Market Place

Market Place Sourcing Support

Sourcing Support

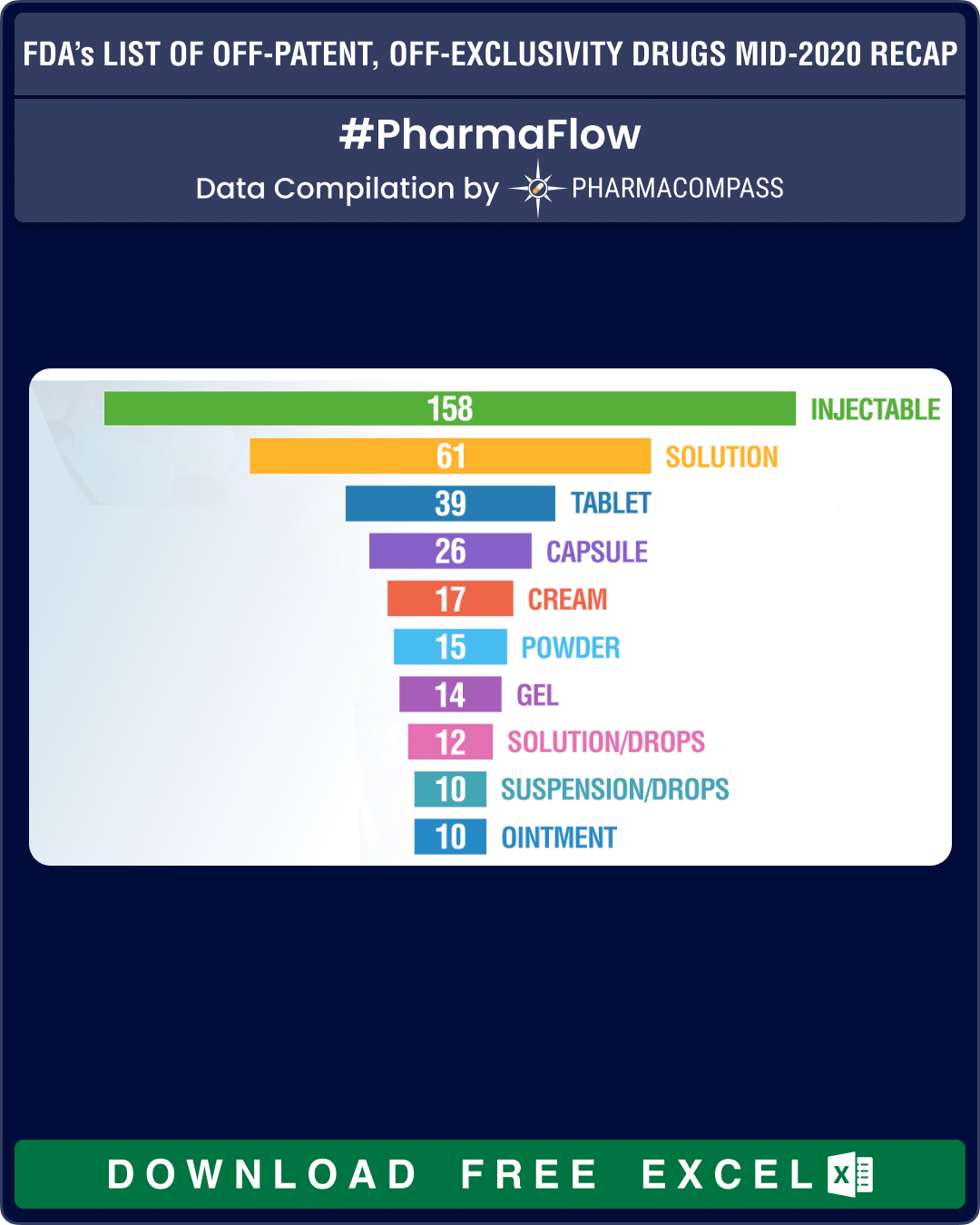

USFDA’s list of drugs that need generic alternatives

In

its continuous endeavor to bolster the competitiveness of the generics

market, the US Food

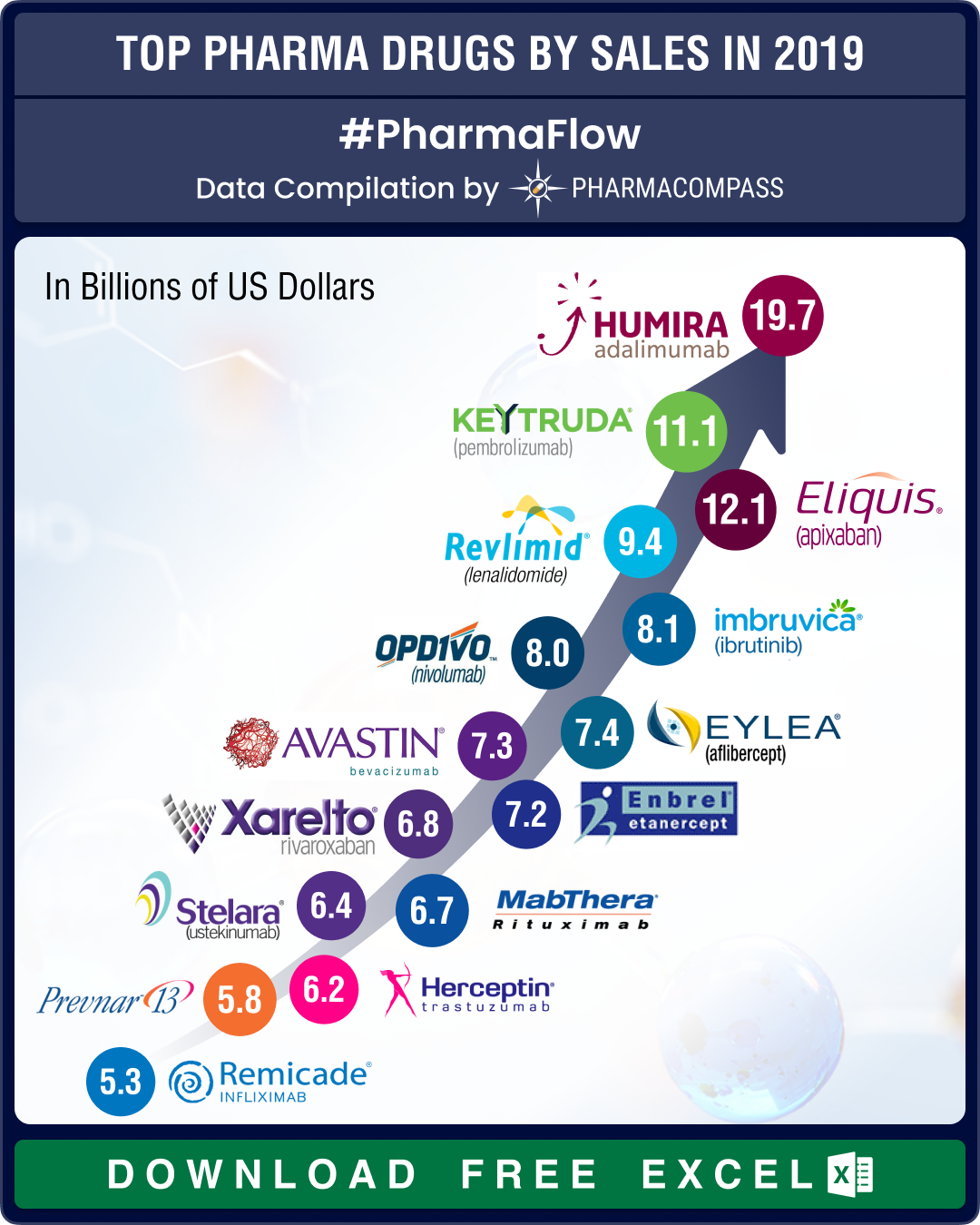

Top drugs and pharmaceutical companies of 2019 by revenues

Acquisitions and spin-offs dominated headlines in 2019 and the tone was set very early with Bristol-

Teva plans 10,000 job cuts, former CEO cites reasons for the downfall; Data-integrity concerns emerge in India and Bangladesh

In the third last week of 2017, Phispers takes a look at the steps being taken by Teva’s new C

After beef, India may ban gelatin capsules; GSK, Gilead’s HIV race heats up

This

week in Phispers, we bring you the latest twists in the GSK-Gilead rivalry over

HIV drugs. Indi

Counterfeit drugs: Toyota’s highest ranking female employee arrested; it’s time to understand!

Yesterday, on July 1, 2015, the Drug Supply

Chain Security Act (or Drug Quality

and Security Act) b

Can Cimetidine, a common antacid, be repurposed for cancer?

A clinical study published in one of the leading oncology journals, Cancer, shows that Cimetidine c

Fondaparinux –An Opportunity Worth Developing

A recent study published in the Journal of the American Medical Association (JAMA) showed that pati