Market Place

Market Place Sourcing Support

Sourcing Support

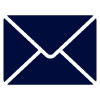

FDA approves record eight biosimilars in H1 2024; okays first interchangeable biosimilars for Eylea

Biologics, or complex drugs that are derived from living organisms, have revolutionized treatment of

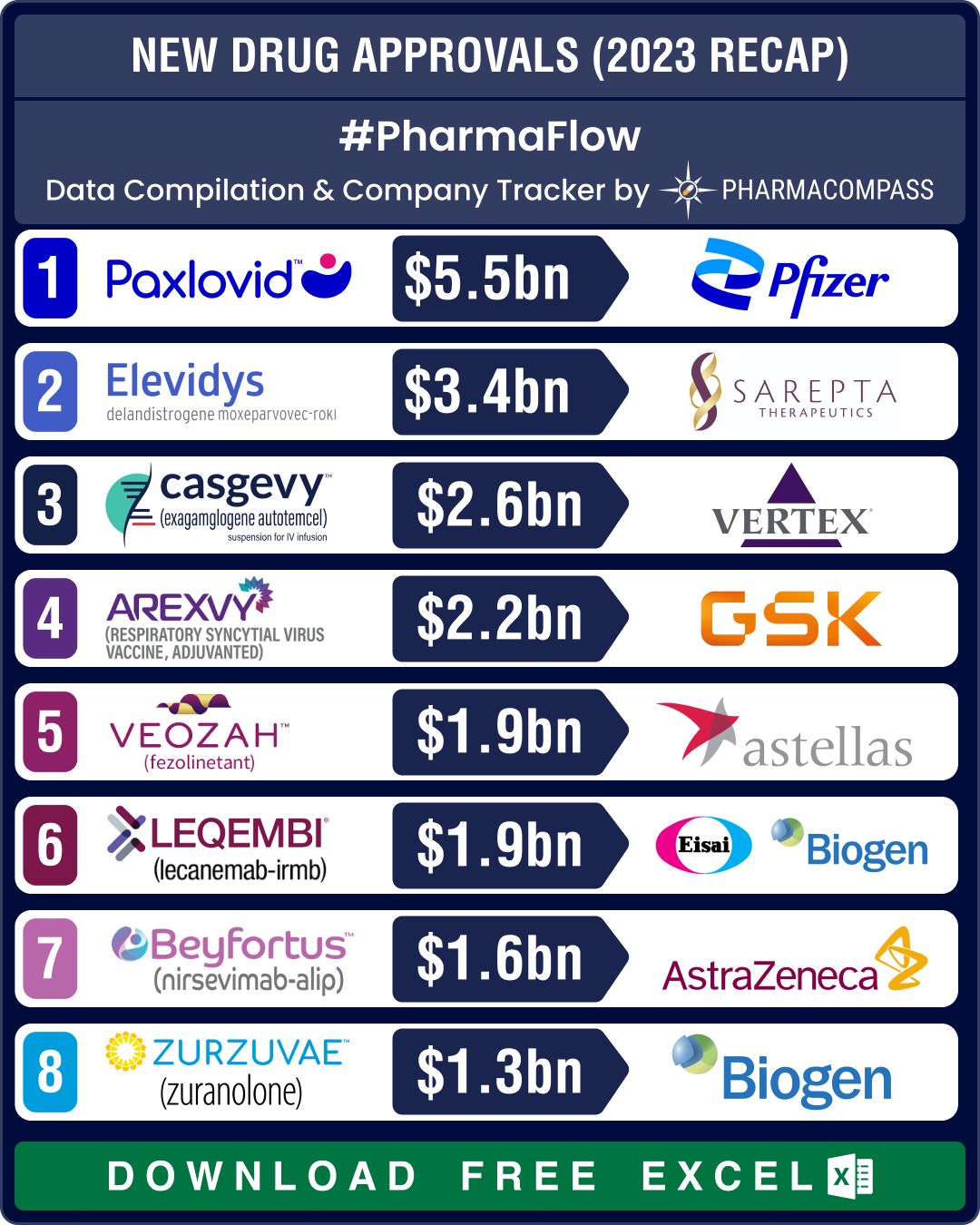

FDA approvals rise 49% in 2023; CRISPR’s gene editing therapy sees light of day

In 2022, when the

US Food and Drug Administration (FDA) was reeling under the impact of the

pandem

Top Pharma Companies & Drugs in 2021: Covid vaccines, pills cause churn in list

Every year, the list of top pharmaceutical products and companies by sales sees some churn. But the

Top drugs and pharmaceutical companies of 2019 by revenues

Acquisitions and spin-offs dominated headlines in 2019 and the tone was set very early with Bristol-