Last month, Novo Nordisk paused

all advertising for Wegovy (semaglutide) amid skyrocketing demand and short supply. The reason behind the drug’s immense popularity is its effectiveness in managing weight, a phenomenon enthusiastically promoted by social media influencers.Wegovy is a glucagon-like peptide-1 receptor agonist (also known as GLP-1 receptor agonist or GLP-1 RA), which bagged US Food and Drug Administration’s approval as a treatment for obesity in June 2021. Most other GLP-1 RAs are used to treat type 2 diabetes mellitus (T2DM).The market for GLP-1 RAs is

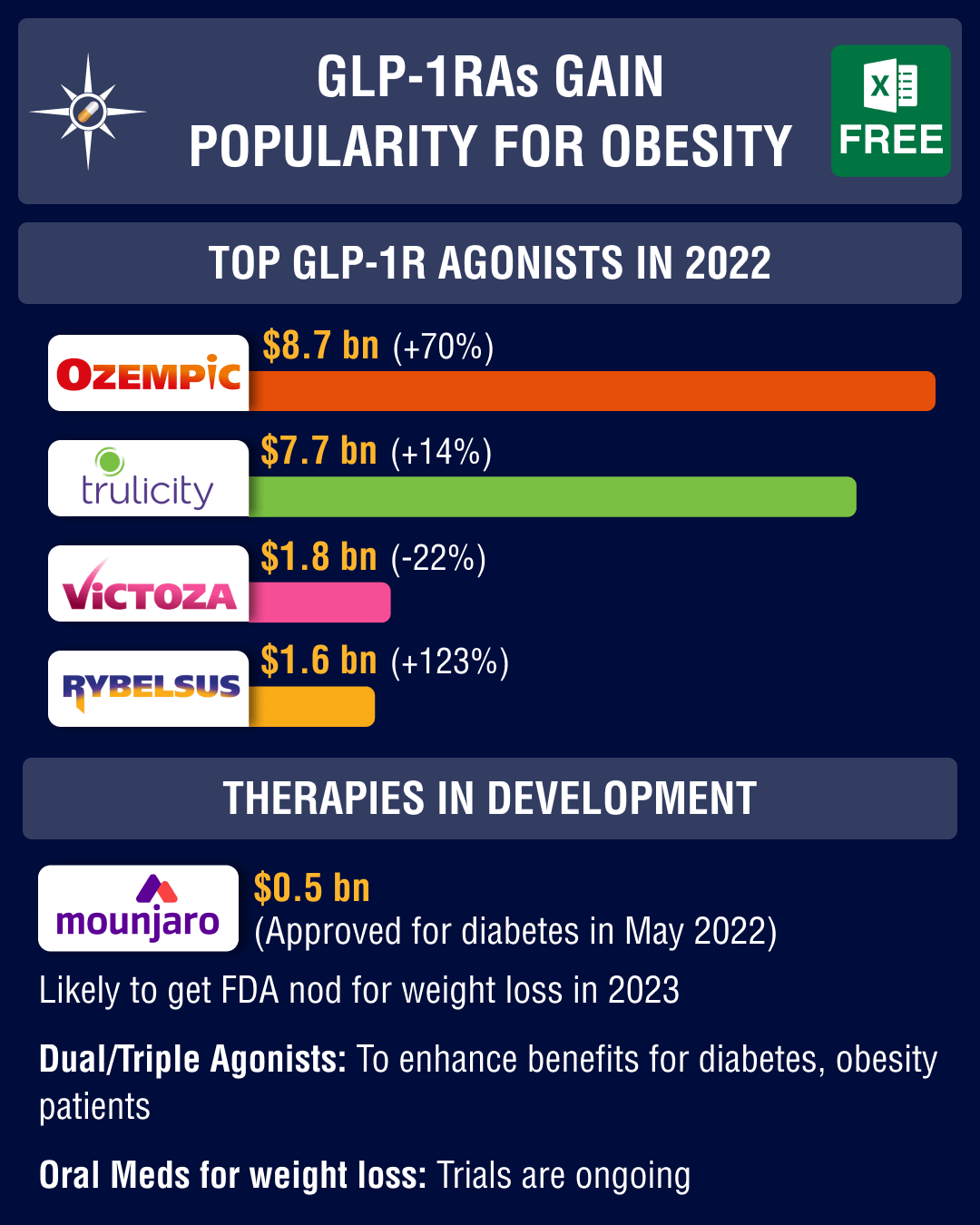

dominated by Novo Nordisk, Eli Lilly, AstraZeneca, Bristol Myers Squibb and GSK. In 2022, some of the top-selling drugs in this category were Novo’s Ozempic (US$ 8.7 billion), Lilly and

partner Dainippon Sumitomo’s Trulicity (US$ 7.7 billion), Novo’s Victoza (US$ 1.8 billion),

and Rybelsus (US$ 1.6 billion). Lilly’s Mounjaro and Novo’s Wegovy are likely to join the blockbuster list very soon.The global GLP-1 RA market is

growing at 9.6 percent per annum, and is

likely to increase from US$ 22.4 billion in 2022 to US$ 55.8 billion by 2032. According to the International Diabetes Federation,

around 537 million adults are living with diabetes. This number is predicted to

rise to 643 million by 2030 and 783 million by 2045.View Our Interactive Dashboard on GLP-1RA Therapies in Development (Free Excel Available)Inspired by Mounjaro, Zealand Pharma-BI, Amgen, Carmot work on dual

agonistsGLP-1 is an incretin, or a

gut hormone, secreted into the blood within minutes of ingesting food. The

other main incretin hormones are glucagon-like peptide 2 (GLP-2),

glucose-dependent insulinotropic polypeptide (GIP) and glucagon (a hormone

that the pancreas makes to help regulate blood glucose levels).GLP-1 RAs have been around

for some time. The first such drug — Amylin and Lilly’s exenatide — received FDA approval in April 2005 for the treatment of T2DM. Subsequently, other drugs such as Novo’s Victoza (liraglutide, approved in 2010), AstraZeneca’s Bydureon (exenatide, 2012), GSK’s Tanzeum (albiglutide, 2014), Lilly’s Trulicity (dulaglutide, 2014) and Novo’s Ozempic (semaglutide, 2017) and Rybelsus

(oral semaglutide, 2019) were approved. In 2021, FDA approved Novo’s Wegovy for chronic weight

management. Today, more than half a dozen companies, including Pfizer, Amgen and Altimmune, are working on weight-loss therapies similar to Wegovy. The field of drug development

is progressing rapidly, with numerous companies now focusing on dual and triple

agonists. In May 2022, Lilly’s Mounjaro (tirzepatide) bagged FDA approval

as the first and only approved dual agonist for the treatment of T2DM. Similar to other medications in its class, tirzepatide functions

by mimicking GLP-1. However, it also targets the GIP receptor.Mounjaro has displayed

effectiveness in promoting weight loss in a phase 3 trial against Novo’s Wegovy. In October, FDA granted fast track status to Mounjaro as a treatment for obesity.Overall, dual agonists are showing efficacy in both weight and cardiovascular risk reduction. Companies

such as Amgen (AMG 133 is in mid stage trials), Innovent Biologics and Lilly (Mazdutide, in phase 2 trials) are working on dual agonists for obesity. Carmot Therapeutics’ experimental dual agonist, CT-868, is currently in phase 2 trials for diabetes.Zealand Pharma and Boehringer Ingelheim are working on two dual agonists — dapiglutide and survodutide (BI 456906) — that are in phase

2 trials for weight loss. Last week, the duo revealed data on

survodutide, which shows benefits in weight loss. Survodutide may also have

direct effects on energy expenditure in the liver in addition to decreasing

appetite.View Our Interactive Dashboard on GLP-1RA Therapies in Development (Free Excel Available) Lilly, Hanmi work on triple agonists; GLP-1 RAs get explored for curing

NASH, CVDsApart from GLP-1 RA and dual

agonists, drugmakers like Eli Lilly and Hanmi are also working on

triple agonists. Eli Lilly is testing retatrutide that affects GLP-1, GIP and glucagon

receptors. This week, Lilly released positive results on weight loss from a

phase 2 retatrutide trial. Retatrutide could be more efficacious than tirzepatide for the treatment of

T2DM and obesity.Another triple agonist

candidate, Hanmi’s efocipegtrutide (HM15211), is in a phase 1 trial for weight loss and

in a phase 1b/2a for nonalcoholic fatty liver disease (NAFLD). In 2020, FDA

granted fast track designation to efocipegtrutide for the treatment of nonalcoholic

steatohepatitis (NASH), the most severe form of

NAFLD.Several other GLP-1

RAs are being explored as treatments for liver and heart diseases as they have shown a significant impact on clinical, biochemical and histological markers of fatty liver and fibrosis in patients with NAFLD.Another

drug that Hanmi is developing with Merck — efinopegdutide — received FDA’s fast track designation this month for the treatment of NASH. Novo is also working with Gilead on a once-weekly

subcutaneous version of semaglutide, which is currently in a phase 3 trial. Top-line data is expected in mid-2028.Lilly’s Mounjaro is also in a phase 2 trial for NASH. Other

products that are in mid- to late-stage studies for NASH are Zealand Pharma & Boehringer Ingelheim’s dapiglutide & survodutide (BI 456906) as well as Altimmune’s pemvidutide.Patients with diabetes

mellitus often suffer from cardiovascular diseases (CVDs), a leading cause of death in these patients. Of late, several clinical trials on GLP-1 RAs have been conducted to study their impact on cardiovascular episodes. Novo’s semaglutide (oral as well as subcutaneous) has shown significant cardiovascular improvement in clinical studies.View Our Interactive Dashboard on GLP-1RA Therapies in Development (Free Excel Available) Pfizer, Novo work on oral GLP-1 RAs; Lilly’s oral orfoglipron reduces weight in trialsAmong GLP-1 RAs, only Rybelsus is administered

orally. The remaining drugs are injectables that are not only more

expensive compared to oral drugs, but also difficult to scale up. However,

various companies are working on oral formulations to ensure cheaper and more

scalable options for patients worldwide. Oral GLP-1 RAs will also address shortages like the one faced by Wegovy. While Novo is working on oral

Wegovy that has shown remarkable weight loss benefits in trials, Pfizer has shared positive results for oral danuglipron. It demonstrated an efficacy and safety

profile consistent with currently available GLP-1 RAs like Wegovy in adults with T2DM. Unlike oral semaglutide, which must be taken an hour before eating food or taking other medications, Pfizer’s experimental twice-daily tablet can be taken alongside food.Lilly’s oral GLP-1 contender, orforglipron is also in a late-stage trial. Just last week, Lilly revealed new phase 2 findings for oral

orforglipron that show it can induce clinically meaningful weight reductions in overweight or obese adults.View Our Interactive Dashboard on GLP-1RA Therapies in Development (Free Excel Available) Our viewWith the rise in

urbanization, affluence and sedentary lifestyles, the incidence of diabetes,

heart and liver diseases and obesity is increasing. Some reports expect the

weight-loss market alone to reach US$ 100 billion by the end of the decade, while NASH has been estimated to be a US$ 35 billion opportunity.GLP-1 RAs and other breakthroughs, such as dual and triple agonist drugs, might be just what the 21st century lazy human body needs to circumvent the deleterious effects of lifestyle disorders.

Impressions: 2304