Market Place

Market Place Sourcing Support

Sourcing Support

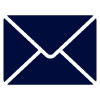

Top Pharma Companies & Drugs in 2021: Covid vaccines, pills cause churn in list

Every year, the list of top pharmaceutical products and companies by sales sees some churn. But the

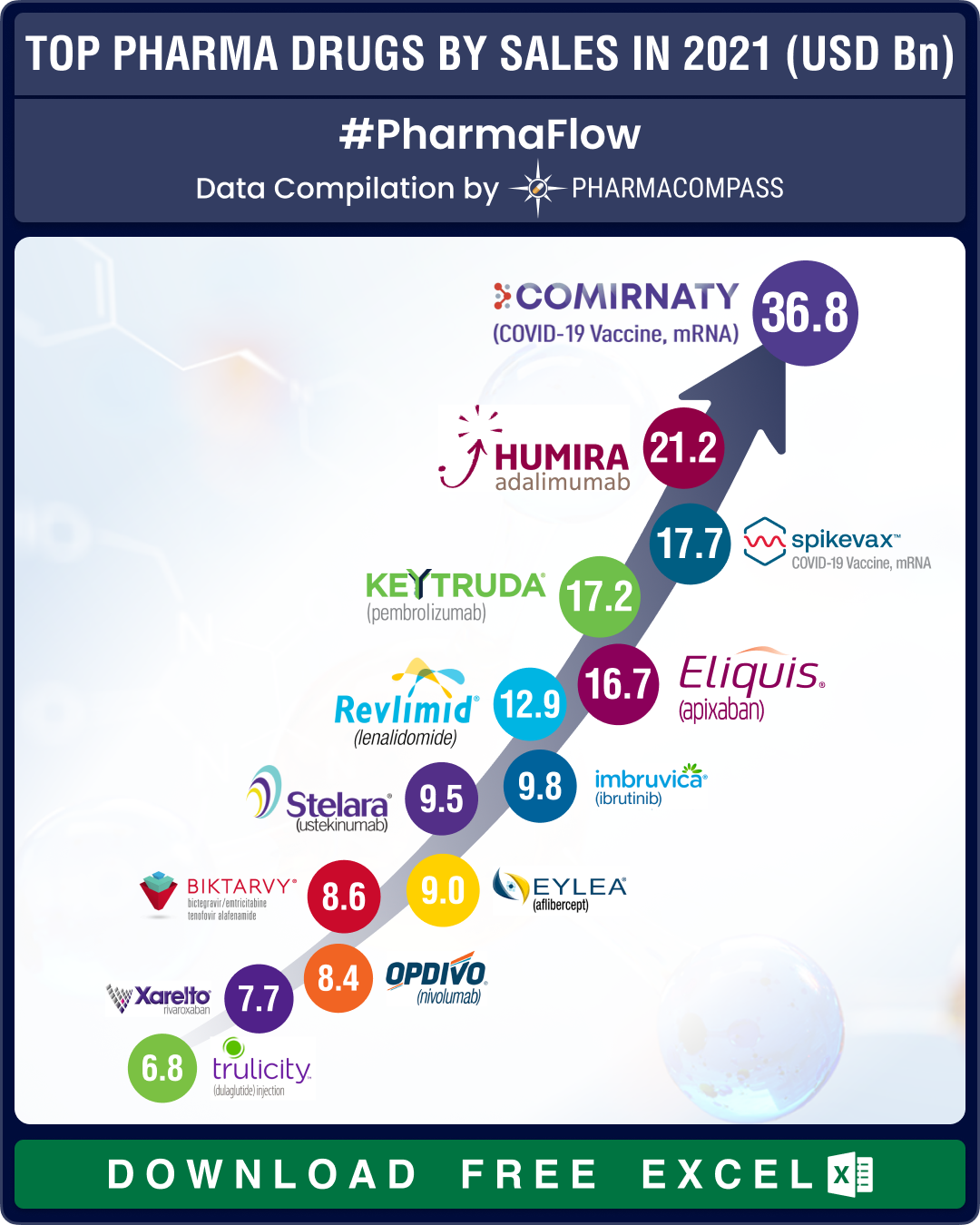

Top drugs and pharmaceutical companies of 2019 by revenues

Acquisitions and spin-offs dominated headlines in 2019 and the tone was set very early with Bristol-

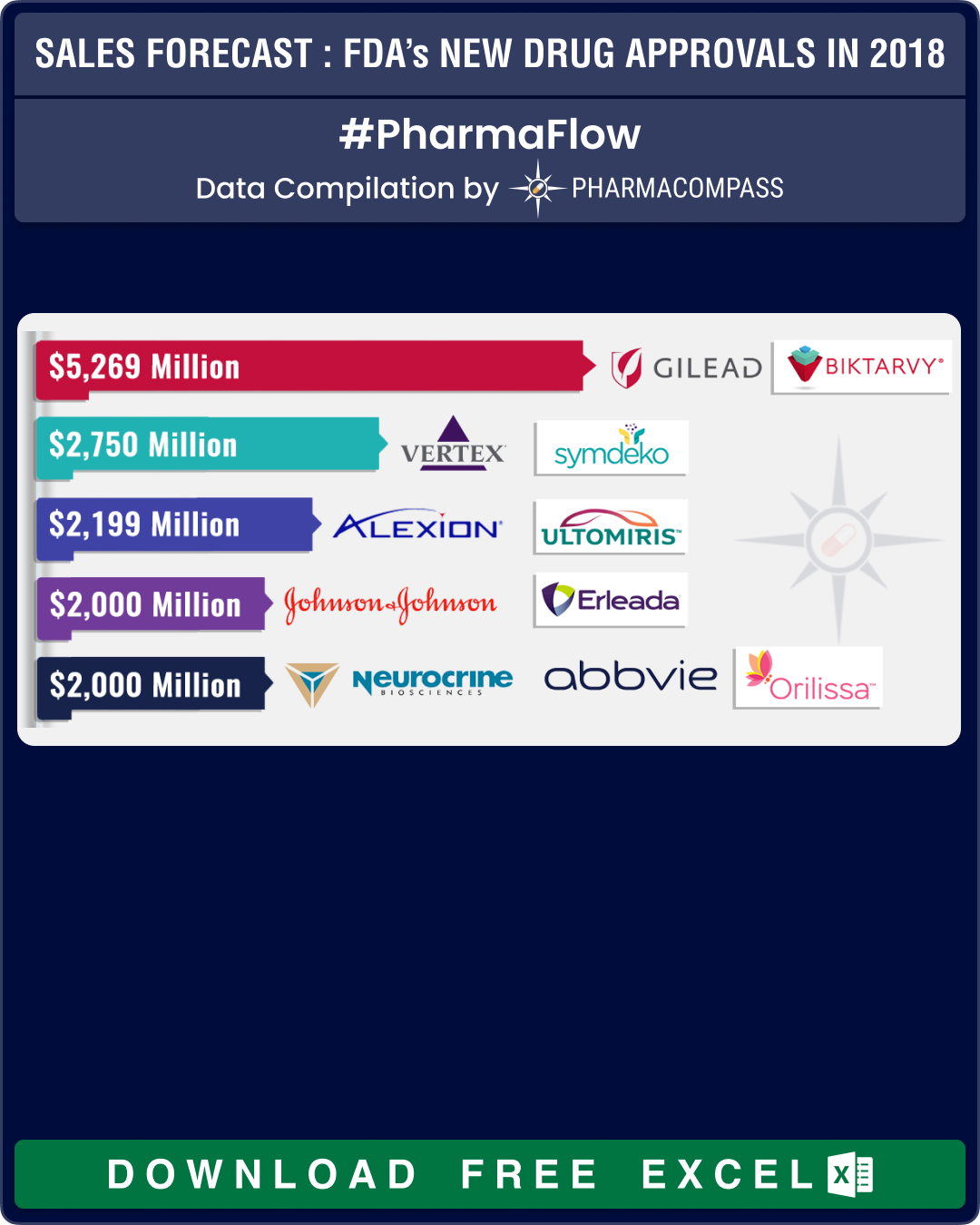

Sales Forecast of FDA’s Novel Drugs Approvals in 2018

The year 2018 was a landmark year for the US Food and Drug Administration (FDA) as the agency approv