Market Place

Market Place Sourcing Support

Sourcing Support

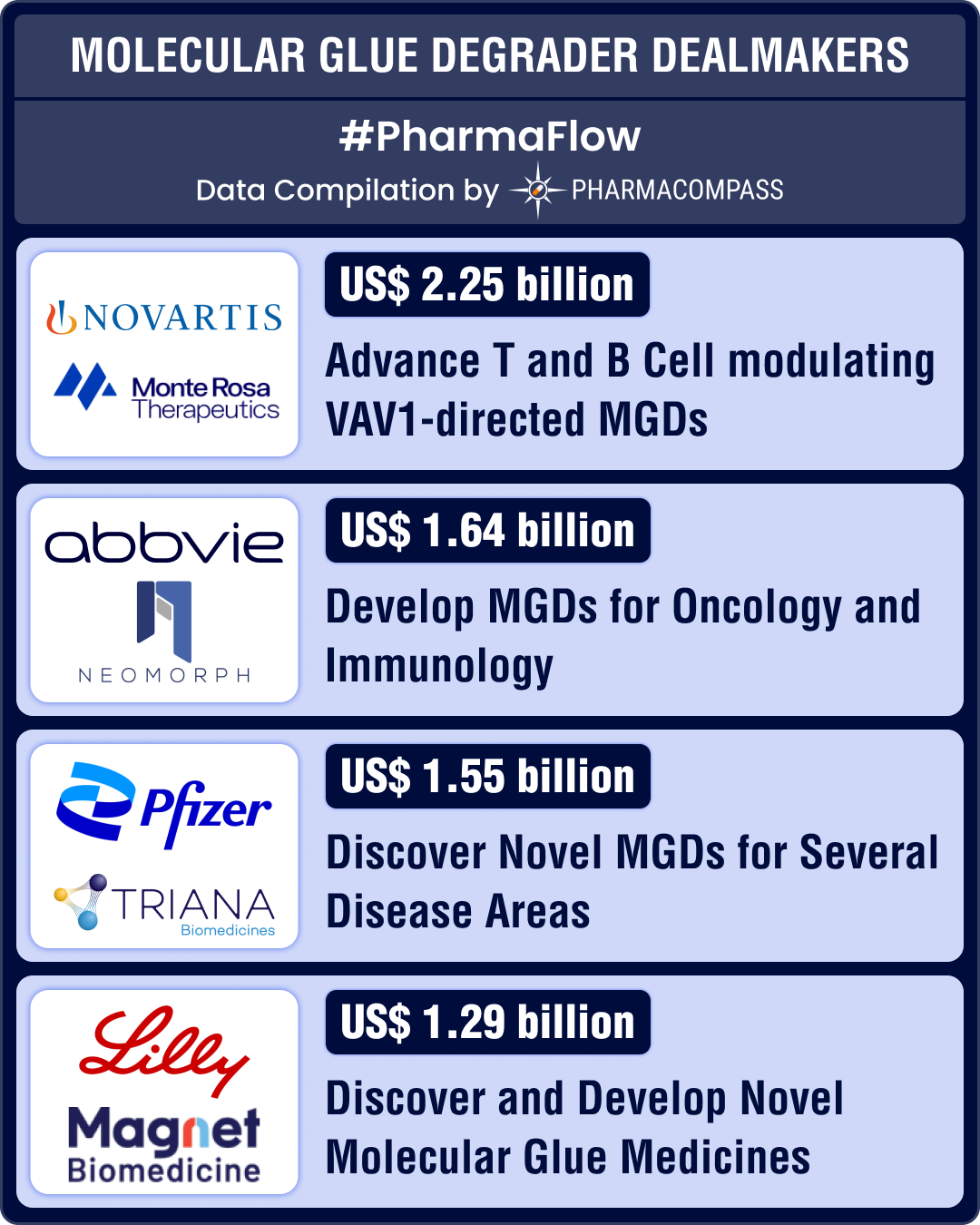

Molecular glue degraders: Lilly, AbbVie sign billion-dollar deals; BMS leads with three late-stage drugs

This week, we delve into molecular glue degraders (MGDs), one of the most promising frontiers in dru

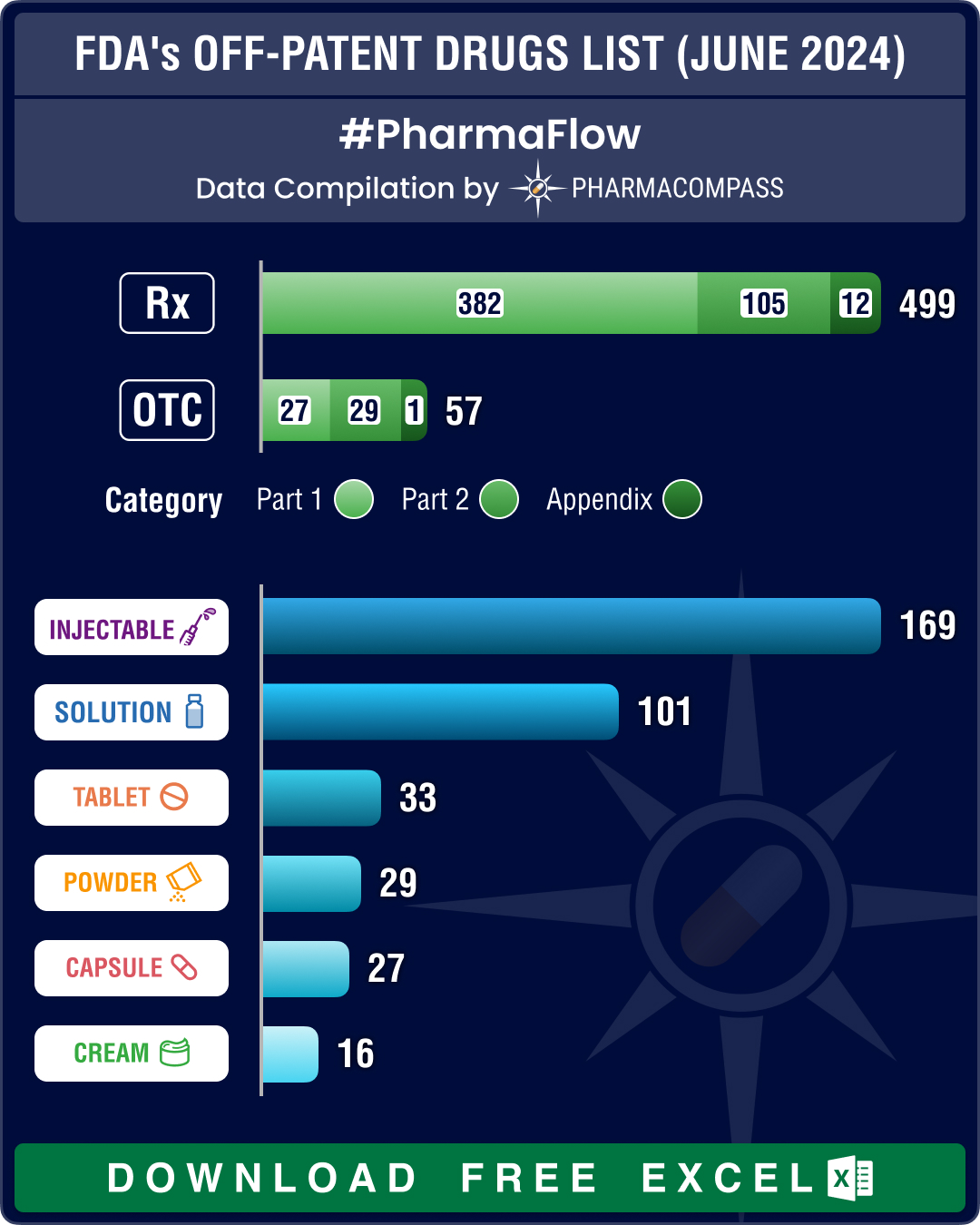

FDA’s June 2024 list of off-patent, off-exclusivity drugs sees rise in cancer, HIV treatments

This week PharmaCompass brings to you key highlights of the US Food and Drug Administration’s