USD 788

USD 2,346

AbbVie

USD 19,960

Bayer

Euro 12,052

Euro 7,923

Euro 22,264

Bristol-Myers

Squibb

USD 15,879

Click here to access and download all

the 2014 data (Excel version available) for FREE!

Not sure that it adds any extra clarity on what should define a global pharmaceutical company…

Since the various divisions make

companies complicated to assess, what about product sales?

The good news is that we have a winner!

Humira®, AbbVie’s monoclonal antibody Adalimumab, used to treat rheumatoid and other types of arthritis, is the highest selling product globally. IMS reported Humira’s annual sales for 2014 at $11,844 million, while AbbVie mentions their sales of Humira at $12,543 million, the difference: a mere $700 million! However, with IMS gathering data across various points of the supply chain, and the recent volatility of the currency markets, we believe that a difference of 5.5% of total sales is within range of reason.

Unfortunately, things stopped making sense the moment we reached the

number-two product on the IMS list. Lantus®,

Sanofi’s insulin glargine, recorded sales of Euro 6,344 million (based on Sanofi’s 2014 annual report), while IMS mentions Lantus sales were $10,331 million last year. In addition, Sanofi has an 11% growth rate reported while IMS indicates a growth of 30%.

So unless the Euro/Dollar exchange rate moves back towards the 1.5

range, there seems to be a serious difference in the way the product sales are

calculated by companies and by IMS.

Using information available in the annual reports and other company declarations, we attempted to compare IMS’ Top 20 Global Products 2014 with available public information, to only find more complications!

Table 3/ Sales comparison of the top pharmaceutical products in 2014 (IMS vs Annual Reports)

Products

IMS Rank

IMS Sales (US $Mn)

Annual Reports Sales (US $Mn)

Pharma

Compass Rank

Big Pharma

Currency

Annual Reports Sales in Mn

Marketing Partner

Marketing Partner Annual Report Sales

(US $Mn)

Humira®

1

11,844

12,543

1

Abbvie

USD

12,543

Lantus®

2

10,331

7,676

5

Sanofi

Euro

6,344

Sovaldi®

3

9,375

10,283

2

Gilead Sciences

USD

10,283

Abilify®

4

9,285

7,556

6

Bristol

Myers-Squibb

USD

2,020

Otsuka

5,536

Enbrel®

5

8,707

8,538

4

Amgen

USD

4,688

Pfizer

3,850

Seretide®

6

8,652

6,589

8

GSK

GBP

4,229

Crestor®

7

8,473

5,512

11

AstraZeneca

USD

5,512

Remicade®

8

8,097

9,880

3

Johnson &

Johnson

USD

6,868

Merck & Co.

2,372

Mitsubishi

Tanabe

640

Nexium®

9

7,681

3,655

19

AstraZeneca

USD

3,655

Mabthera®

10

6,552

6,936

7

Roche

CHF

5,603

Roche

1,305

Avastin®

11

6,070

6,449

9

Roche

CHF

6,417

Lyrica®

12

6,002

5,168

12

Pfizer

USD

5,168

Herceptin®

13

5,564

6,306

10

Roche

CHF

6,275

Spiriva®

14

5,483

3,917

17

Boehringer

Euro

3,237

Januvia®

15

4,991

3,931

16

Merck & Co.

USD

3,931

Copaxone®

16

4,788

4,237

14

Teva

USD

4,237

Novorapid®

17

4,718

2,835

20

Novo Nordisk

DKK

17,449

Neulasta®

18

4,627

4,596

13

Amgen

USD

4,596

Symbicort®

19

4,535

3,801

18

AstraZeneca

USD

3,801

Lucentis®

20

4,437

4,152

15

Novartis

USD

2,441

Roche

1,711

Click here to access and download all

the 2014 data (Excel version available) for FREE!

It’s clear that the methods used to determine product sales are considerably different between IMS and the pharmaceutical companies, however there is a range of consistency as well. How accurate is each information really depends on the analyst’s point of view.

Our take:

With over $350 billion in total sales, we have provided our raw data for your review since we are certain that there are opportunities worth capitalizing

upon and others, which may not be worthwhile to pursue.

While the assessment of pharmaceutical sales is far more complicated

than what we had originally imaged, the focus of Big Pharma on small molecules

is on Hepatitis C drugs (Sofosbuvir, Olysio, AbbVie Hep C), blood thinners, Eliquis® (Apixaban), Xarelto®(Rivaroxaban) and of course ‘tinib’ cancer treatments.

Table 4/ Growth of ‘tinib’ cancer treatments in 2014 (Annual Reports)

Products

Big Pharma

Sales (US $Mn) 2013

Sales (US $Mn) 2014

Growth (%)

Ibrutinib

Pharmacyclics,

Inc

(now

AbbVie)

14

492

3414%

Dasatinib

Bristol-Myers

Squibb

1280

1493

17%

Trametinib

GSK

10

68

580%

Nilotinib

Novartis

1266

1529

21%

Ruxolitinib

Novartis

163

279

71%

Ceritinib

Novartis

Not

launched

31

Sunitinib

Maleate

Pfizer

1204

1174

-2%

Crizotinib

Pfizer

282

438

55%

Axitinib

Pfizer

319

410

29%

Tofacitinib

Citrate

Pfizer

114

308

170%

Click here to access and download all

the 2014 data (Excel version available) for FREE!

However, Big Pharma is now all about biologics.

IMS’s data indicates that the top 10 products have only 5 biologics, while our calculations have 8 out of the top 10 products as biologics. The future strategy is best summed up by the statement in Bristol-Myers Squibb’s annual report “Just 5 years ago, we had about 40% of our development projects in biologics. If we look forward 3-5 years, we believe that number could potentially grow to about 75%”.

The barriers of entry for generic competition and potential windfalls have made rivals come together to co-market Synagis® (AbbVie & AstraZeneca), Remicade® (Johnson & Johnson, Merck and Tanabe), Xolair® and Lucentis® (Roche & Novartis).

Our pharmaceutical whisper (phisper): join the bio-age or bio-degrade!

Impressions: 12833

https://www.pharmacompass.com/radio-compass-blog/who-has-the-biggest-one-sales-of-the-top-pharma-products-by-revenue

#PharmaFlow by PHARMACOMPASS

23 Apr 2015