Biologics, or complex drugs that are derived from living organisms, have revolutionized treatment of various conditions such as cancer, autoimmune diseases, and chronic illnesses. In 2023, eight out of 10 of the world’s top-selling drugs were biologics, including Merck’s Keytruda, AbbVie’s Humira, and Sanofi’s Dupixent.Due to their high costs, accessibility of biologics has been a challenge. That’s why biosimilars, or game-changing copycats of biologics that provide highly similar yet more affordable alternatives to established biologics, are becoming popular.The first biosimilar — Sandoz’ Zarxio — was approved by the US Food and Drug Administration (FDA) in 2015. Its reference biologic was Amgen’s Neupogen (filgrastim). Since then, the global market for biosimilars has been growing at an impressive pace — between 2015 and 2020, it grew at a whopping compounded annual growth rate (CAGR) of 78 percent, touching US$ 17.9 billion in size. It is expected to continue growing at a CAGR of 15 percent and reach a size of about US$ 75 billion by 2030.Major

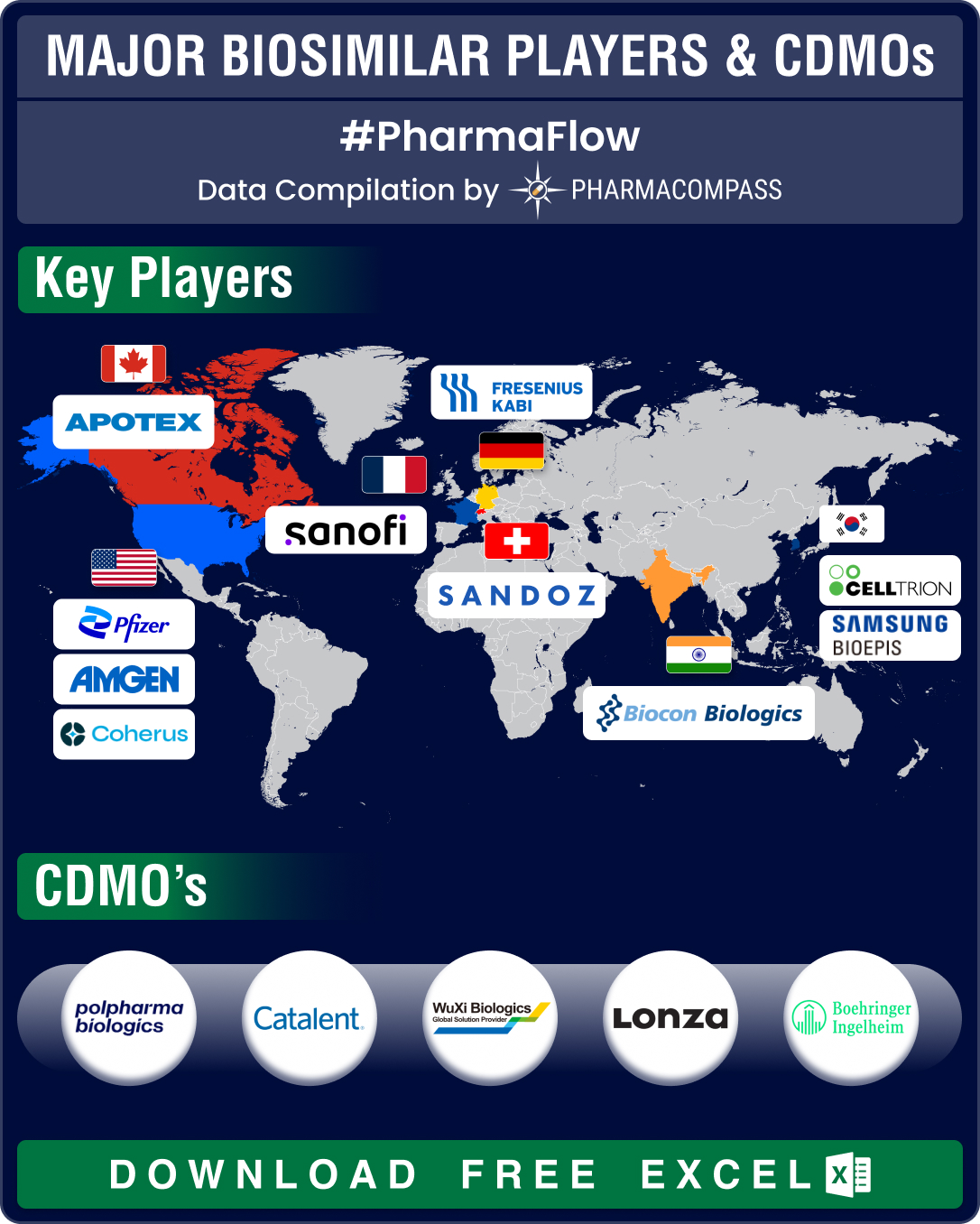

biosimilar players include Amgen, Sandoz, Samsung Bioepis, Pfizer, Biocon Biologics, Celltrion, Stada Arzneimittel, Accord Healthcare, Fresenius Kabi, Coherus Biosciences, Apotex, and Sanofi. The increasing demand for

biosimilars has propelled growth in contract manufacturing. Some of the

leading contract manufacturing organizations (CMOs) and contract development

and manufacturing organizations (CDMOs) that manufacture biosimilars are Polpharma Biologics, Catalent, Pfizer CentreOne, Lonza, Boehringer Ingelheim BioXcellence, Thermo Fisher Scientific, WuXi Biologics, and FUJIFILM Diosynth

Biotechnologies.Access the Interactive Dashboard for Biosimilar Developments (Free Excel)Amgen, Sandoz top list of ‘approved biosimilars’; FDA okays 8 copycats in H1 2024Over

the recent years, regulatory agencies like the FDA

and the European Medicines Agency (EMA) have established rigorous approval pathways for biosimilars.Since 2015, FDA has

approved 53 biosimilars, while the EMA has approved 86 biosimilars. Among the US, European and

Canadian markets, Amgen and Sandoz are tied in the first place

with 13 approved biosimilars each. Samsung Biologics has nine approved

biosimilars, followed by Pfizer with eight and Biocon Biologics with seven. In the first half of this year, FDA set a record by approving eight biosimilars — the highest for H1 of any year. EMA has okayed six biosimilars so far in 2024.In 2023, five biosimilars were approved by the FDA with just one

being okayed in the first half. The year marked the end of exclusivity for Humira after 20 years, in which it

netted a total of US$ 200 billion in sales. AbbVie’s flagship autoimmune drug has a record 10 biosimilars.Johnson & Johnson’s Stelara also lost exclusivity in 2023 and as many as 11

drugmakers hope to bring its biosimilars to the market. Amgen’s Wezlana was the first biosimilar to

Stelara, and it was approved as interchangeable by FDA in October last year.Access the Interactive Dashboard for Biosimilar Developments (Free Excel) FDA approves first

interchangeable biosimilar for Eylea, cuts regulatory feeDeveloping a biosimilar costs both money and time. According to

Pfizer, developing a biosimilar can take five to nine years and cost over US$ 100 million, not including regulatory fees.In October 2023, FDA slashed its fees with the program fee at US$ 177,397, down from US$ 304,162. The application fees for products that require clinical data has been set at US$ 1,018,753, down from US$ 1,746,745. The application fee for products that don’t require clinical data has been set lower — at US$ 509,377 — down from US$ 873,373 set earlier. This reduction in application fee has propelled demand for contract manufacturing of biosimilars.There has also been a rise in approvals of interchangeable

biosimilars this year. Interchangeable biosimilars meet additional requirements

and may be substituted for its reference product by a pharmacist without

consulting the prescriber. This year saw FDA approve the first interchangeable biosimilars for bone cancer

drug denosumab (Prolia and Xgeva) in

Jubbonti and Wyost as well as for eculizumab (Soliris) in Bkemv.In May, FDA approved the first interchangeable biosimilars

for eye drug aflibercept (Eylea) in Opuviz and

Yesafili. Other biosimilars approved in 2024 include Simlandi for adalimumab (Humira), Tyenne for tocilizumab (Actemra), Selarsdi for ustekinumab (Stelara), and Hercessi for trastuzumab (Herceptin).Access the Interactive Dashboard for Biosimilar Developments (Free Excel) Merck’s Keytruda, BMS’ Opdivo, Novartis’ Cosentyx brace for biosimilar competitionHealthcare spending in the US is projected to rise from US$ 4.5

trillion in 2022 to US$ 6 trillion by 2027. While biologics involve just two

percent of prescriptions, they account for 46 percent of all pharmaceutical

spending. In 2022, US$ 252 billion was spent on biologics.Biosimilar-related savings in 2023 were estimated to be US$ 9.4

billion in the US and € 10 billion (US$ 10.68 billion) in Europe. With expensive and widely used drugs like AbbVie’s Humira, J&J’s Stelara, and Regeneron’s Eylea coming under competition, US

savings are projected to reach US$ 181 billion through 2027. Between 2026

and 2032, about 39 blockbusters are set to lose exclusivity in the US and Europe. Merck’s Keytruda (pembrolizumab) was the world’s top-selling drug last year, generating US$ 25 billion in sales. Its patent is set to expire in 2028 with sales expected to drop

19 percent to US$ 27.4 billion in 2029 from US$ 33.7 billion the previous year. Samsung

Bioepis and Amgen initiated phase 3 trials of pembrolizumab in April

and May of this year, respectively.Opdivo (nivolumab), belonging to the same

class of drugs, competes with Keytruda and is also set to lose patent

protection in 2028. It hauled in US$ 10 billion in total global sales in 2023

for Bristol Myers Squibb. The key patents of Novartis’ Cosentyx (secukinumab) are set to expire between

2025 and 2026. Cosentyx saw sales of US$ 5 billion in 2023. Taizhou Mabtech Pharmaceutical and Bio-Thera Solutions are conducting phase 3 trials of secukinumab.Access the Interactive Dashboard for Biosimilar Developments (Free Excel) Our viewWith

over 2 billion people worldwide unable to access life-saving medicines,

biosimilars hold the key to healthcare accessibility. In 2023, a record 13 biosimilars were launched in the market — the highest for a single year. And this included nine much-anticipated biosimilars to AbbVie’s Humira. In April this year, FDA announced a Biosimilars Action Plan to streamline the development of biosimilars. With a sharp focus on biosimilars, we expect more records to be broken in the near term. New launches of biosimilars to drugs like J&J’s Stelara, Regeneron’s Eylea and Merck’s Keytruda will surely help in creating new records.

Impressions: 1447

https://www.pharmacompass.com/radio-compass-blog/fda-approves-record-eight-biosimilars-in-h1-2024-okays-first-interchangeable-biosimilars-for-eylea

#PharmaFlow by PHARMACOMPASS

27 Jun 2024

The pharma industry clearly recalibrated itself in 2023, turning its focus away from Covid and onto two of the biggest threats to human health – obesity and cancer. The top lines of the major pharma companies reflect this shift in focus.We

always knew that Pfizer’s record US$ 100 billion revenue for 2022 wasn’t sustainable. Even though Pfizer’s 2023 sales were lower by nearly 42 percent against its 2022 sales, the New York-headquartered drugmaker managed to retain its pole position. The two main reasons behind its ‘top of the charts’ sales of US$ 58.5 billion were Pfizer’s record nine new molecular entity approvals by the US

Food and Drug Administration (FDA) and the launch of its vaccine for

respiratory syncytial virus (RSV).Johnson & Johnson came second with sales of US$ 54.8

billion (excluding its consumer business and MedTech units). AbbVie took bronze despite Humira being subject to biosimilar competition

and Merck maintained its fourth position. Roche nabbed the fifth position from Novartis (which stood sixth). Bristol Myers Squibb maintained its position at seven, as did

AstraZeneca (eighth) and Sanofi (ninth). And Eli Lilly bumped into the tenth spot, knocking out

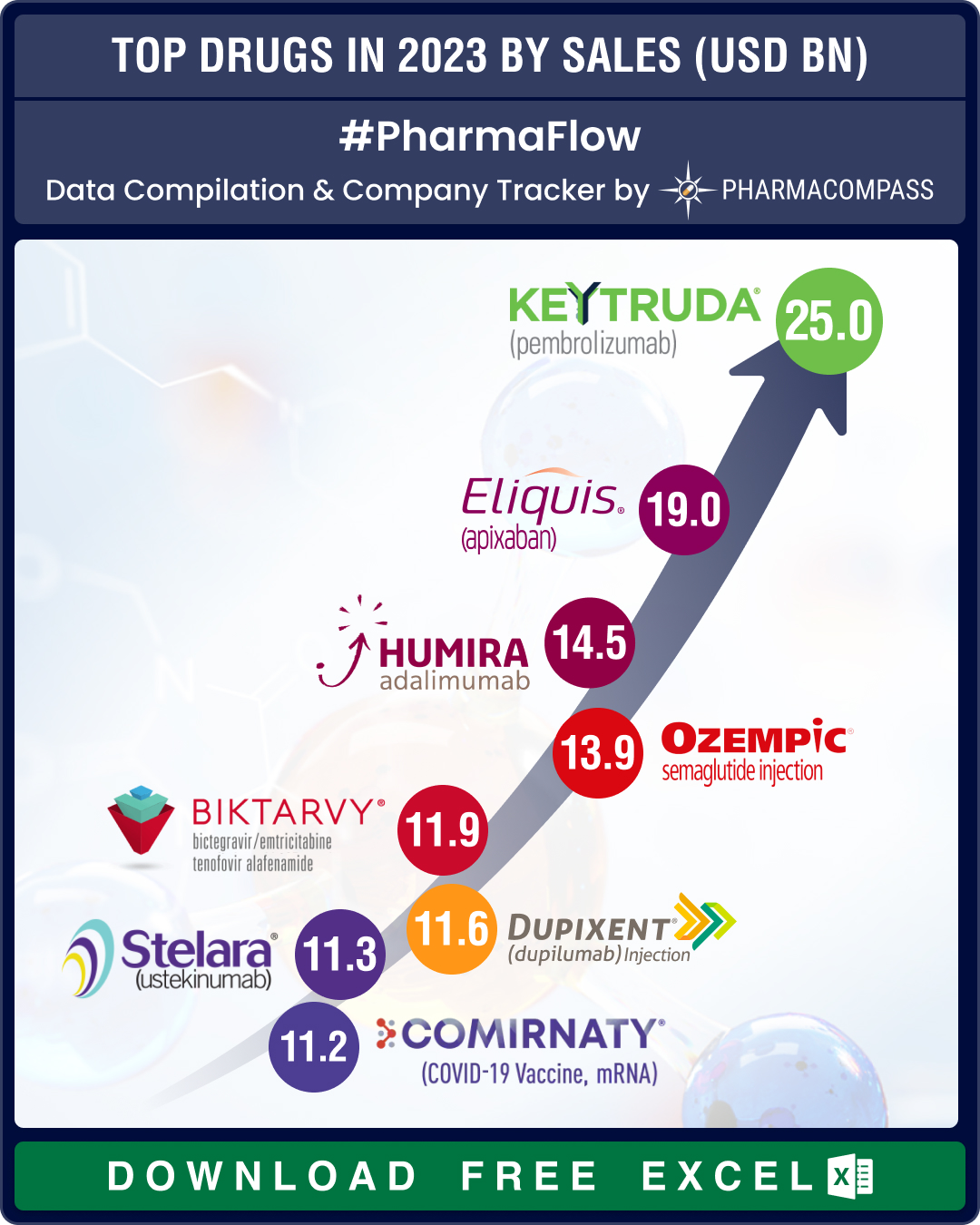

GSK.View Our Interactive Dashboard on Top Drugs in 2023 by Sales (Free Excel Available)Keytruda, Eliquis, Humira top charts; Novo’s Ozempic debuts top 10 list at number fourMerck’s Keytruda became the number one selling drug in the world, a position that was held

by AbbVie’s Humira for long, and Pfizer’s Comirnaty in the Covid years. This

oncology drug raked in a whopping US$ 25 billion, with sales increasing 19 percent last

year. In fact, Keytruda accounted for 46.7 percent of Merck’s pharmaceutical sales, which grew 3 percent in 2023 to US$ 53.6 billion.At number two was

Pfizer and BMS’ anticoagulant Eliquis — it posted global sales of US$

18.95 billion (marking a

growth of 4

percent on 2022 sales). With

competition from generics, Humira’s sales fell by 32 percent to US$ 14.5 billion. As a result, this

blockbuster anti-rheumatic drug fell to the third rank.The

fourth spot was taken up by Novo Nordisk’s Ozempic, the wonder drug that treats type 2

diabetes. Gilead’s Biktarvy, a med that treats HIV-1, saw sales jump 14 percent — from US$ 10.39 billion posted in 2022 to US$ 11.85 billion last year. This way, Biktarvy emerged as

the fifth largest selling drug of 2023.At

number six was Sanofi and Regeneron’s Dupixent. This allergic diseases med posted

11-figure sales in 2023, netting € 10.72 billion (US$ 11.59 billion) globally, a growth of 34 percent over

2022 numbers.At

number seven was J&J’s biggest blockbuster immunology drug Stelara that raked in US$ 11.3 billion in 2023. Coming a close eighth was Pfizer-BioNTech’s Covid-19 vaccine Comirnaty — its sales fell by over 70 percent to US$ 11.22 billion in 2023. At the ninth spot was Lilly and Boehringer’s diabetes drug Jardiance that saw a 27.7 percent increase in

total global sales at US$ 10.6 billion. And rounding off the list at number 10

is BMS’s Opdivo, a Keytruda rival. Opdivo hauled in US$ 10 billion

in total global sales in 2023, a year-on-year increase of 8 percent.View Our Interactive Dashboard on Top Drugs in 2023 by Sales (Free Excel Available)Driven by diabetes, obesity care meds,

Novo, Lilly post double-digit sales growthDemand

for diabetes and new weight-loss drugs catapulted Novo Nordisk to emerge as the most valuable public

company in Europe. Its net sales zoomed 31 percent to DKK 232.3 billion (US$ 33.75 billion) compared to DKK 177

billion (US$ 25.8 billion) in 2022. Net profit jumped 51 percent to DKK 83.68 billion (US$ 12.51 billion) in 2023 from DKK

55.5 billion (US$ 8.32

billion) in 2022 — the highest annual profit for the Danish drugmaker in over three decades.The

growth was driven by Ozempic, whose sales spiked 60 percent in 2023

to DKK 95.7 billion (US$ 13.91 billion), from DKK 59.8 billion (US$ 8.71 billion) the

year before.Rival

Eli Lilly’s revenue grew 20 percent in 2023 to US$ 34.1 billion from US$ 28.5 billion in 2022. Mounjaro turned out to be a star for the

Indianapolis drugmaker with its sales rocketing 970 percent in 2023 to US$ 5.16 billion. FDA also approved it to treat obesity

under the brand name Zepbound in November, which brought in additional

revenues of US$ 176 million.View Our Interactive Dashboard on Top Drugs in 2023 by Sales (Free Excel Available) GSK’s RSV jab makes strong debut; AbbVie’s immunology drugs post steep growthGSK’s Arexvy was the first RSV vaccine approved by the FDA. It made a strong debut — Arexvy contributed £ 1.2 billion (US$ 1.5 billion) to GSK’s sales in just four months.AbbVie posted another solid financial year.

Though the drop in Humira revenue was offset by two newer

immunology blockbuster drugs, Skyrizi and Rinvoq, the Illinois-headquartered drugmaker

did posted a marginal decrease in revenue of 6.4 percent to US$ 54.3 billion. However, revenue from Skyrizi soared 50 percent to US$ 7.8 billion,

while Rinvoq’s sales increased 57 percent to US$ 4

billion. AbbVie expects a combined US$ 16 billion from Skyrizi (US$ 10.5 billion) and Rinvoq (US$ 5.5 billion) sales in 2024. BMS attributed its 2 percent decrease in

revenue (of US$ 45 billion) to lower sales of Revlimid in the US due to competition from

generics. Sales of the multiple myeloma treatment dropped 39 percent to US$ 6.1

billion. Ophthalmology drug Eylea saw a drop in sales of

4 percent, at US$ 9.21 billion (from US$ 9.65 billion), as competition from Roche’s Vabysmo triggered a price cut by Regeneron. Vabysmo saw sales balloon 324 percent

from CHF 591 million (US$ 685.56 million) to CHF 2.4 billion (US$ 2.78 billion) in 2023.View Our Interactive Dashboard on Top Drugs in 2023 by Sales (Free Excel Available) Our viewAccording

to data analytics company GlobalData, GLP-1 agonist drugs (such as Ozempic and Mounjaro that treat type 2 diabetes) are slated to overtake PD-1 antagonists (such as oncology drugs

Keytruda and Opdivo) as the top-selling drugs on the market

in 2024. It estimates a robust compounded annual growth rate (CAGR) of 19.2

percent from 2023 to 2029 for GLP-1 drugs that seem to have more benefits

besides bringing down blood sugar levels (such as weight management, benefits

to the heart etc).The

market size for GLP-1 is likely to increase to US$ 105 billion by 2029. In

contrast, the data firm projects a CAGR of 4.7 percent in the PD-1 antagonist

market, with its market size projected to be around US$ 51 billion in 2029.

Given these projections, we are likely to see more movers and shakers in our

top 10 drug list this year.

Impressions: 3048

https://www.pharmacompass.com/radio-compass-blog/top-pharma-companies-drugs-in-2023-merck-s-keytruda-emerges-as-top-selling-drug-novo-lilly-sales-skyrocket-due-to-glp-1-drugs

#PharmaFlow by PHARMACOMPASS

25 Apr 2024

Every year, the list of top pharmaceutical products and companies by sales sees some churn. But the year 2021 was a lot different — it saw the pharma industry landscape change dramatically. It was a

year when the industry was busy developing vaccines and therapies so that the

world could recover from the Covid-19 pandemic. And this resulted in many

drugmakers raking in billions of dollars in sales.

As a result,

the top company of 2020 in terms

of pharmaceutical sales — Roche — slipped to the number five spot, while Pfizer, which was at number eight in 2020 after

spinning off its generic business, moved up to the number one slot.

The year

proved to be a good one for pharmaceutical companies.

Interestingly, last year none of the top 20 pharmaceutical companies saw a decline in

their revenue.

View Our Interactive Dashboard on Top Drugs by Sales in 2021 (Free Excel Available)

Pfizer’s Comirnaty steals the show

The

company that reaped the maximum gains from its Covid vaccine was Pfizer.

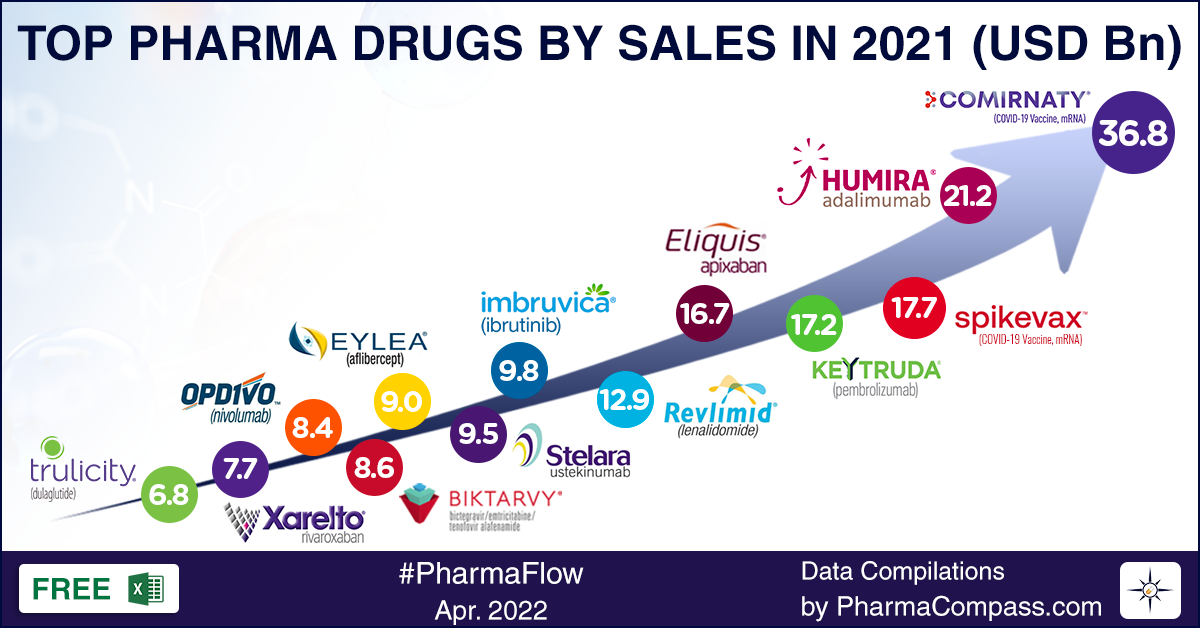

Comirnaty (tozinameran) was the top selling pharmaceutical

product of 2021, posting global revenues of US$ 36.8 billion. This

messenger-RNA Covid-19 vaccine, developed along with its German partner BioNTech, catapulted Pfizer to the slot of the top company by sales in 2021. Pfizer’s global topline grew from US$ 41.7 billion in 2020 to US$ 81.3 billion in 2021.

In

2020, Pfizer was at

number eight, behind Roche, Novartis, GSK, AbbVie, J&J, Merck and BMS. In 2021, it took a lead of billions of dollars on all these companies. The second largest drug company by sales — AbbVie — was way down at US$ 56.1 billion in global revenues. In fact, Comirnaty has

become the fastest-selling drug in the history of the pharmaceutical

industry.

Back in

December 2020, when both Comirnaty and Moderna’s Spikevax had bagged the US Food and Drug Administration’s emergency use authorization (EUA), there was a lot of uncertainty around how the promised doses would be delivered across the world. But both Comirnaty and Spikevax have proven to be a resounding success. Spikevax emerged as the third largest selling pharmaceutical product of 2021, bringing in US$ 17.7 billion for Moderna.

Analysts

expect both Pfizer-BioNTech and Moderna to sell even more vaccines in

2022. The reasons are manifold. First, SARS-CoV-2 is able to mutate often, and

is unlikely to be eradicated in the near future, creating a need for booster

shots. Second, the younger age groups are still to get vaccinated.

Along with

Comirnaty, Pfizer is battling Covid-19 with its antiviral pill, Paxlovid. Though the sales of Paxlovid have nosedived of late, Pfizer expects

Comirnaty and Paxlovid to help the New York-headquartered drug behemoth achieve US$ 100 billion

in 2022 revenues.

View Our Interactive Dashboard on Top Drugs by Sales in 2021 (Free Excel Available)

AbbVie

moves up, sans Covid product; Roche slips to number five

With no

Covid-19 related products, AbbVie did fairly well in 2021 — it moved up from the number four spot in 2020 to number two position, thanks to its Allergan acquisition, cash cow Humira (adalimumab), the continued success of its

cancer drug Imbruvica (ibrutinib) and an increase in sale of its psoriasis treatment Skyrizi (risankizumab) by a whopping 85 percent in 2021. Humira brought in sales of US$ 21.2 billion for AbbVie in 2021. However, things may change soon, with biosimilars of Humira slated to enter the market in 2023. The years 2022 and 2023 are likely to be transition years for AbbVie, as it works to build the market for its Humira successors — Rinvoq and Skyrizi.

Roche

emerged as a big loser in 2021, as several copycats of its blockbuster drugs

hit the market. Copycats to Roche’s three blockbuster cancer drugs—Avastin, Herceptin and Rituxan—eroded US$ 4.9 billion (CHF 4.73 billion) from the company’s sales in 2021. A large chunk

of growth for Roche came from its multiple sclerosis med Ocrevus, hemophilia drug Hemlibra, inflammatory disease therapy Actemra and PD-L1 inhibitor Tecentriq. The pandemic resulted in

lower-than-expected sales of Ocrevus (ocrelizumab) due to fears around its

immunosuppressive effects.

Like Roche, Novartis also slipped last year. It fell from

number two in 2020 to the number four slot in 2021. Essentially, Novartis is

struggling with a relatively lackluster pipeline. It had sold its 33 percent stake in Roche last

year for US$ 20.7 billion. It plans to use that sum for acquisitions in order

to beef up its pipeline. The Swiss drugmaker has also drawn up a restructuring

plan that includes layoffs of thousands of employees.

Before the

pandemic, Merck’s Keytruda was touted as the drug that would overtake

Humira at the top in 2024. The checkpoint inhibitor has continued to grow

impressively, adding new indications and treatment lines. Keytruda is now used

in close to 40 indications. With US$ 17.2 billion in sales, Keytruda emerged as

the fourth largest selling drug of 2022.

Overall

though, Merck slipped from number six to the number eight slot. This was due to

the fact that Merck had spun out its women’s

health, biosimilars and established brands businesses into Organon. However, its Covid-19 antiviral pill — Molnupiravir — was able to compensate for the lost revenue. Though the FDA is yet to grant the drug a full approval (it bagged an EUA in December 2021), advance sales agreements helped it rack up US$ 952 million in sales in the fourth quarter.

View Our Interactive Dashboard on Top Drugs by Sales in 2021 (Free Excel Available)

BMS moves

up with Eliquis, Revlimid; J&J lands at number three

Bristol Myers Squibb (BMS) moved up from number seven in 2020 to number six, thanks to two of its drugs that made it to top 10 — anticoagulant Eliquis at number five and oncology drug Revlimid at number six. However, Revlimid will soon face competition — four generic companies now have the approval to sell their versions of Revlimid (lenalidomide) after March 2022. Revlimid

sales are expected to drop from US$ 12.9 billion to just US$ 2.06 billion in

2026.

BMS posted

US$ 46.4 billion in global revenues, a nine percent increase from US$ 42.5

billion reported in 2020. In immuno-oncology, Opdivo

brought in US$ 7.52

billion in sales, while Yervoy drew in sales of US$ 2 billion

(an increase of 20 percent).

J&J’s pharma division brought in US$ 52.1 billion in revenues

last year, an increase of 14 percent over its revenues of US$ 45.6 billion

posted in 2020. Drugs like Darzalex (for multiple myeloma), Stelara and its Covid-19 vaccine brought in growth during 2021,

helping J&J move up from number five to the number three slot. J&J’s Covid-19 vaccine brought in US$ 2.4 billion in

sales.

View Our Interactive Dashboard on Top Drugs by Sales in 2021 (Free Excel Available)

GSK bags

approval for shingles vaccine; Takeda suffers setbacks

GlaxoSmithKline (GSK) slipped four places — from number three in 2020 to number seven in 2021. Though GSK did not have a drug in the top 10, sales of GSK and Vir Biotechnology’s Covid-19 antibody treatment

sotrovimab helped produce a seven percent increase in its 2021 revenue. The British drugmaker also bagged a critical FDA approval — its vaccine to prevent shingles (herpes zoster), Shingrix, bagged the agency’s nod in July. GSK hopes to double the sales of Shingrix by 2026.

GSK is also undergoing a major transformation, and plans to demerge its consumer health unit this year. The unit generated revenues of £9.6 billion (US$ 13 billion) last year, and GSK sees the demerger as a necessary step to fuel growth through the development of new vaccines and specialty medicines.

Sanofi managed to retain its ninth slot, even as

its global turnover increased from US$ 39.3 billion (Euro 36.04 billion) to US$

41.6 billion (Euro 37.76 billion). It snapped up Kymab, Tidal Therapeutics, Translate Bio, Kadmon Holdings, Origimm Biotechnology and Amunix in deals that bolstered its presence in immunology, immuno-oncology and vaccines. Dealmaking is on the French drugmaker’s menu for 2022 and beyond, Sanofi’s CFO said at this year’s virtual JP Morgan Healthcare Conference.

AstraZeneca’s global revenues grew from US$ 26.6 billion in 2020 to US$ 37.4 billion in 2021. However, its rank fell from nine in 2020 to 10 in 2021.

AstraZeneca

wrapped up the US$ 39 billion acquisition of Alexion in July 2021. Alexion’s rare disease franchise—led by C5 inhibitors Soliris and Ultomiris—added an extra US$ 3.1 billion to Astra’s top line last year.

Takeda suffered several clinical and regulatory setbacks in 2021, which it labeled as an “inflection year.” For Gilead, sales of its Covid-19 antiviral Veklury brought in US$ 5.6 billion last year,

helping its revenues grow by 11 percent.

View Our Interactive Dashboard on Top Drugs by Sales in 2021 (Free Excel Available)

Our view

If anything,

the pandemic has taught us that change is the only constant. It has also taught

us that products can become blockbusters in a matter of a few months.

The industry

landscape continues to change. On the one hand, we are seeing people scrambling

to get Covid vaccines and booster shots, on the other hand, the FDA has limited the use of monoclonal antibodies, such as Eli Lilly’s bamlanivimab and etesevimab and

Regeneron’s REGEN-COV (casirivimab and

imdevimab), in treating Covid caused by the Omicron variant. The FDA has also pulled the authorization

granted to GSK and Vir Biotechnology’s antibody therapy this month,

citing data that suggested it was unlikely to be effective against the dominant

Omicron sub-variant.

And last

week, there was news that demand for Pfizer’s

antiviral pill Paxlovid has remained unexpectedly low. The supply

of Paxlovid, which reduced hospitalizations or deaths in high-risk patients by

around 90 percent in a clinical trial, has far outstripped demand in many

countries like the US, the UK and South Korea.

Though Pfizer is hopeful of crossing US$ 100 billion in revenue this

year, much depends on how the pandemic pans out and what new research has to

say about the novel coronavirus. A lot will change once the pandemic becomes endemic.

The first four months of 2022 tell us that vaccines like Comirnaty and Spikevax

will continue to perform well.

But two years down the line, our charts could look very different.

Impressions: 8048

https://www.pharmacompass.com/radio-compass-blog/top-pharma-companies-drugs-in-2021-covid-vaccines-pills-cause-churn-in-list

#PharmaFlow by PHARMACOMPASS

28 Apr 2022